Luxury Furniture Market 2026: Strategic Imperatives for Executives — A PW Consulting Preview

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a concise but incisive preview of our latest Luxury Furniture Market study — a briefing designed to frame the critical strategic choices facing executives in 2026. The luxury furniture sector is no longer niche craftmanship insulated from macro forces; it is a dynamic, innovation-led market whose structural trajectory and regulatory volatility will materially shape investment, sourcing and go-to-market decisions over the coming planning cycles.

Luxury Furniture Market

Executive snapshot — why this study matters in 2026

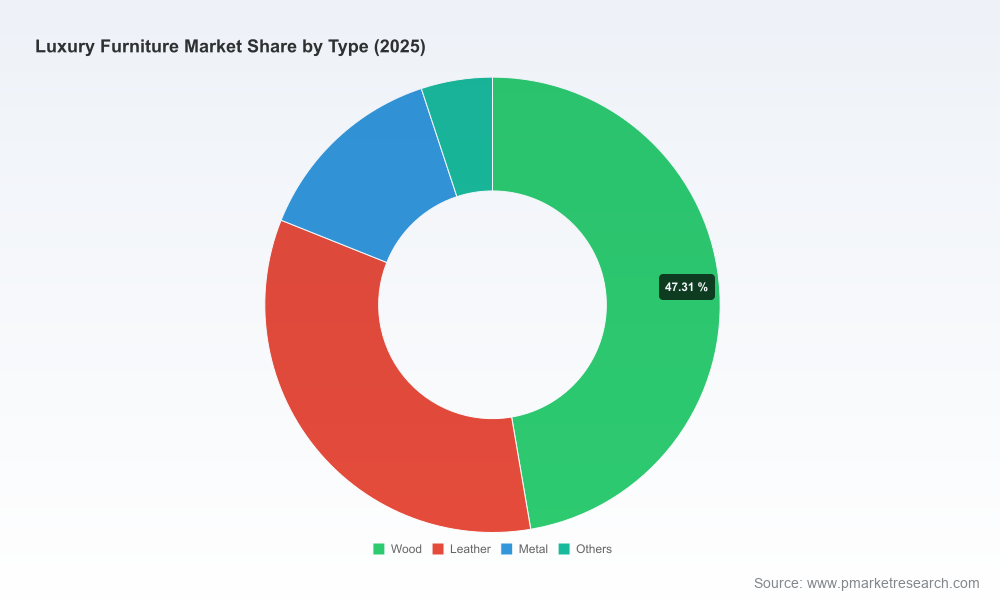

The global luxury furniture market has entered a multi-year expansion phase. By 2025 the market had surpassed the low‑double-digit billion dollar mark and is projected to grow at a compound annual growth rate (CAGR) of approximately 5.74% through the 2026–2032 forecast window, reaching a materially larger scale by the end of that period. This baseline growth conceals important shifts in demand composition, value capture and supplier economics that will determine which firms win in the second half of this decade.

Luxury Furniture Market

For C-suite leaders, this report serves three immediate purposes in 2026: (1) to convert headline growth into actionable portfolio choices; (2) to align capital allocation with near-term regulatory and supply‑chain risk; and (3) to identify capability gaps—whether in circular design, premium DTC channels, or contract/experiential services—that will determine competitive advantage.

Luxury Furniture Market

Market trajectory and strategic implications

- Sustained, premium-led growth: The mid-single-digit CAGR projects a healthy expansion that is concentrated among premium segments that combine design provenance, customization and sustainability credentials. Growth is not uniform; margins and valuation multiples will diverge sharply between commoditized suppliers and brands that can command experiential pricing.

- Profit pools are shifting: Value is migrating from pure manufacturing scale toward differentiated capabilities — proprietary design, brand equity, after‑sales services (refinishing, refurbishment) and circular product lifecycles. Executives should evaluate margin roadmaps that assume increasing returns to brand and service integration.

- Fragmentation and consolidation potential: The market remains moderately fragmented: leading players do not yet dominate a majority share, leaving room for targeted consolidation and partnership plays. Strategic M&A and bolt-on investments will be decisive for firms aiming to scale distribution, obtain design IP, or internalize sustainable supply chains without excessive capex.

Demand drivers and supply-side dynamics

Several interlocking forces underpin the forecasted expansion and are central to 2026 strategic planning:

- Demographic and lifestyle evolution: High-net-worth cohorts and aspirational mass affluents are investing more in curated living spaces and bespoke pieces. Remote work permanence in premium segments is increasing demand for home office luxury solutions that balance ergonomics and aesthetics.

- Sustainability as a purchase determinant: Buyers are rewarding circularity, traceability and low-carbon materials. Early adopters that can demonstrate circular design, take-back programs, and third-party sustainability certification are commanding premium pricing, faster sell-through and stronger resale economics.

- Supply chain recalibration: Tariff uncertainty, input-cost inflation and logistics bottlenecks are forcing firms to diversify sourcing, onshore critical manufacturing steps, and invest in nearshoring or regional micro-factories to protect lead times and margin.

- Experience over product: Luxury customers buy narratives — provenance, designer collaborations and service experiences. Firms that build omni-channel showrooms, virtual customization tools and membership-based care services capture higher lifetime value.

Competitive landscape — strategic profiles of core players

The competitive map blends long-standing European ateliers with US design-forward and contract-focused firms. Each archetype suggests distinct playbooks:

- Italian and French design houses (e.g., Poltrona Frau, B&B Italia, Minotti, Cassina, Roche Bobois): These incumbents trade on heritage, artisanal manufacturing and high-design collaborations. Their strategic advantage lies in IP-rich design catalogs, atelier networks, and aspirational showroom experiences. In 2026, their focus will likely be on protecting brand cachet while scaling circular initiatives and selective licensing.

- US-based innovators and contract specialists (e.g., Knoll, Herman Miller, Restoration Hardware, Kimball International, Baker Furniture): These firms combine design credibility with robust contract channels (hospitality, corporate) and operational scale. Expect aggressive investments in ergonomic premium home office collections, integrated contract solutions, and digital direct-to-consumer (DTC) platforms that shorten the path to consumer insight.

- Strategic implications: European luxury brands should prioritize securing material provenance, scaling made-to-order systems and protecting export economics amid tariff volatility. US players should leverage supply-chain scale, accelerate aftermarket services, and deepen partnerships with architects and developers to capture contract spend.

Regulatory and geopolitical “noise” — immediate 2026 considerations

Policy and trade developments in late 2025 and early 2026 inject tangible uncertainty into sourcing and pricing decisions:

- The US administration has delayed planned tariff increases on certain imported furnishings, maintaining current duties for an additional year. This temporary reprieve provides a planning window but not certainty — executives must model scenarios for tariff reinstatement and hedging strategies.

- European manufacturers are contending with proposed punitive measures on exports to the US, raising the specter of reciprocal duties that could reshape cross‑border sourcing economics and push more production domestically or to neutral third countries.

- Recent jurisprudence limited the scope of reciprocal tariffs while affirming existing duties on specific upholstered imports, creating a mixed precedent that keeps importers and brands on high alert for discrete policy shifts.

Strategic takeaway: Treat regulatory outcomes as a material risk factor. Accelerate flexible sourcing, dual‑sourcing, and tariff-optimized product engineering. Where possible, use the current delay in tariff changes as a controlled environment to pilot nearshoring investments or to trial circular logistics that reduce exposure to import cycles.

Notable recent market development

In May 2026, a prominent manufacturer introduced a formal Sustainability Standard for luxury furniture manufacturing, emphasizing circular design and take-back economics to reduce the traditional buy‑and‑dispose model. This move signals a nascent industry standardization push: firms that lag risk losing both premium customers and access to certain distribution partnerships that will increasingly require demonstrable lifecycle credentials.

Actionable strategic playbook for 2026

From boardroom to plant floor, the following priorities will produce measurable outcomes through 2026 and position firms to capture disproportionate value as the market scales:

- Reallocate capex toward modular, nearshore production: Prioritize modular manufacturing cells that support customization without sacrificing throughput. Nearshoring reduces tariff risk, compresses lead times and enhances quality control.

- Invest in circular product systems: Pilot refurbishment services, certified materials registries and customer trade-in programs. Quantify resale economics and include them in lifetime value models to justify initial capex.

- Upgrade digital channels to experiential commerce: Digital configurators, AR-enabled showrooms and concierge-level DTC logistics convert design equity into higher conversion and aftermarket service revenue.

- Balance brand exclusivity with scale partnerships: Pursue selective licensing and co-branded collections to access new channels while preserving premium positioning. Evaluate M&A targets that add capability (e.g., logistics, upholstery specialists, circular refurbishment platforms).

- Scenario-plan for trade shocks: Build three tariff/ trade scenarios into 2026 budgets, stress-testing pricing, margin and working capital. Implement contractual hedges and diversify supplier footprint across tariff-exposed geographies.

- Embed sustainability in commercial KPIs: Link sustainability metrics (material traceability, take-back rates) to distributor incentives and executive compensation to accelerate implementation.

What our full report delivers — practical content overview

The PW Consulting Luxury Furniture Market report goes beyond headline forecasts. It provides the operational playbooks and analytics required to execute in 2026, including:

- Buy-side and sell-side decision frameworks that translate growth projections into SKU rationalization, pricing ladders and channel investment plans.

- Supplier resilience diagnostics and a toolset for tariff-optimized sourcing and onshore/nearshore transition roadmaps.

- Actionable M&A filters and synergy calculators for consolidating premium manufacturing, scaling DTC logistics, or acquiring circular service platforms.

- Commercial strategies for brand licensing, designer collaborations and contract-market penetration with quantified revenue levers and margin scenarios.

- Benchmarks on operational metrics, service economics and sustainability KPIs, tailored to C-suite and board-level decision-making.

Consciously, this preview omits the granular segmentation tables and proprietary regional/application breakdowns that drive precise tactical choices; those sensitive analytics are reserved for the full report and are essential for route-to-market execution.

Final recommendation — how to use this preview

Use this briefing to orient 2026 planning: prioritize optionality, defend margin through service integration, and accelerate circularity as both a margin and risk-management tool. For private equity investors, the combination of mid-single-digit growth, moderate fragmentation, and regulatory tailwinds presents clear roll-up and operational-improvement opportunities. For incumbent brands, the test is whether you can convert design pedigree into systemic, service-enabled economics without diluting exclusivity.

For a complete set of proprietary segment models, regional demand scenarios, and the tactical worksheets your operations and M&A teams need, access the full PW Consulting Luxury Furniture Market study on our website. The full report contains the granular intelligence that converts these strategic imperatives into executable 90‑ and 180‑day plans.

For detailed analysis of this topic, please visit the official page:Luxury Furniture Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com