PW Consulting Strategic Brief: Refrigerated Food Vending Machine Market — 2026 Decision Playbook

Executive summary

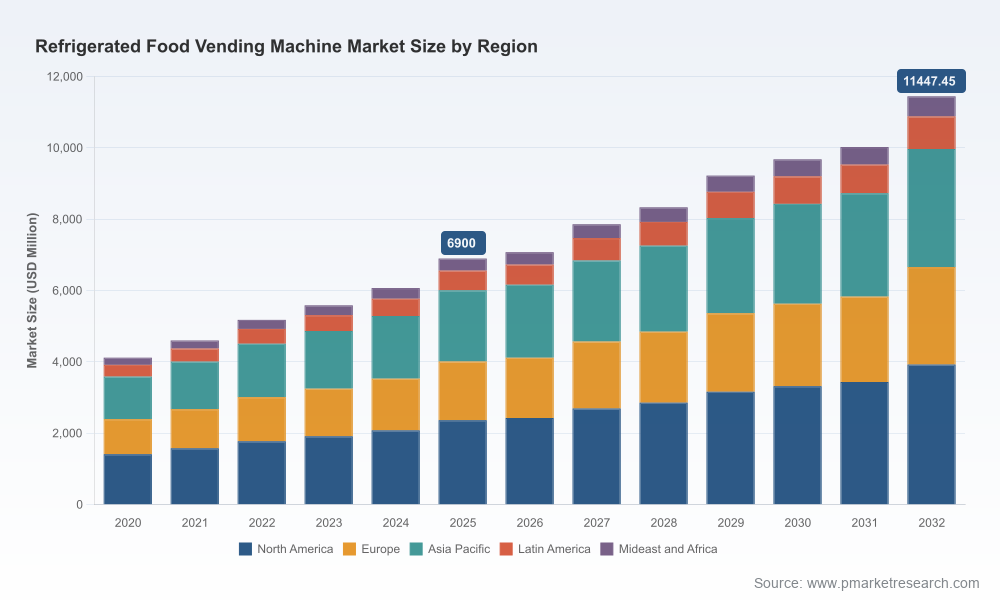

The global refrigerated food vending machine market continues to transition from niche novelty to core last‑mile foodservice infrastructure. Using 2025 as the base year, PW Consulting’s market model shows the market expanding at a compound annual growth rate (CAGR) of 7.5% over the 2026–2032 forecast window, with total market value moving from roughly USD 6.9 billion in 2025 toward the low‑double‑digit billion mark by the end of the forecast. This trajectory is driven by converging forces: tighter energy and refrigerant regulation, rising demand for fresh and chilled off‑premise meals, and rapid adoption of smart, connected vending technologies.

Refrigerated Food Vending Machine Market

Why this matters for 2026 strategy

- Regulatory imperatives are now a commercial timeline: manufacturers and large deployers face binding compliance deadlines that materially affect product lifecycles, component sourcing, and capital expenditure plans.

- Technology is shifting purchase criteria from pure equipment price to lifecycle cost, serviceability and data monetization potential — creating a premium for smarter, more efficient units.

- The market structure remains moderately fragmented (top‑3 suppliers hold under one‑third of the market and top‑5 approach mid‑40% share), so there is room for selective consolidation, strategic partnerships and differentiated product plays.

Market dynamics shaping 2026 decisions

- Regulatory pressure on refrigerants and energy efficiency. U.S. AIM Act provisions and parallel EU energy‑labeling/efficiency rules have changed the economics and permissible BOM for new builds. Manufacturers must rework refrigeration subsystems, prioritize low‑GWP refrigerants and demonstrate labeled energy performance for market access.

- Operational economics trump sticker price. Procurement teams increasingly evaluate TCO incorporating energy consumption, remote diagnostics, inventory shrinkage mitigation and servicing cadence. Units enabling remote telemetry and predictive maintenance command better uptime and lower servicing cost curves.

- Smart features enable new revenue streams. RFID, touchless payment, dynamic merchandising, and integrated media allow operators to boost per‑transaction yield and enable targeted sponsorship/advertising revenue.

- Materials and supply chains matter. Structural durability and thermal performance remain driven by traditional materials; steel continues to dominate structural decisions for hot‑and‑cold frames, which has implications for procurement risk and supplier negotiation.

- Channel and format innovation. Micro‑markets, retail partnerships, transportation hubs and institutional installations each require different product form factors, service models and approval workflows — winners will have modular portfolios and channel‑specific GTM plans.

Competitive landscape — what the leading players signal

The competitive set combines long‑standing OEMs, regional specialists and tech‑centric newcomers. Key strategic positioning we observe from public disclosures, launches and trade participation is summarized below.

Refrigerated Food Vending Machine Market

- Crane Payment Innovations (formerly Crane Merchandising Systems) — Advanced merchandising platforms and touchscreen interfaces indicate a strategy focused on premium UX, digital media monetization and reliable refrigeration for high‑turn fresh items. Strategic implication: prioritize integration of payment and content ecosystems to capture ancillary revenue.

- AMS Vendors — Specialist in low‑temperature combo units and guaranteed delivery systems; signals strength in targeted use cases where delivery reliability and temperature control are non‑negotiable. Strategic implication: partner or license proven mechanical subsystems for faster route to market.

- SandenVendo America — Emphasis on energy‑efficient refrigeration and glass‑front merchandising positions this player for environmentally conscious commercial accounts and regulated markets. Strategic implication: energy labeling compliance can be a competitive differentiator.

- REDYREF — Recent deployments of RFID‑enabled smart food fridges show the commercial viability of fully connected fresh‑meal kiosks. Strategic implication: digital inventory and frictionless access are becoming baseline expectations in premium deployments.

- Azkoyen Vending Systems — European specialist offering temperature‑controlled lines for perishables; notable for localized product designs that respond to regulatory and customer preferences. Strategic implication: localized engineering and type‑approval workflows reduce time‑to‑market in tightly regulated jurisdictions.

- Seaga Manufacturing, Fuji Electric, TCN Vending — These companies demonstrate breadth from established cold combo machines to touchscreen, adjustable cooling and global supply footprints. Strategic implication: incumbents can scale service networks rapidly; newcomers should plan selective alliances to match coverage.

Recent industry signals (selected)

- Feb 2025 — REDYREF launched and deployed an RFID‑enabled Smart Food Fridge at a commercial venue, demonstrating field readiness for fresh meal kiosks.

- May 2026 — NAMA Show highlighted AI smart vending coolers and refrigerated micro‑market innovations; multiple vendors showcased energy‑optimized models with advanced telemetry.

- May 2026 — Vendors exhibiting at Venditalia signaled accelerating cross‑market diffusion of smart refrigerated units, with an emphasis on modularity and serviceability.

Strategic recommendations for 2026 leadership teams

PW Consulting’s applied research yields seven priority moves operators, OEMs and investors should include in 2026 roadmaps.

Refrigerated Food Vending Machine Market

- Immediate compliance retrofit & SKU rationalization. Audit existing fleets and next‑generation SKUs against AIM Act and EU labeling rules. Retire or retrofit non‑compliant designs and prioritize production capacity for compliant models before the secondary sales market tightens.

- Shift procurement to lifecycle value. Re‑architect RFPs to weight energy consumption, telemetry capability, modular serviceability and spare‑parts commonality more heavily than upfront price.

- Invest in refrigeration R&D and partnerships for low‑GWP solutions. Secure compressor and heat‑exchange technology partnerships now; component lead times and qualification cycles will slow product introductions if left to the final year before enforcement milestones.

- Scale digital services as a margin lever. Deploy telemetry, inventory analytics and dynamic pricing pilots to reduce shrink, increase product turnover and create subscription or revenue‑share models with venue partners.

- Design for modular maintenance and standardization. Standardize modular cold‑packs, door assemblies and control boards to reduce mean time to repair and simplify aftermarket logistics across regions.

- Evaluate consolidation and selective M&A. Given the market’s mid‑level fragmentation, pursue tuck‑ins that add manufacturing scale, regional service coverage or software capabilities rather than only product SKU expansion.

- Operationalize sustainability and ESG reporting. Publish lifecycle energy intensity and end‑of‑life recycling pathways to win large retail and institutional contracts where procurement criteria include supplier sustainability scores.

What our report gives you — practical tools for 2026 decisions

PW Consulting’s Refrigerated Food Vending Machine Market report (base year 2025; forecast 2026–2032) is designed as an executive decision toolkit rather than a static market summary. Key deliverables include:

- Forward‑looking market model with scenario variants that test regulatory shock, energy price volatility and rapid AI adoption.

- Commercial playbooks for OEMs, operators and investors: GTM sequencing, pilot design, margin uplift levers and contract templates for revenue‑share installations.

- Supplier and component heatmaps (materials, compressors, control electronics) to prioritize procurement actions and mitigate lead‑time risk.

- Compliance checklist and label‑ready product spec templates aligned to current U.S. and EU regulations.

- Operational dashboards and unit‑economics calculators that translate equipment specs into payback periods and OPEX sensitivity by channel.

- Competitive profiles and a transaction tracker to identify partnership and M&A targets based on capability gaps and geographic coverage.

Concluding perspective — the 2026 inflection

The refrigerated food vending machine market is at an inflection: what began as mechanical product competition is rapidly becoming a contest over regulatory compliance, service economics and data‑enabled customer experiences. For decision makers in 2026, the imperative is clear — move beyond reactive product redesigns and adopt integrated strategies that align engineering, procurement, software and channel teams around lifecycle value. Those who treat compliance as a ceiling to be met will be outpaced by players who leverage the same constraints as differentiation levers (energy efficiency, lower operating costs, smarter user experiences).

Next step

PW Consulting’s full report contains the granular segmentation, interactive models and supplier matrices that operational teams need to execute the recommendations above. This brief intentionally outlines strategic direction and practical priorities while preserving the detailed sub‑segment data and downloadable decision tools for report subscribers. To access the complete dataset, scenario files and the procurement playbook, visit our official report page or contact PW Consulting’s Strategy Desk for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Refrigerated Food Vending Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com