Global Weight Loss & Diet Management Products & Services Market by 2034: Trends and Growth Analysis

Home |

2026-04-24 10:01:59

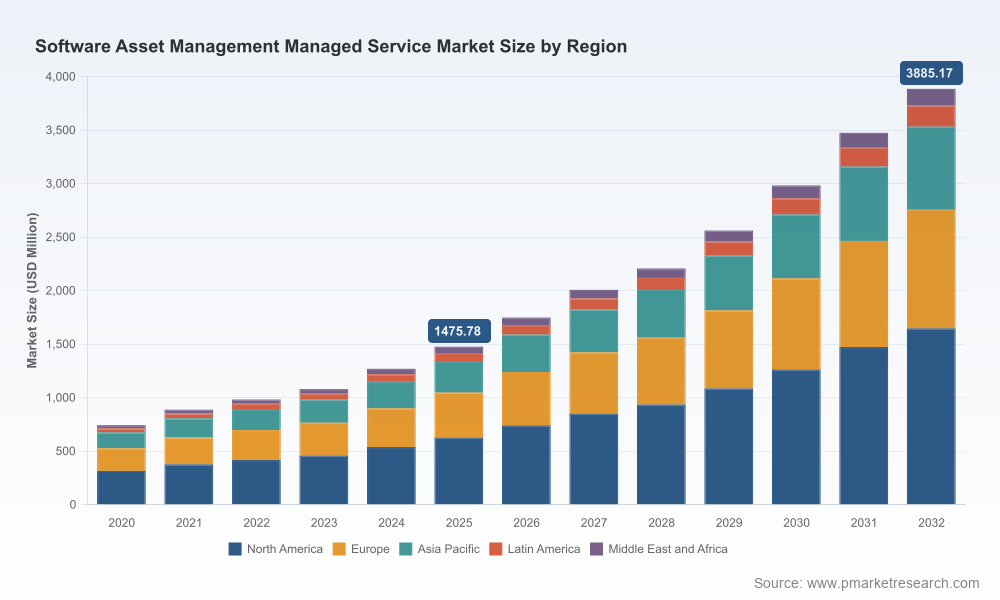

PW Consulting’s latest market research report on the Software Asset Management Managed Service market (base year: 2025; forecast: 2026–2032) provides enterprise leaders with an evidence‑based playbook for decisions that will determine cost, compliance and agility outcomes across the next contracting cycle. The market reached roughly USD 1.48 billion in 2025 and, driven by strong demand for cloud/SaaS optimization, compliance and vendor‑licensing expertise, is projected to grow at a compound annual growth rate (CAGR) of approximately 14.8% through 2032 — reaching an estimated USD 3.89 billion by the end of the forecast period. This trajectory makes SAM managed services not a discretionary line item but a strategic investment for 2026 planning.

Software Asset Management Managed Service Market

Risk surface has shifted. Heightened data privacy regimes and new rules for bulk data handling have elevated the regulatory and operational risk around software usage telemetry and license records. SAM outcomes are now tightly coupled with privacy, auditability and breach mitigation.

Software Asset Management Managed Service Market

Cloud and SaaS consumption patterns have accelerated license sprawl and subscription complexity; simple discovery is no longer sufficient — continuous optimization and controls are required to control spend and contractual exposure.

Software Asset Management Managed Service Market

Labor dynamics and skills gaps mean human expertise (vendor‑specific licensing, audit defense, and AI tool stewardship) remains a principal cost and capability constraint, even as automation matures.

Executive decision frameworks that translate the market economics and 2026 regulatory outlook into board‑level questions and CFO/CPO checkpoints.

Vendor selection matrix and weighted evaluation criteria tailored to multiple buyer archetypes (risk‑averse regulated enterprise, fast‑moving cloud native organization, and centrally governed multinational).

Implementation roadmaps and sample operating model(s) for onsite/remote/hybrid SAM managed delivery, including roles, SLA templates and staffing profiles for the next three years.

RFP templates and negotiation playbooks designed to secure audit defense, data protection commitments, breach notification clauses, and flexible commercial terms for SaaS and perpetual licensing.

ROI and TCO models that let procurement and finance teams model scenarios (outsourcing vs insourcing, tool + managed service bundles, and phased migration to AI‑assisted operations) using your own telemetry inputs.

Case studies demonstrating measurable savings, compliance outcomes and remediation timelines from recent deployments across heavily regulated industries.

Appendices covering methodology, data sources, and the detailed forecast models that power our market projections — the actionable datasets for enterprise planners and advisors.

Between 2020 and 2025 the market effectively doubled in scale, reflecting an inflection point where organizations began buying managed SAM outcomes (continuous compliance, cost optimization, audit defense) rather than discrete discovery projects. That momentum is projected to continue into 2026 and beyond, reinforcing four dynamics every buyer must account for:

Regulatory overlay: A proliferation of state and sector privacy laws and new federal rules has increased requirements for secure handling, retention and auditability of software usage data, which in turn raises the bar for contractually assured controls from SAM providers.

Convergence with FinOps and Cloud Cost Management: SAM is increasingly integrated into cloud/SaaS cost governance; buyers should expect integrated tooling and cross‑functional SLAs.

Skills scarcity and automation mix: Human, vendor‑licensing expertise remains critical, but the value equation is increasingly about the right balance of licensed tools, AI/automation and expert intervention to deliver predictable outcomes.

Vendor landscape maturation: Recognitions and analyst placements are consolidating the market narrative, but execution and delivery consistency remain primary differentiators.

Our competitive analysis synthesizes vendor strengths and positioning rather than producing a simple leaderboard. Key strategic attributes to weigh:

Depth of vendor‑licensing expertise and audit defense capabilities — critical for enterprises with large legacy estates or complex vendor portfolios.

Cloud/SaaS optimization and integration with FinOps tooling — crucial for organizations driving cloud-first consumption.

Global delivery footprint and multi‑jurisdictional compliance experience — necessary for multinational programs facing varied privacy rules.

Productized service models and automation maturity — determine unit economics and scalability of SAM outcomes.

Selected provider highlights (brief descriptors featured in the report):

Anglepoint — specialized SAM managed services with strong visibility and remediation capabilities across broad enterprise portfolios; repeatedly recognized for leadership in SAM managed services.

SoftwareOne — global scale with productized SAM service offerings that combine licensing optimization and compliance across large enterprise estates.

Crayon — execution‑focused SAM delivery with strong licensing vision and recognized global presence for managed SAM services.

Insight — emphasizes cloud cost optimization and integration with wider IT service portfolios; recently recognized in analyst evaluations for vision and execution.

Deloitte — leverages deep vendor license expertise and strong advisory capability to support transformation and compliance programs at scale.

Zluri — SaaS‑centric tooling and discovery capabilities aimed at subscription governance and rapid time‑to‑value for cloud‑first estates.

Livingstone Technologies — specialist operator focused on optimization and navigating vendor licensing changes for enterprise clients.

Softchoice — combines SAM managed services with cloud enablement and digital workplace offers, suited to North American‑centric buyers.

Recent vendor recognitions (summarized in the report) confirm market leadership and growing analyst attention, but procurement decisions should emphasize proof‑points (customer references, audit outcomes, SLA adherence) over awards alone.

The report contextualizes how recent legal and regulatory developments materially affect SAM program design. Examples include expanded state privacy regimes and rules around bulk data handling, which impose additional obligations on how providers collect, store and process software usage telemetry. These changes translate into contractual requirements (data locality, encryption, access logging), operational controls (least‑privilege access, pseudonymization) and audit evidence readiness — all of which should be scored during vendor selection.

Additionally, labor market realities mean buyers must explicitly model the cost and availability of vendor‑licensing specialists and AI tool operators as part of any managed service procurement. Our staffing profiles and cost curve scenarios help CFOs and HR partners plan resourcing and training investments for 2026–2028.

Treat SAM as a strategic control function and budget accordingly: incorporate SAM outcomes into procurement and audit committees rather than leaving it to IT operations alone.

Design contracts for data protection and audit defensibility: require explicit commitments on data handling, retention, and breach response mapped to the regulatory landscape in your footprint.

Insist on outcome‑based SLAs and transparent reporting: demand measurable KPIs (cost savings realized, compliance posture improvements, audit outcomes) and audit evidence delivery mechanisms.

Adopt a hybrid delivery stance: combine vendor automation and tooling with retained in‑house expertise for licensing strategy and vendor negotiations.

Plan for AI‑assisted operations: allocate a portion of your SAM budget to modernization (analytics, automation, anomaly detection) to reduce human effort and increase repeatability.

Validate providers against real scenarios: require vendors to run a short, scoped pilot that includes audit simulation and privacy control verification before committing to multi‑year programs.

How does our current SAM posture materially reduce enterprise audit and compliance risk under new privacy and bulk‑data rules?

Can our potential providers produce reproducible audit artifacts and attestations for data handling and license entitlements?

What portion of our cloud and SaaS spend is visible and actionable under candidate SAM deployments within 90 days?

Are commercial terms structured to shift provider incentives toward continuous optimization and audit defense?

What is our plan to retain vendor‑licensing expertise as automation grows?

How will we measure vendor performance and realize value, quarter over quarter?

This executive brief highlights the trends, practical tools and vendor considerations that PW Consulting’s full Software Asset Management Managed Service Market report delivers in depth. The full report contains the granular segmentation, downloadable forecast models, detailed vendor scorecards, case study appendices and contract templates you will need to operationalize these recommendations. To review the complete dataset and decision‑support materials, download the full report or contact PW Consulting for a tailored briefing and model walkthrough.

For enterprise leaders planning budgets, procurement cycles and governance changes in 2026, the choices made now — about vendors, operating models and contractual commitments — will determine whether SAM becomes a cost center or a strategic lever for compliance and cloud cost control. Our research shows the market is expanding rapidly; the differentiator will be disciplined selection and implementation grounded in outcomes, not tooling alone.

For detailed analysis of this topic, please visit the official page:Software Asset Management Managed Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com