Insect Protein Market Growth and Future Trends 2025 –2032

Home |

2026-06-18 07:30:38

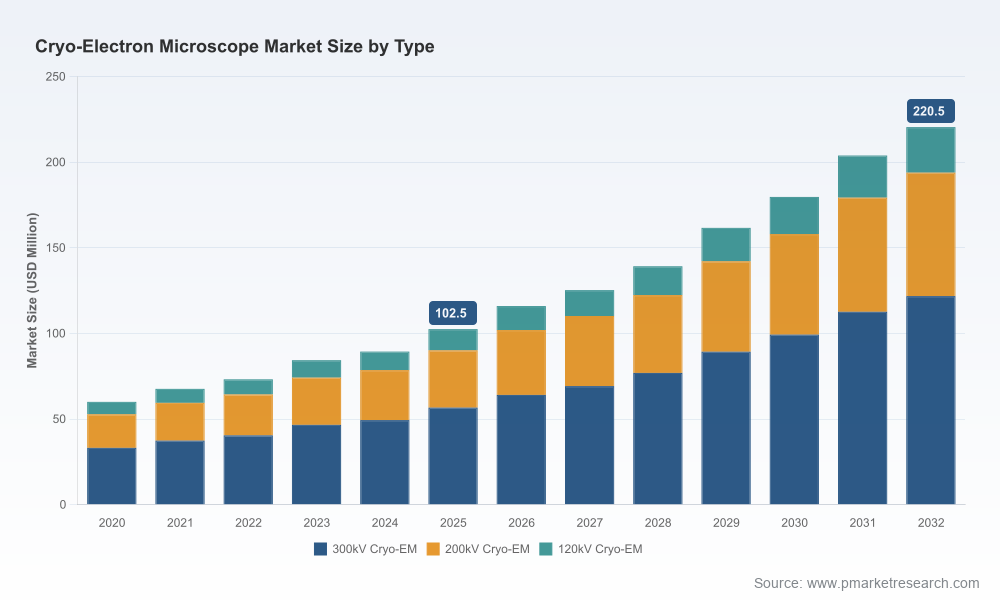

As organizations recalibrate investment priorities for 2026, the cryo‑electron microscope (cryo‑EM) market is emerging as a strategically important, fast‑growing segment of the life‑ and materials‑science instrumentation landscape. This preview synthesizes the most consequential findings from PW Consulting’s full Cryo‑EM Market Study (base year: 2025, forecast period: 2026–2032), highlighting the trends, competitive moves, funding dynamics and decision frameworks that will determine winners and losers over the next strategic planning cycle. The global market is on a sustained upward trajectory — expanding from the 2025 base and projecting robust growth out to 2032 at an 11.65% CAGR — a profile that calls for targeted, time‑sensitive responses from vendors, buyers, investors and policy stakeholders.

Cryo-Electron Microscope Market

Timing: 2026 is a hinge year in which technological maturation (AI‑enabled automation, improved detectors, cryo‑FIB workflows) converges with structural biology demand and renewed public funding. Decisions made this year about product roadmaps, capital deployment, and shared‑facility investments will shape market positions for the remainder of the decade.

Cryo-Electron Microscope Market

Risk/Return profile: The market’s sustained double‑digit growth makes it attractive, but capital intensity and service complexity create distinctive execution risks. Understanding concentration dynamics, channel economics, and lifecycle service models is essential to de‑risk investments.

Cryo-Electron Microscope Market

Strategic inflection points: Funding programs and national center initiatives are broadening access and skills, changing the buyer base from a small set of elite labs to a larger ecosystem of core facilities, contract research organizations (CROs), and industry R&D centers.

Our analysis shows a consistent, technology‑led expansion: a post‑2020 recovery into 2025 and a sustained, forecasted expansion through 2032 at an 11.65% compound annual growth rate. That trajectory is supported by several reinforcing forces: continued demand for atomic‑level structural insights in drug discovery, accelerated adoption of cryo‑ET and correlative workflows in cell biology and materials science, and incremental productivity gains from instrument automation and AI‑assisted reconstruction.

For strategy teams, the implications are clear. Vendors should treat this as a scale play: innovate to increase usable throughput and uptime, build out service and consumables revenue streams, and create partnerships that lower the total cost and time to usable data for end customers. Institutional buyers and governments should weigh the benefits of adding capacity against the material requirements of long‑term operation — investment in shared infrastructure and training will unlock disproportionate access benefits compared with isolated purchases.

The sector is moderately concentrated: the top three suppliers control a dominant share of high‑end system deployment, and the top five collectively account for an even larger portion of the installed base. Competition is less about single hardware specs and more about integrated workflow value: ease of use, automation, detector performance, specimen preparation and cryo‑FIB integration, software and AI pipelines, consumables, and long‑term service contracts.

Thermo Fisher Scientific — continues to push system automation and optics upgrades into the market. Recent product introductions emphasize AI‑enabled workflows and higher productivity for structural biology users, and their scale gives them leverage in service and consumables ecosystems.

JEOL Ltd. — remains focused on field‑emission, high‑stability platforms aimed at single‑particle analysis and beam‑sensitive specimens, positioning for customers who prioritize resolution and stability for specialized applications.

Carl Zeiss AG — differentiates through cryo‑FIB/SEM capabilities and 3D imaging workflows that speak to labs conducting correlative microscopy and complex sample preparation.

Gatan, Inc. — is a critical ecosystem player, supplying detectors, automation and accessories; success in the market will track how detector performance, data throughput and workflow interoperability evolve.

Oxford Instruments — focuses on cryo‑stages and cooling infrastructure; these supporting technologies are increasingly strategic as end‑to‑end sample integrity becomes a competitive axis.

Taken together, vendor strategies divide along two axes: integrated platform providers that bundle hardware, software and services, and best‑of‑breed suppliers that focus on critical subsystems (detectors, stages, consumables). Winning models will combine strong product performance with scalable service and training networks.

Public funding and national initiatives are materially changing adoption economics and talent pipelines. Recent grants and notices of funding opportunity aimed at national cryo‑EM and cryo‑ET centers are expanding access to instrumentation and structured training programs. Those initiatives accelerate diffusion by lowering the upfront barrier for researchers, creating demand for shared facility management services, and formalizing curricula that produce instrument‑ready personnel.

Concurrently, scientific meetings and congresses through 2026 are amplifying best practices and reducing knowledge transfer lags between instrument manufacturers, core facilities and end users. For strategic planners, the key takeaway is to treat policy and academic networks as a distribution channel: capture partnerships early, align product roadmaps with training curricula, and design service offerings that fit shared‑facility economics.

Vendors (hardware and subsystems): Prioritize automation and software interoperability. Invest in embedded AI that demonstrably reduces operator time to publishable results. Strengthen field service and remote diagnostics to improve uptime economics for customers who share capacity across projects.

Institutional buyers / core facilities: Evaluate acquisition strategies against a shared‑resource model. Consider staged investments: initial access through national centers or CRO partnerships, followed by targeted purchases as in‑house expertise and throughput justify full ownership.

Investors and M&A teams: Look for targets that expand workflow control (detectors, automation software, sample prep) or that deepen service reach into core facilities. Assess integration risk and recurring‑revenue potential from consumables and maintenance.

Service providers / CROs: Differentiate on turnaround time, reproducibility, and bundled analytics. Partnerships with instrument OEMs and subsystem suppliers can create preferential access and improve margins.

Policymakers and funders: Commit to workforce development programs and flexible shared‑infrastructure grants. Funding that lowers operating costs and invests in operator training yields outsized gains in national research productivity.

Proprietary market sizing and scenario models (2020–2032) that quantify upside and downside paths under different technology adoption and funding scenarios.

Competitive scorecards that assess product, service and ecosystem strengths across the leading vendors, with implications for partner selection and vendor negotiation strategies.

Go‑to‑market playbooks for hardware OEMs and subsystem suppliers: channel choices, pricing frameworks, service contract structures, and bundling options that accelerate adoption in core facilities and industry R&D.

Procurement and total cost‑of‑ownership templates tailored for institutional buyers, including sensitivity analyses for utilization, staffing and consumables — designed to support capital‑budget approvals.

Supply‑chain and component risk mapping, including critical subsystem dependencies and mitigation levers that preserve uptime in constrained markets.

Policy and funding intelligence that translates recent public programs and grant mechanisms into near‑term access pathways and partnership opportunities.

Buyer case studies and interviews from leading core facilities and industrial labs that reveal real‑world tradeoffs in adoption, staffing and workflow design.

Note: This preview deliberately omits the detailed regional and application splits, discrete segment‑level pricing tables, and certain procurement cost lines included in the full report. Those granular data and downloadable models are available with the subscription or single‑report purchase and are essential for operational planning and bid‑level decisioning.

In aggregate, the cryo‑EM market in 2026 represents a growth opportunity with a clear ruleset: technology performance and workflow productivity drive adoption; service and consumables create recurring revenue; and public funding plus shared facilities are reshaping who buys and who uses high‑end systems. The market’s projected expansion from the 2025 base at an 11.65% CAGR through 2032, along with its moderate concentration among a handful of established suppliers, points to a period of consolidation around integrated workflows and scale‑oriented service models.

If your 2026 strategic plan includes positioning in structural biology, correlative imaging, or high‑resolution materials analysis, you should treat this study as a decision accelerant: it connects market sizing to executable playbooks, competitor dynamics to M&A screens, and funding trends to procurement timing. To access the full datasets, scenario models, and tactical roadmaps that underpin these conclusions, PW Consulting’s comprehensive report and advisory services provide the next step to operationalize your strategy.

For detailed analysis of this topic, please visit the official page:Cryo-Electron Microscope Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com