Three Dimensional Transistor Market 2026 Growth Outlook Through 2032

Health |

2026-07-08 10:29:18

As shipping decarbonization and tighter emissions enforcement reshape capital and lifecycle choices across fleets, turbochargers have migrated from being purely performance components to pivotal nodes in fleet-level strategy. PW Consulting’s Ships Turbocharger Market study (base year 2025, forecast 2026–2032) synthesizes market sizing, regulatory impact assessment, supplier capabilities and aftermarket economics into an actionable playbook for executives making 2026 decisions. The market recorded steady expansion across the 2020–2025 period and, following a 5.3% CAGR projection, is modelled to continue growing into the next decade — reflecting a combination of newbuild demand, retrofit cycles and increasing emphasis on efficiency and emissions compliance.

Ships Turbocharger Market

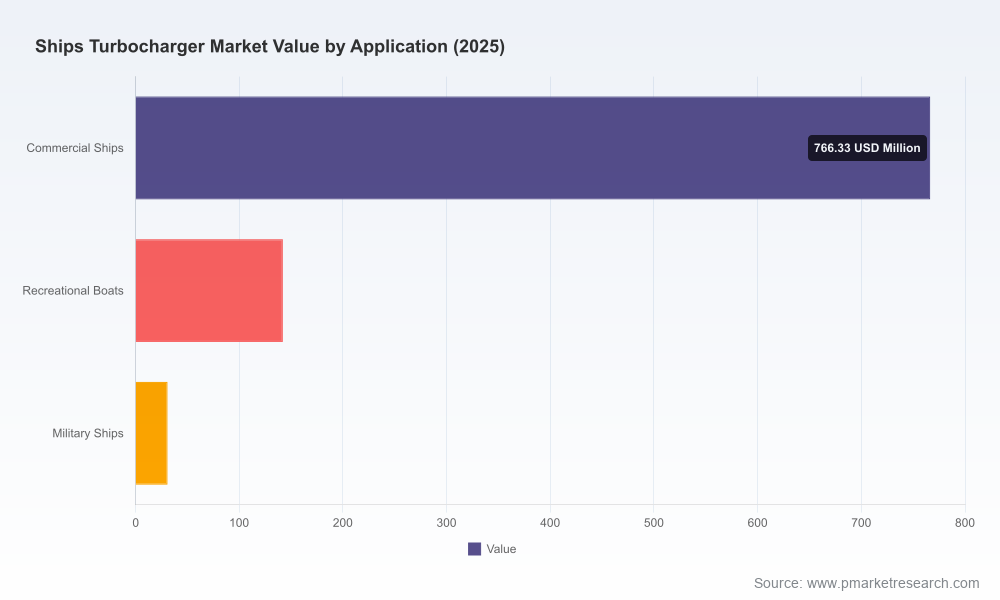

From USD 729.97 Million in 2020, the ships turbocharger market expanded through 2025 and is forecast to reach approximately USD 990 Million in 2026, continuing to climb to roughly USD 1.37 Billion by 2032 under the core forecast. This trajectory indicates a market that is mature but with sustained, technology-driven upside.

Ships Turbocharger Market

The compound annual growth rate of 5.3% across the forecast period signals steady demand that will reward firms able to combine product innovation with robust service models and regulatory alignment.

Ships Turbocharger Market

Market concentration is moderate: top-tier suppliers command meaningful share, but there remains room for challengers who can deliver niche performance advantages, localized service networks, or integrated system solutions.

Regulatory tightening is the single-largest strategic driver. IMO Tier III NOx limits, ongoing MARPOL Annex VI enforcement and convergent regional frameworks (including EPA rules and EU/US type-approval regimes) are forcing turbocharger design and fleet owner procurement decisions to embed after-treatment and control-system integration from the outset. For many operators, turbocharger selection is now an emissions compliance decision as much as a power/efficiency selection.

Energy transition and fuel flexibility matter. As operators pilot LNG, methanol, ammonia and e-fuels, turbocharger architectures that offer adaptability across combustion chemistries — while preserving thermal efficiency and durability — will capture a premium. The ramp-up of e-fuels and dual-fuel engines creates retrofit and newbuild opportunities, but timelines are lumpy and geography-dependent; firms must be ready to pivot product lines and certification routes quickly.

Aftermarket and service revenue are strategic differentiators. The shift toward service agreements, performance-based contracts and digital monitoring is intensifying. Players that lock-in long-term agreements or provide predictive-maintenance platforms convert one-time sales into recurring, higher-margin revenue.

Supply chain resilience and localization have moved from operational nicety to board-level priority. OEMs and suppliers face lead-time volatility for specialist machining, bearings and control electronics. Strategic partnerships, licensing, and selective local manufacturing reduce disruption risk — especially where local type approvals and retrofit-ready stocks are decisive for buyers.

Technology bifurcation: incremental vs platform innovation. Some suppliers pursue incremental efficiency gains around compressor/ turbine aero and control calibration; others are investing in new low-speed platforms and digital integration for system-level gains. The market will reward both, but on different timelines and with different margin profiles.

Our analysis profiles the sector’s leading and fast-moving suppliers and synthesizes recent moves that matter for 2026 sourcing, partnership and M&A strategies. Key firms include Accelleron (ABB’s turbocharging division), Mitsubishi Heavy Industries (MET series licencing footprint), MAN Energy Solutions, IHI Corporation, Everllence, and Cummins. Taken together, these firms illustrate three distinct strategic archetypes:

Technology-integrator OEMs: Firms that offer broad engine-to-turbocharger systems and leverage OEM relationships to secure newbuild content share (e.g., MAN, MHI). Their advantage is system integration and scale.

Service- and performance-led specialists: Companies pushing aftermarket agreements, digital services and retrofit portfolios to extract recurring revenue and capture retrofit windows (e.g., Accelleron/ABB, Everllence).

Platform-focused challengers: Suppliers investing in next-generation low-speed and medium-speed platforms that target specific fuel types or operational profiles.

Notable recent developments — especially from Accelleron — underline where the market is concentrating its attention in early 2026: approvals from engine OEMs for service-friendly designs, high-volume order milestones for low-speed product lines, new product launches targeted at low-speed applications, and expanded service agreements that link product sales to energy-transition priorities. These moves illustrate a playbook that combines product approval (to unlock OEM chains), scalable production, and a services overlay to capture lifetime value.

This study is built for executives who must make 2026 capital allocation, procurement and M&A decisions under uncertainty. It contains:

A calibrated market model (base year 2025; forecast 2026–2032) with scenario variants for conservative, base and high-adoption pathways — enabling CFOs to stress-test capex and revenue cases.

Regulatory impact mapping and a type-approval matrix showing where design changes and certification lead-times will most affect time-to-market (IMO, EPA, EU, US Coast Guard implications).

Supplier scorecards and a negotiation playbook: capability maps, service-network overlays and a risk-adjusted supplier valuation framework suitable for procurement and corporate development teams.

Aftermarket economics and service strategy blueprints: pricing levers, digitalization roadmaps, and retrofit demand models that quantify recurring revenue potential vs one-time sales.

Technology roadmap and integration checklist: decision criteria for axial vs radial architectures, control-electronics strategies, and fuel-flexible design considerations — presented as actionable decision trees rather than academic survey data.

Target shortlist and M&A screening filters based on capability gaps, geographic coverage and service-network synergies — optimized for 12–24 month execution horizons.

For executives facing imminent choices — product launches, supplier selection, retrofit investment, or M&A — we recommend a three-track approach:

Immediate: Rebase procurement and compliance plans on the regulatory matrix in this report. Confirm type-approval paths with engine OEM partners and prioritize designs that reduce integration time for after-treatment systems. This reduces retrofitting risk and protects newbuild content share.

Near-term (6–18 months): Convert product features into service propositions. Invest in condition-monitoring analytics and repackage turbocharger offerings as lifecycle services. Our models show meaningful margin expansion for firms that shift to multi-year service contracts and predictive maintenance.

Strategic (18–36 months): Use the supplier scorecards to identify bolt-on acquisitions or licensing relationships that close capability gaps (e.g., low-speed platform expertise, local manufacturing for strategic markets, digital service IP). The market’s moderate concentration means well-targeted M&A can materially alter competitive position.

Turbochargers sit at a crossroads of regulatory compliance, fuel transition and operational economics. The next 18 months will see fleets and shipyards convert regulatory and fuel uncertainty into concrete procurement decisions — and suppliers that can demonstrate approved, fuel-flexible platforms coupled with service ecosystems will capture disproportionate upside. PW Consulting’s Ships Turbocharger Market study equips leaders with the market sizing, regulatory mapping, supplier intelligence and executable playbooks needed to convert 2026 uncertainty into durable advantage.

To evaluate how these dynamics map to your product roadmap, procurement pipeline or M&A appetite, download the full report. The report contains the granular models, supplier scorecards and certification timelines that are essential to operationalize the strategies outlined here.

For detailed analysis of this topic, please visit the official page:Ships Turbocharger Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com