PFAS-Free Paper Coating Market to Reach USD 4.68 Billion by 2034 | 9.2% CAGR

Other |

2026-06-25 11:49:31

PW Consulting today releases its authoritative market research brief on the Household Solid State Relay (SSR) market — a focused intelligence asset designed to inform executive decision-making throughout 2026. Built on a structured historical window (2020–2025) with base year 2025 and a forward-looking forecast horizon covering 2026–2032, the study synthesizes macro demand, supplier dynamics, technology trajectories, and regulatory pressures to provide a clear, prioritized set of actions for manufacturers, OEMs, component suppliers, and strategic investors.

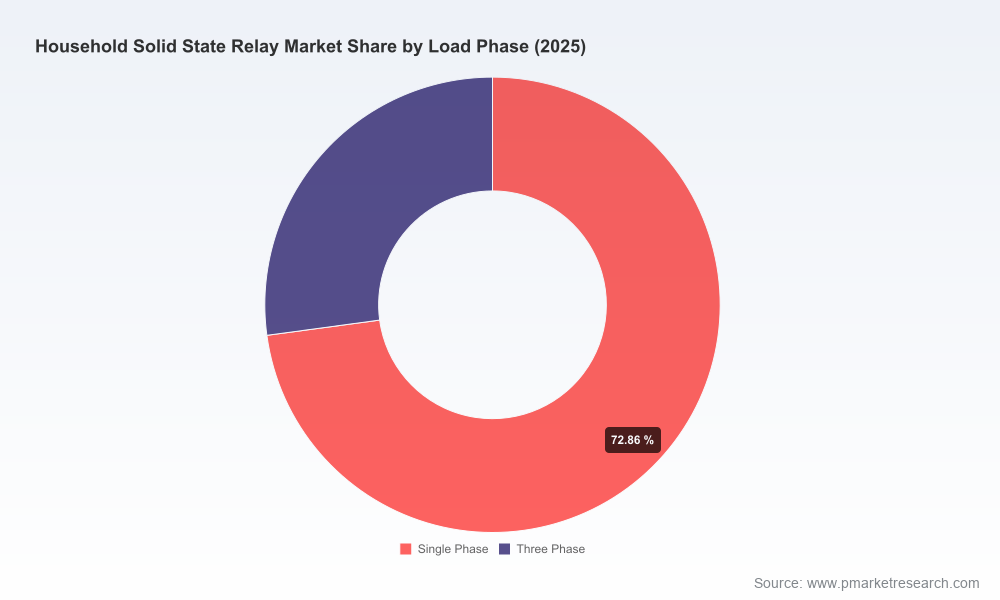

Household Solid State Relay Market

The household SSR market was modeled in USD (Million) with 2025 established as the base year. PW Consulting’s model indicates the market is growing at a compound annual growth rate (CAGR) of 7.66% across the forecast window, driven by rising smart-home penetration, electrification of household systems, and greater emphasis on silent, reliable switching in consumer applications.

Household Solid State Relay Market

Under our central case, the global household SSR market expands materially over the 2026–2032 forecast period, reflecting sustained adoption in appliance controls, lighting automation, and residential HVAC/equipment. The height of this trajectory underscores that strategic moves made in 2026 will compound value through the end of the forecast horizon.

Household Solid State Relay Market

Market concentration metrics from our competitive mapping show a moderately consolidated landscape (CR3 ≈ 32.5%; CR5 ≈ 48.2%), indicating leader-driven product and channel influence while leaving substantial pockets for specialized challengers and niche incumbents.

Timing: 2026 is a pivot year — component tariffs, critical-mineral policies, and supplier shifts are converging. The report translates these external shocks into prioritized, executable strategies so leadership teams can move from reactive to pre-emptive postures.

Risk-to-opportunity translation: We quantify exposure across sourcing, regulatory, and pricing vectors and identify where tactical investments (e.g., alternative materials, local assembly, supplier equity stakes) yield asymmetric protection and upside.

Product roadmaps and commercial alignment: The study maps performance attributes (thermal, electrical isolation, switching topology) against household use-cases and channel economics to guide R&D prioritization, SKU rationalization, and margin-recovery plans.

M&A and partnership signal: With a mid-range concentration profile, the report surfaces likely consolidation corridors — compelling targets, potential acquirers, and integration pitfalls — enabling quicker, higher-conviction M&A execution in 2026.

Quantitative market model (USD, Million) with historical tracking (2020–2025), a transparent base-year (2025), and scenario-driven forecasts through 2032. Models are provided with adjustable assumptions to stress-test strategic options.

Technology and product capability matrix linking SSR architectures (photoMOS, MOSFET, triac-based designs, zero-cross switching, etc.) to household performance needs and manufacturing complexity.

Supply chain heatmaps and tiered supplier dependency scoring (including critical-material exposure), with contingency pathways and near-term actions to insulate production from policy shocks.

Commercial playbooks: go-to-market segmentation frameworks, channel economics for appliance OEMs and smart-home integrators, pricing levers, and contract negotiation templates.

Regulatory and trade impact assessment: focused analysis of tariff scenarios, export-control disruptions, and processed-mineral policy shifts that materially affect component sourcing and landed cost.

Competitive intelligence suite: detailed profiles and capability maps for leading vendors, supplier benchmarking templates, and a curated list of potential strategic partners and acquisition targets.

Decision dashboards and a 90-day to 12-month action plan that tie research findings directly to investment, sourcing, and product development milestones.

The household SSR arena features a mix of global electrical groups, component specialists, and automation-focused suppliers. PW Consulting’s analysis highlights positional strengths and strategic moves that matter for 2026 planning.

Omron Corporation (Kyoto, Japan) — Strengths: broad SSR portfolio spanning compact PCB mount to panel solutions and deep customer access into appliance OEMs. Strategic implication: Omron’s channel reach and systems-level product development make it a likely anchor supplier for appliance manufacturers seeking integrated control solutions; competitors should expect continued investments in high-reliability, renewable-aligned variants.

Panasonic Corporation (Osaka, Japan) — Strengths: PhotoMOS and low-power SSR expertise optimized for silent switching in consumer electronics. Strategic implication: Panasonic’s product-led differentiation in low-power, small-form-factor SSRs positions it well in smart devices; rivals need to defend with cost-effective miniaturized designs or focus on higher-power, thermally robust niches.

Carlo Gavazzi (Steinhausen, Switzerland) — Strengths: DIN-rail and panel-mounted SSRs targeted at building automation and HVAC. Strategic implication: Their focus on integrated heat-management and rail-mounted form factors creates a competitive moat in installation-driven segments; manufacturers targeting installers must match ease-of-fit and on-site cooling performance.

Sensata Technologies / Crydom (USA) — Strengths: industrial-grade relays adapted for high-reliability household applications, with recent thermal and isolation upgrades. Strategic implication: Sensata’s industrial DNA gives it a premium-positioning play in high-reliability household systems (e.g., energy management); price-sensitive OEMs may instead pursue volume players or alternative architectures.

Schneider Electric, Siemens, ABB (Europe) — Strengths: systems-level offerings and smart-home/building automation integration. Strategic implication: These electrical conglomerates control channel access and specification influence in commercial-to-residential transitions; component suppliers should prioritize interoperability and certified integrations to unlock these channels.

TE Connectivity, Vishay, Littelfuse — Strengths: component-level robustness (shock/vibration, optocoupler and MOSFET SSRs, high-endurance series). Strategic implication: Their products are attractive for high-cycle consumer electronics and appliance subassemblies; partnership models that bundle design-in support will accelerate uptake.

Celduc, Fujitsu — Strengths: focused engineering for heating, motor, and consumer electronics control. Strategic implication: Niche players will remain important acquisition targets for larger vendors seeking rapid capability fills.

Product showcases and trade-show participation (notably events in 2025–2026) confirm supplier focus on thermal performance, electrical isolation, and semiconductor-enabled miniaturization — all directly relevant to household design constraints and appliance reliability demands.

Notable vendor product updates in 2025–2026 indicate a near-term cadence of improvements in thermal management and isolation characteristics, shortening windows for competitive differentiation in baseline SSR features.

Strategic planning for SSRs must now factor in material and policy concentration risks. Key considerations in 2026 include:

Single-source risk in critical inputs: the global production of certain raw materials used in optocouplers and power semiconductors is highly concentrated, creating acute exposure to export controls and licensing regimes.

Trade policy shifts: elevated tariffs and processed-minerals directives have materially increased landed costs for imported semiconductor components; these moves necessitate fresh sourcing and pricing strategies.

Recommended mitigations: pursue diversified supplier networks (including non-traditional geographies), invest in local assembly or contract manufacturing to reduce tariff incidence, evaluate substitute chemistries and semiconductor architectures, and adopt inventory and contract hedges to smooth cost volatility.

Movement toward higher-efficiency MOSFET-based SSRs and improved PhotoMOS designs for low-noise switching in residential settings.

Integration of SSRs into intelligent power modules and smart-home communication stacks; product teams must weigh the trade-off between adding digital features and keeping unit costs acceptable for mass-market appliances.

Thermal design and isolation improvements are fast becoming table stakes; differentiation will move to lifecycle reliability, certification, and ease-of-integration.

90-day: Conduct a supplier exposure audit; begin dual-sourcing negotiations for critical components; run SKU profitability triage and delay non-core new SKUs with marginal returns.

6 months: Execute targeted design-for-sourcing initiatives (material substitutions, standardization), finalize strategic supplier agreements with defined volume and quality SLAs, and pilot localized assembly tests to validate landed-cost improvements under tariff scenarios.

12 months: Advance select M&A or JV conversations supported by granular valuation scenarios from the report; scale integration of higher-reliability SSR lines for premium appliance and energy-management offerings.

PW Consulting’s Household SSR report is structured to be an operational tool for 2026: it converts market projections (USD, Million), a 7.66% CAGR, and competitive and policy signals into prioritized, executable initiatives that protect margins, sustain supply continuity, and accelerate growth in targeted household applications. The study is intentionally prescriptive — offering both the strategic thesis and the tactical steps needed to execute it — while preserving full datasets and detailed segment-level modeling for subscribers.

To access the complete datasets, segment-level forecasts, and the full suite of supplier scorecards and executable templates, please visit our report landing page. The executive summary above is a strategic trailer: it outlines the stakes and the recommended direction while reserving the full, downloadable evidence base for validated subscribers and clients preparing firm 2026 commitments.

For detailed analysis of this topic, please visit the official page:Household Solid State Relay Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com