Ocean Wave Energy Technology Market: PW Consulting Strategic Briefing — A 2026 Decision-Maker’s Roadmap

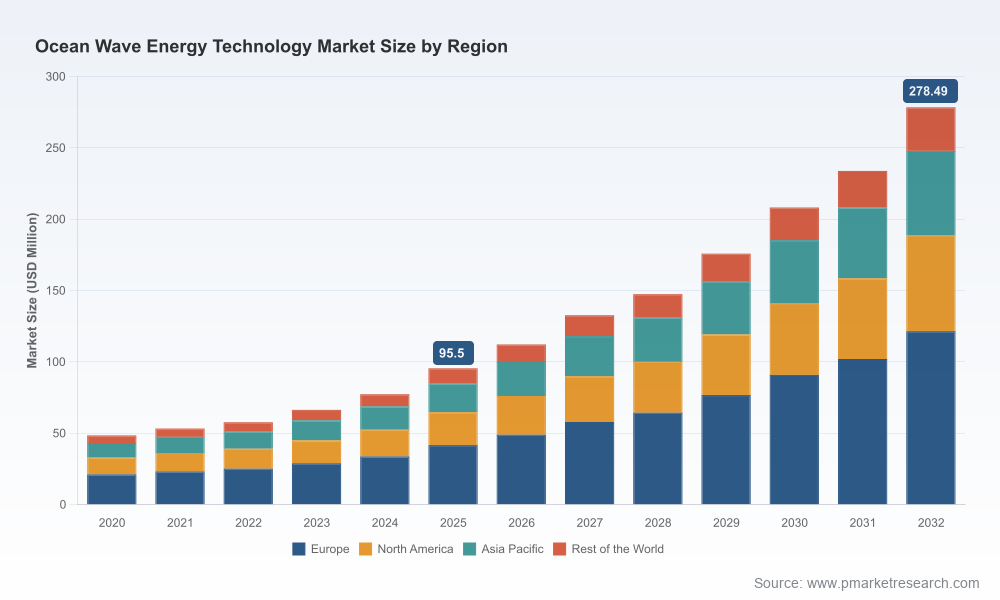

PW Consulting’s latest market intelligence on Ocean Wave Energy Technology synthesizes proprietary modeling, near-term project tracking and on-the-ground vendor due diligence to deliver a decision-ready view for corporate strategy teams in 2026. Our analysis covers the historic 2020–2025 window, anchors on 2025 as the base year and projects through 2026–2032. At the macro level, the market is on a sustained expansion trajectory — growing from a global base of roughly USD 95.5 Million in 2025, and forecast to exceed USD 278 Million by 2032 at a compound annual growth rate (CAGR) of approximately 16.52% over the 2026–2032 forecast period. This briefing highlights the report’s practical value for near-term capital allocation, partnership formation, procurement timing and regulatory engagement, while reserving proprietary segment-level datasets for report subscribers.

Ocean Wave Energy Technology Market

Why this report matters for 2026 corporate decisions

- Timing capital deployment: 2026 is a pivotal year when pilot programs transition to first commercial arrays and utility offtake contracts begin to appear onshore and offshore. Our model quantifies the short-run uptick in commissioning and supply-chain activity, enabling CFOs and project sponsors to time capex, working capital and offtake negotiations to reduce price and delivery risk.

- Technology selection under uncertainty: Multiple device families (point absorbers, oscillating water columns, attenuators and overtopping concepts) are advancing in parallel. The report synthesizes comparative performance envelopes, survivability profiles and indicative LCOE trajectories so CTOs can prioritize technology pilots most likely to meet 2030 cost and reliability targets.

- Commercial partnerships and procurement windows: With early grid connections and PPAs materializing, 2026 will separate technologies ready for scale from those that require further R&D. We map vendor maturity against procurement levers (standardized BOS packages, O&M frameworks, insurance structures) to guide executives on when to move from option-stage commercial agreements to binding commitments.

- Regulatory engagement and incentives: Several public funding and test-infrastructure initiatives are lowering early-stage risk. The report translates policy instruments and grant programs into actionable scenarios for revenue support, permitting timelines and co-investment structures.

Key takeaways: market dynamics and commercial inflection points

- Strong growth, early economics improving: The sector’s double-digit CAGR reflects both rising deployment activity and accelerating technology maturity. While absolute installed volumes are still small versus other renewables, unit economics are improving meaningfully as manufacturers move from single-site pilots to repeatable product lines and aggregated procurement reduces BOS costs.

- Project pipeline is clustering around test hubs: Concentrated test sites and national test centres are serving as convergence points for pilots, scale demonstrations and early PPAs. These hubs reduce permitting friction and concentrate O&M experience, which in turn shortens the learning curve for developers and insurers.

- Supply-chain winners will be those solving survivability and maintainability: Hardening PTO systems, accessible modular components, and composite-based hull structures have emerged as critical differentiators. Expect procurement RFPs to include lifecycle performance KPIs and maintenance access requirements as standard.

- Funding and offtake catalysts: Public funding mechanisms and early utility PPAs are materially derisking early projects and enabling anchor customers to form. These public-private instruments are the trigger for institutional capital to consider the space on a risk-adjusted basis.

Competitive landscape: who matters and why

The vendor landscape remains dynamic and geographically diverse, populated by technology specialists whose device concepts and commercial strategies differ substantially. Leading players include established device developers focused on grid-connected pilots, diversified engineering firms pursuing hybrid platforms, and newer entrants delivering novel PTO and submersible architectures. Below we summarize strategic positioning without disclosing confidential contract-level details.

Ocean Wave Energy Technology Market

- Eco Wave Power — A specialist in onshore floater systems that leverage existing marine structures. Recent milestones include U.S. pilot completion at the Port of Los Angeles (achieving program milestones in collaboration with energy partners) and a successful onshore project launch that demonstrates low OPEX ratios versus CAPEX. For companies seeking low-permitting pathways and shoreline asset integration, Eco Wave’s model is a compelling case study.

- CorPower Ocean — Developer of compact point-absorber devices characterized by high wave-to-wire efficiencies and robust survivability. Commercial-scale deployments and storm survivability testing at European test sites illustrate a pathway from single-unit testing to array-level operations; their device architecture is attractive for high-energy deployment sites where power density matters.

- Carnegie Clean Energy — Known for integrating wave power with desalination, presenting combined-value propositions for island, remote and industrial water markets. Their hybrid value chains are pertinent to corporate buyers evaluating multi-service project economics.

- Ocean Power Technologies (OPT) — Focused on PowerBuoy systems and PTO innovations for reliable generation. OPT demonstrates the importance of ruggedized PTO and long-duration survivability for utility and remote applications.

- AW-Energy, Mocean Energy, Oscilla Power, CalWave, ORPC, Seabased, NoviOcean, Marine Power Systems — Each brings differentiated IP: nearshore surge converters, high-energy ocean machines, drivetrain advances for 1 MW-class systems, submerged multi-DOF capture, cross-flow adaptability, linear seabed generators, and floating non-resonant absorbers. Strategic partnerships and pilot-to-commercial pathways vary; selecting the right collaborator depends on site regime, offtake profile and CAPEX tolerance.

Recent developments that change the 2026 agenda

- Completion of high-visibility pilots and inaugural U.S. onshore projects has demonstrated operational learnings and unit-level O&M economics that institutions and utilities can analyze for underwriting decisions.

- The first continental U.S. PPA for wave power (covering output from a major West Coast test facility) and expanded federal funding windows are accelerating the move from demonstration to commercial procurement.

- Device survivability trials and material innovations (notably composite hulls and advanced drivetrain concepts) have materially reduced technical uncertainty in severe sea states, shifting risk appetite among insurers and lenders.

Practical contents of the PW Consulting report (what you get)

- Scenario-driven market sizing and revenue forecasts (2026–2032) with sensitivity runs reflecting deployment pacing, capex decline, and policy scenarios.

- Technology deep dives comparing wave-to-wire efficiency bands, survivability outcomes, expected O&M profiles and indicative LCOE pathways for representative device classes.

- Supply-chain heatmaps identifying critical vendors for composites, PTO subsystems, mooring and subsea electrical infrastructure, plus procurement timing recommendations.

- Project-level case studies and checklist templates for permitting, community engagement, insurance clauses and contractor selection — built to be drop-in usable for bid teams.

- Commercial playbooks: contracting strategies, PPA term structures, co-investment models, and sample term-sheets for technology licensing and hybrid project SPVs.

- M&A and partnership mapping highlighting likely consolidation vectors and criteria for strategic investment, plus a shortlist of target capabilities for roll-up strategies.

How corporate leaders should use this intelligence in 2026

- Portfolio prioritization: Use our comparative device and site analytics to select a mix of low-risk shoreline and higher-yield offshore exposure that aligns with corporate risk-return profiles.

- De-risk via staged commitments: Negotiate optioned supply agreements and staged capacity purchase commitments tied to technical milestones rather than fixed-capacity buys to preserve flexibility.

- Leverage public funding: Align pilot timelines with grant windows and test-facility availability to maximize cost-sharing and shorten time-to-revenue for demonstration projects.

- Standardize procurement KPIs: Include maintainability, retrieval time, component modularity and insurance-backed performance guarantees in RFPs to avoid scope creep and retrofit costs.

Why PW Consulting’s methodology matters

Our findings are the product of multi-layered triangulation: device-level engineering performance models, verified project trackers, supplier interviews, and policy mapping. We layer conservative, base and upside deployment scenarios to provide a bounded view of market outcomes and to identify strategic inflection points where corporate action changes payoff materially. To preserve the utility of this briefing while protecting proprietary, project-level intelligence, the report intentionally limits public dissemination of granular segmentation tables and individual contract terms; however, subscribers receive the full datasets and model workbooks for bespoke scenario analysis.

Ocean Wave Energy Technology Market

Next steps and how to access the full analysis

For corporate strategy teams preparing budgets, procurement roadmaps or investment committees in 2026, the full PW Consulting Ocean Wave Energy Technology Market report provides the datasets, playbooks and vendor scoring you will need to act with confidence. The report includes downloadable scenario models and an executive workshop package we can deliver to align your internal stakeholders around a phased market-entry or scale-up plan.

To license the full report, schedule a briefing, or request custom modelling tailored to your portfolio, please visit the official PW Consulting report page or contact our market team directly. Detailed segmentation, project-level contracts and proprietary vendor scoring are available to subscribers and clients under standard non-disclosure terms.

PW Consulting — translating emerging ocean energy science into 2026-ready commercial strategy.

For detailed analysis of this topic, please visit the official page:Ocean Wave Energy Technology Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com