Polyurethane Sealants Market — Strategic Outlook for 2026 Decision-Makers

In an industry increasingly defined by input-cost volatility, tightening environmental standards, and selective consolidation, the global polyurethane sealants market presents measured growth and clear strategic inflection points for 2026. According to PW Consulting’s latest study, the market reached approximately USD 3,052 million in 2025 and is expected to expand at a compound annual growth rate (CAGR) of roughly 4.23% through the 2026–2032 forecast window, culminating in a materially larger addressable market by 2032. For senior executives and investment committees preparing capital allocation and go-to-market plans in 2026, this research is structured to convert macro trajectory into executable choices while preserving competitive sensitivity on granular segment tables and proprietary datasets.

Polyurethane Sealants Market

Why this study matters for 2026 decisions

- Timing of investment: The market’s steady mid-single-digit CAGR signals opportunities for targeted expansion—especially where product differentiation and regulatory compliance intersect with end-market demand.

- Input-cost and supply-chain risk: Accelerated feedstock price movements and trade-policy shifts mean procurement strategy and manufacturing footprint are now strategic levers, not just operational variables.

- Regulatory-driven product repositioning: Green building, maritime emissions standards, and indoor air quality benchmarks are converting into preferential procurement and spec-grade requirements—benefiting first movers that can demonstrate compliance at scale.

Market trajectory and implications

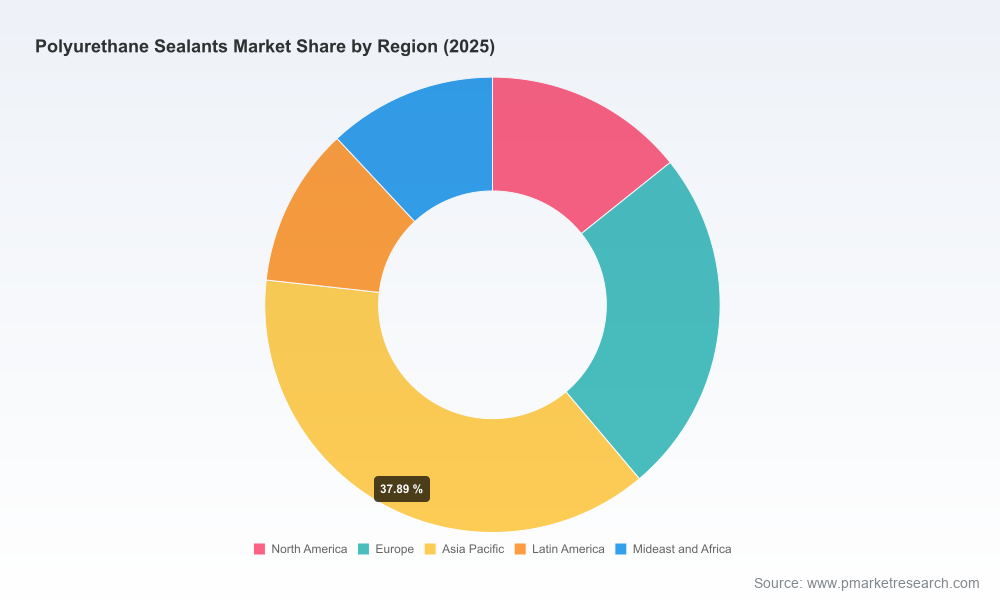

Historically, the polyurethane sealants market has shown resilient demand through construction retrofit cycles and automotive production rebounds. PW Consulting’s top-line view captures this dynamic: after a multi-year recovery, the market size observed in 2025 provides a stable base from which a 4.23% CAGR delivers meaningful incremental opportunity by the end of the forecast horizon. That growth is non-uniform—the interplay of construction spending, transportation manufacturing, and infrastructure projects creates pockets of accelerated adoption, while other segments exhibit more price-sensitivity and substitution risk.

Polyurethane Sealants Market

For executives, the implication is straightforward: prioritize investments where growth outpaces the blended market CAGR and where competitive advantage can be defended through formulations, service, or localized supply. The full report provides the granular segmentation and scenario breakdowns required to identify those pockets; to preserve commercial confidentiality, those detailed splits are available in the complete dataset available from PW Consulting.

Polyurethane Sealants Market

Key dynamics reshaping the operating environment

- Feedstock cost pressure and volatility: Isocyanate (MDI) and polyol prices experienced upward pressure into 2025–2026. Industry intelligence indicates MDI feedstock costs rose by approximately USD 200–260 per ton in February 2026, compounding margin pressure for formulators that cannot pass through higher costs or hedge exposure.

- Trade and tariff friction: Section 301 tariffs, for example, have introduced additional ad valorem duties on relevant imports, producing incentives to localize supply or renegotiate supplier terms in affected geographies.

- Regulatory and standards tailwinds: Low-VOC formulations have moved from niche to default in many developed markets as green-building certifications and indoor-air-quality standards tighten. New maritime environmental standards in Europe have also elevated demand for certified marine-grade, low-emission sealants.

- Concentration and competitive dynamics: The market exhibits a moderate-to-high concentration at the top end—buyers face a landscape in which a handful of global players control a material share of supply, but regional and niche specialists remain important for specification-driven projects.

- Product innovation and differentiation: Reformulation to meet environmental criteria, fast-curing systems for productivity, and hybrid chemistries for weather resistance are the innovation vectors likely to determine winners in 2026.

Competitive landscape — who moves the market

Market leadership is distributed among established chemical and adhesive manufacturers with global scale and channel reach, complemented by regional specialists that compete on speed-to-spec and application support. The leading incumbents—whose strategic moves and portfolios we analyze in depth—include globally integrated chemical companies and performance-adhesive specialists. Their positioning can be summarized as follows:

- Integrated global manufacturers: Firms with upstream access to feedstock and extensive production footprints are leveraging scale to manage margin compression and to accelerate low-VOC product launches.

- Formulation-driven adhesive specialists: Those with deep application engineering capabilities—particularly in construction assembly, automotive bonding, and marine sealing—are defending specification-driven channels through technical service and certified product families.

- Regional and niche players: Companies oriented around quick specification cycles, local codes, and retrofit markets maintain relevance by delivering rapid lead times and application-focused technical support.

Notable company actions that demonstrate these dynamics include portfolio and capacity expansions, targeted R&D investments in low-VOC and extreme-weather formulations, and facility openings to shorten supply chains. The full report contains individual company scorecards, comparative product maps, and M&A heatmaps that enable benchmarking and partner selection; specific segmentation lists and proprietary scoring matrices remain available in the full deliverable.

Report contents — what executives will find inside

- Comprehensive market-sizing and historical time series (base year 2025), with bottom-up validation and scenario-level forecasts through 2032.

- Competitive benchmarking: feature-by-feature product comparisons, capacity maps, and recent strategic moves (facility investments, product launches, and R&D commitments).

- Supply-chain and feedstock risk model that quantifies margin exposure to MDI and polyol price swings and tariff scenarios.

- Regulatory and standards matrix that links regional codes to product development requirements and certification pathways.

- Commercial playbooks for pricing, channel segmentation, and specification capture—tailored to construction, automotive, and marine applications.

- M&A and partnership guide that identifies adjacent capabilities and regional targets to accelerate market access or de-risk feedstock exposure.

- Decision-support dashboards and scenario planners designed for board-level capital allocation discussions.

Strategic playbook for 2026 — actionable priorities

We translate market signals into a concise set of actions for leadership teams making 2026 commitments:

- Hedge and diversify feedstock exposure: Establish multi-sourcing strategies, long-term offtake agreements, and financial hedges tied to isocyanate and polyol indices. For players with scale, evaluate vertical integration or toll-manufacturing partnerships in low-tariff jurisdictions.

- Prioritize low‑VOC reformulation: Fast-track certified low-emission product lines for construction and marine markets; invest in validated testing protocols and third-party certifications to shorten adoption timelines.

- Localize critical capacity: Use a mix of brownfield expansions and selective greenfield plants to mitigate tariff exposure and reduce lead times for specification-driven projects.

- Differentiate via application engineering: Build or acquire application-lab capabilities and field-support teams that convert spec opportunities into repeat business—particularly in window/door installation and infrastructure sealing.

- Adopt value-based pricing in premium niches: Where formulations offer documented lifecycle or productivity advantages (faster cure, longer durability), move away from commodity price competition and toward TCO-based contracting.

- Monitor M&A selectively: Target acquisition of regional formulators with certification footprints or downstream channel assets that accelerate market penetration without requiring large capex outlays.

How to use this report in boardroom and investment discussions

PW Consulting’s study is structured to be a decision enabler. Use the report to build three informed deliverables for your 2026 planning cycle:

- Scenario-backed capital-plan: Overlay three supply-and-price scenarios onto your production plan to stress-test ROI timings for new plants or product lines.

- Procurement playbook: Quantify exposure to key feedstock movements and design contractual hedges and inventory triggers tied to MDI and polyol price bands.

- Commercial growth roadmap: Define prioritized application segments and geographies—mapped to internal capabilities and competitor weak points—so sales and R&D investments are tightly aligned with highest-return opportunities.

Closing — the strategic value proposition

As companies calibrate strategy for 2026, the combination of moderate market growth and elevated supply-side risk demands disciplined prioritization: invest where regulatory compliance, product differentiation, and localized supply create defendable margins. PW Consulting’s polyurethane sealants study packages market-scale forecasting, competitive intelligence, and an actionable playbook to inform capital allocation, procurement policy, and product development decisions. The executive summary you’ve read highlights the thematic conclusions; for the granular segmentation, full company profiles, and proprietary datasets that underpin our recommendations, access to the complete report and supporting dashboards is available via PW Consulting’s source portal.

For detailed analysis of this topic, please visit the official page:Polyurethane Sealants Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com