Traumatic Brain Injury Treatment Market Size, Share, Trends, and Industry Forecast by 2032v

Other |

2026-06-08 06:45:29

PW Consulting’s End Stage Renal Disease (ESRD) Market report, published ahead of Q1 2026 planning cycles, distills a complex and fast-evolving sector into decision-ready intelligence for corporate strategy, commercial teams, and investors. Our analysis synthesizes historical performance, regulatory inflection points, competitive positioning, and technology adoption dynamics to frame the strategic choices that will define winners and laggards through the 2026–2032 forecast horizon.

End Stage Renal Disease Market

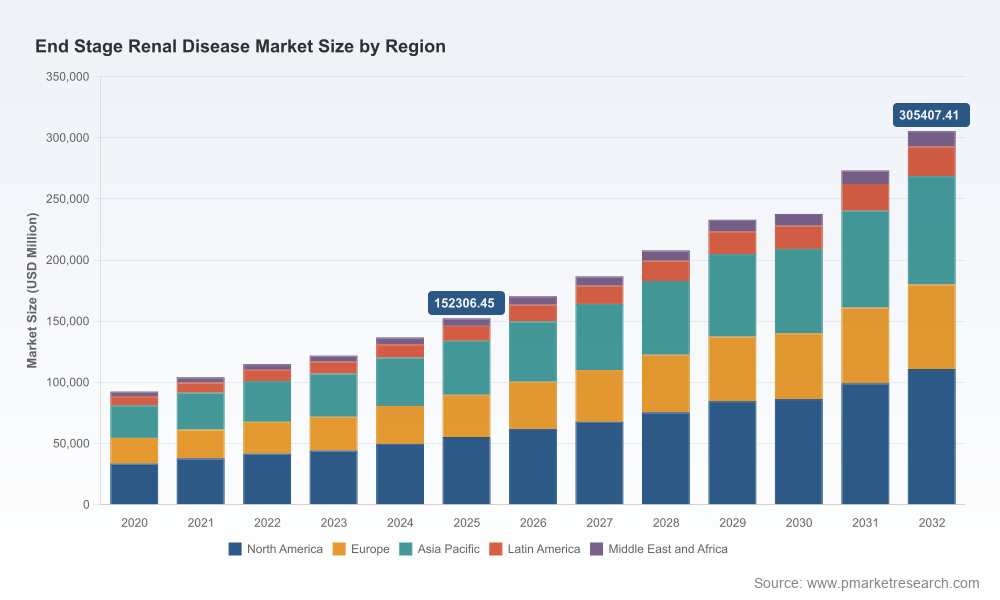

At the macro level, the ESRD market reached a significant milestone in 2025 and is projected to nearly double within the 2026–2032 forecast window, reflecting a compounded annual growth rate of 10.45% for that period. The combination of durable demand, rising clinical adoption of advanced modalities, and renewed policy-level reimbursement clarity creates both runway and complexity for market participants. Our report is tailored to help executives convert that complexity into actionable roadmaps without exposing proprietary segment-level datasets in this preview.

End Stage Renal Disease Market

Timing and fidelity: Organizations must reconcile near-term regulatory shifts with multi-year product and commercial plans. Our report aligns 2026 operational plans with projected market growth and scenario stress-tests, enabling companies to prioritize investments that yield the highest risk-adjusted returns.

End Stage Renal Disease Market

Capital allocation: With market scale expanding materially over the forecast horizon, prioritizing R&D, manufacturing footprint, and M&A requires calibrated projections. PW Consulting’s financial models quantify the relative return profiles of growth levers while preserving confidentiality around detailed segment monetization.

Market access and reimbursement strategy: Recent reimbursement updates and payment policy finalizations require rapid policy-to-pricing translation. The report maps how payment mechanics and bundled care dynamics will influence price realization and unit economics across channels.

Competitive differentiation: Leading and challenger companies are racing on product innovation, integrated care models, and go-to-market design. Our competitive playbooks identify tactical moves to protect share, accelerate adoption in prioritized channels, and capture higher-margin adjacencies.

PW Consulting’s base-year anchoring (2025) and 2026–2032 forecast scenario work show consistent expansion driven by three mutually reinforcing forces: aging demographics and rising ESRD prevalence, faster uptake of home and high-efficiency in-center modalities, and an accelerating cadence of product innovation across devices, consumables, and service models. Under our central forecast, the market’s momentum in 2026 sets the stage for robust revenue progression through 2032, reflecting a compound annual growth rate of 10.45% over the forecast period.

The growth profile is not uniform; it is shaped by regulatory changes, reimbursement resets, and capacity shifts across outpatient and hospital settings. PW Consulting quantifies the sensitivity of market value to variations in reimbursement rates, device adoption curves, and the speed of home-therapy penetration — inputs that are packaged into scenario dashboards in the full report.

Reimbursement alignment: The CY 2026 ESRD Prospective Payment System final rule provides updated clarity for base payments and payment composition. PW Consulting models the operational implications of the most recent final rule for a spectrum of provider and manufacturer business models, translating headline rate changes into bottom-line impacts under different throughput and cost structures.

Bundling and clinical scope: Policy decisions made in 2024–2025 around drug bundling and oral renal products remain operative and continue to influence procurement and contracting strategies. Our analysis shows how bundle scope alters incentives for therapy mix and supplier negotiations.

Labor and wage-index effects: Wage-related mechanics embedded in recent rulemaking create asymmetric effects across geographies and facility types. The report includes a regionally informed framework for forecasting margin pressure under alternative labor scenarios.

Acute/AKI alignment: Payment parity in certain settings (e.g., AKI dialysis rate alignment) has implications for channel substitution and hospital-vendor relationships. We quantify how short-term revenue shifts could ripple into long-term modality portfolios.

The ESRD ecosystem remains a mix of scale incumbents, specialty manufacturers, and technology disruptors. Market concentration metrics indicate a meaningful presence of top players while leaving room for competitive disruption. In this report we profile the strategic positioning, capability stacks, and near-term product roadmaps of the most consequential companies — from large integrated dialysis providers to agile medtech entrants — and assess where cooperation, consolidation, or head-to-head competition is most likely.

Scale incumbents: Established global providers maintain advantage through integrated care networks, procurement depth, and installed base economics. Their strategic emphasis is shifting toward value-based care programs and full-service delivery models to protect long-term patient relationships.

Device and consumables leaders: Firms with durable manufacturing and distribution footprints retain strong aftermarket revenue streams. Their competitive choreography includes iterative product upgrades, supply-chain redundancy, and selective vertical integration.

Disruptors and digital entrants: A new wave of innovations — compact all-in-one dialysis platforms, cyber-hardened networked systems, and home-enablement technologies — is creating pathways to displace legacy devices in specific care settings. Recent regulatory clearances have accelerated commercial timelines for several of these entrants.

Notable recent developments we examine in depth include the commercial plans of major dialysis platform vendors, FDA-clearance-driven launches for next-generation systems, and annual reporting that signals strategic emphasis on value-based care and modality diversification. The full report contains proprietary scoring of each major competitor across product, channel, regulatory-readiness, and financial-resilience dimensions.

Executive playbooks for manufacturers, providers, and investors: tactical 12–36 month moves and contingency plans tied to reimbursement and adoption scenarios.

Integrated financial models and sensitivity analyses: enterprise-impact view of price, volume, and cost drivers (provided with regional and modality toggles in the full dataset).

Commercial go-to-market templates: channel segmentation, contract levers, and sales-force alignment recommendations to accelerate uptake in target settings.

Regulatory impact heatmaps: reconciled implications of the latest policy pronouncements and recommended advocacy priorities.

M&A and partnership pipeline: prioritized target profiles and valuation heuristics for bolt-on acquisitions, licensing, and strategic alliances.

Supply-chain and manufacturing risk assessment: resilience checks and mitigation playbooks for consumables and device production.

Technology adoption frameworks: decision matrices for disruptive platforms, home therapy enablement, cybersecurity readiness, and service-layer monetization.

Prioritize modular investments that preserve optionality. Given the forecast growth and policy fluidity, firms should design product and commercial investments that can scale across care settings without large stranded costs.

Accelerate interoperability and cybersecurity investments for networked dialysis systems. Recent clearances underscore that enterprise-grade connectivity is becoming a baseline requirement rather than a differentiator.

Align pricing strategies to bundled care models. Cross-functional teams (commercial, regulatory, clinical) must stress-test pricing under alternate bundle definitions to avoid margin erosion.

Use M&A selectively to fill capability gaps. Targets that bring either home-therapy enablement, differentiated consumables, or service delivery capabilities offer the quickest path to higher blended margins.

PW Consulting’s ESRD market model synthesizes historical time-series, regulatory filings, company disclosures, and primary interviews with payers, providers, and product leaders. Our base-year calibration is 2025; the report provides transparent model logic and scenario mechanics that allow clients to customize assumptions. To preserve competitive confidentiality in this briefing, we have deliberately excluded line-item segment tables and regional breakdowns — these are available in the full report package.

This briefing is a strategic preview. The full PW Consulting End Stage Renal Disease Market report delivers the granular regional and modality-level forecasts, proprietary segmentation, and interactive financial workbooks necessary for immediate incorporation into 2026 corporate planning. For access to the complete dataset, model workbooks, and bespoke consulting engagements, please visit our report landing page or contact your PW Consulting account representative. Organizations seeking an expedited executive workshop to translate findings into a 90-day action plan should request our planning sprint offering.

PW Consulting remains committed to delivering market insight that balances transparency with commercial prudence. This briefing is intentionally curated to demonstrate the analytical depth and practical orientation of the full report while reserving sensitive segment-level detail for subscribing clients and workshop participants.

For detailed analysis of this topic, please visit the official page:End Stage Renal Disease Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com