Nerve Repair and Regeneration Biomaterials Market Analysis: Opportunities Across Regenerative Medicine Applications

Health |

2026-07-02 12:35:27

The carbon offset and carbon credit trading services market is entering a phase of accelerated institutionalisation. From a clearly measurable base in 2025, the market is set to expand rapidly through 2032, driven by regulatory tightening, corporate net‑zero commitments, and growing demand for verified removals. PW Consulting’s new market study synthesises quantitative forecasting with practical, transaction‑level guidance designed to inform corporate strategy, procurement, investment and risk management through 2026 and beyond.

Carbon Offset/Carbon Credit Trading Service Market

Time‑sensitive regulatory shifts: 2026 is when multiple policy vectors—ranging from regional ETS pathways for durable removals to ongoing amendments to cap‑and‑invest programs—interact with market infrastructure launches and registry reforms. These moves materially change eligibility, price formation and counterparty risk profiles for buyers and sellers.

Carbon Offset/Carbon Credit Trading Service Market

Market scale and momentum: The market that was modest but active a few years ago has expanded substantially and is projected to continue compounding at a double‑digit pace. That trajectory changes the calculus for long‑dated offtakes, capital deployment into removals, and integration of carbon trading into enterprise risk frameworks.

Carbon Offset/Carbon Credit Trading Service Market

Operational complexity: New registry technology, independent quality raters, and blockchain‑enabled platforms create both opportunity (lower friction, novel products) and complexity (interoperability, custody, legal enforceability). Corporates must move from high‑level pledges to operational procurement playbooks in 2026 if they are to avoid elevated financial and reputational costs.

PW Consulting’s modelling uses 2025 as the base year, builds on a five‑year historical series (2020–2025) and projects through 2032. The market climbed from an identifiable low‑hundreds base in 2020 and roughly doubled by 2025; under our central scenario the sector grows at a compound annual growth rate of 22.3% across the forecast window, reaching an order‑of‑magnitude higher scale by 2032. Put simply: the market that many viewed as niche in 2020 is becoming a mainstream component of corporate climate strategy within a single corporate planning cycle.

Procurement and portfolio design: Buyers must segment credit types by quality, permanence and registry compatibility and then align procurement horizons to policy milestones (e.g., ETS pathways, CORSIA eligibility clauses). Shortlisted suppliers and project types should be stress‑tested across regulatory and price scenarios; our report supplies templates and scoring matrices to do this quickly.

Financial planning and risk allocation: With market liquidity improving but still uneven, hedging and price‑risk transfer will become core treasury functions. We provide a practical decision tree for when to lock in multi‑year offtakes versus using spot exposure, and a sample economic model for comparing internal abatement versus purchased offsets across discount rates and residual risk allowances.

Investment and M&A screening: Investors and corporate development teams need frameworks to convert credit quality, registry standing and counterparty risk into valuation multiples. Our method translates ratings, certification lineage and issuance histories into an investment score that maps to expected cashflow volatility.

Operationalising traceability and compliance: Registry interoperability and serialization are increasingly important. The report’s technical annex explains the implications of new registry technologies for custody, retirement mechanics and audit trails—essential reading for compliance and procurement teams.

Reputational risk management: As buyers face greater scrutiny, a defensible procurement playbook—combining third‑party quality assessments, transparent retirements and documented traceability—is now table stakes. We provide a checklist for disclosure‑grade documentation that meets the expectations of investors and NGOs.

Market sizing and high‑frequency forecasting (base year 2025; scenario outputs through 2032) aligned to policy milestones and technological adoption curves.

Procurement playbook: supplier shortlisting templates, contract clauses, quality scoring matrices and a model for structuring staggered offtake agreements.

Risk and compliance toolkit: registry interoperability map, due diligence checklist for counterparties and projects, and legal considerations for tradability and retirement mechanics.

Investment and valuation framework: valuation-adjusted cashflow models, sensitivity analyses and acquisition screening criteria for removals and avoidance projects.

Competitive landscape and strategic positioning guide: capability matrices for exchanges, registries, verifiers, rater platforms and emerging fintech entrants, plus partnership playbooks.

Scenario modelling engine and interactive dashboards (accessed via secure portal) that permit managers to stress test assumptions about issuance volumes, policy eligibility and quality premiums.

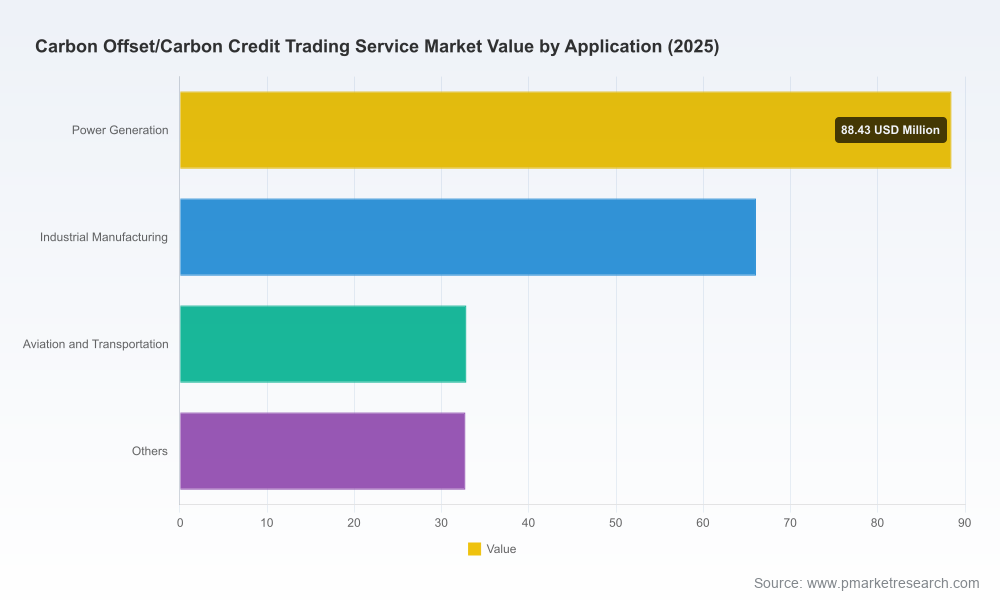

Note: in keeping with the “preview” nature of this article we showcase methodology and key macro benchmarks but intentionally withhold the granular regional, application and type splits that are included in the full report. Those segmentation layers are material to procurement and investment decisions and are available through our source page and full report purchase.

The market’s structure combines a small set of dominant registry/standard administrators and a growing cohort of specialised intermediaries and data providers. Market concentration is high: the top three platform/standard players account for a commanding share of registry issuance and liquidity, and the top five capture the overwhelming majority of formalised activity. At the same time, new entrants—ranging from independent raters to blockchain platforms—are expanding functionality and creating alternative paths to liquidity and settlement.

Registry and standard administrators: Organisations such as Verra and American Carbon Registry operate core crediting programs and registries that underpin both voluntary and compliance flows. Their program rules and major updates materially affect market eligibility and supply timing.

High‑integrity certification and marketplace actors: Gold Standard focuses on high‑integrity, SDG‑aligned credits while marketplace operators and curators such as TerraPass, Wren and Carbon Direct bridge buyers and projects, packaging credits for corporate customers.

Quality and analytics providers: Independent raters—Sylvera, BeZero Carbon, Calyx Global—provide essential intelligence on project quality, additionality and risk; their coverage is increasingly integrated into buyer procurement frameworks and pricing models.

Infrastructure and fintech innovators: Exchanges and registry tech efforts (e.g., ICE GreenTrace™), and blockchain-enabled platforms such as Toucan Protocol and Carbonmark, are lowering transaction costs and enabling new liquidity pools—especially for removal credits that require durable serialization.

Standards evolution: major program updates and methodology approvals are being issued in 2026, with implications for which project vintages and methodologies will remain bankable into the late 2020s.

Market intelligence expansion: independent ratings firms are broadening coverage and regional footprint, making it easier for buyers to apply credit quality overlays to procurement decisions.

Infrastructure builds: registry and trading platforms are rolling out improved technology stacks to support traceability, settlement and compliance workflows—lowering operational friction for larger corporate portfolios.

Policy interplay: concurrent regulatory developments—from aviation schemes to domestic ETS reforms and extended state cap‑and‑invest horizons—are redefining demand windows and eligibility criteria for a wide set of credits.

Our projections combine historical issuance and transaction data, policy timelines, corporate offtake trends, and input from market participants. The base year is 2025, the forecast period spans 2026–2032, and currency is USD (revenue units reported in millions). We employ scenario analysis (central, upside, downside), sensitivity testing and Monte Carlo simulation on key assumptions such as issuance growth, policy eligibility timing and quality premia. Full model inputs, assumptions and confidence intervals are documented in the report annex.

Embed carbon procurement into capital planning and procurement cycles now—delay raises procurement cost and increases exposure to supply‑shock price spikes.

Adopt a two‑track approach: secure a baseline of high‑quality credits for near‑term reporting and gradually add high‑integrity removals through staged offtakes that reflect evolving policy clarity.

Invest in internal capability—legal, procurement, treasury and sustainability—so your organisation can evaluate credit quality, legal enforceability and balance‑sheet treatment without outsourcing every decision.

Use third‑party quality ratings and registry provenance as a minimal control; build layered due‑diligence for larger or multiyear commitments.

This article is a strategic preview. The full PW Consulting Carbon Offset/Carbon Credit Trading Service Market report contains the granular segmentation, region and application level detail, contract language examples, interactive scenario dashboards and the complete competitive profiles necessary to operationalise the guidance above. For teams making procurement, investment or compliance decisions in 2026, the full study and our bespoke advisory engagements will materially reduce risk and improve negotiation outcomes.

For detailed analysis of this topic, please visit the official page:Carbon Offset/Carbon Credit Trading Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com