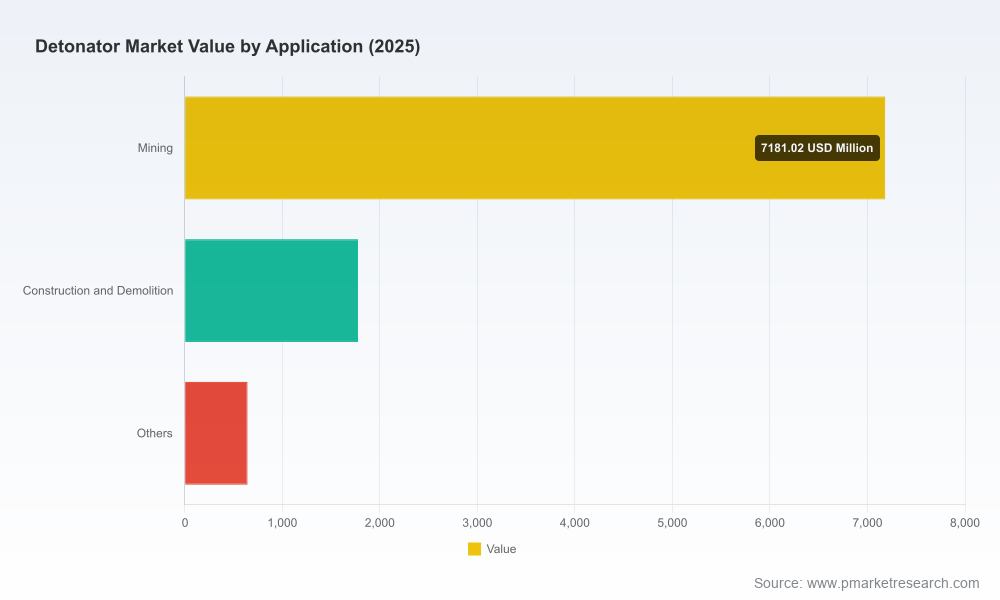

PW Consulting: Detonator Market to Grow from USD 9.6B in 2025 to USD 12.03B by 2032 at 3.42% CAGR — North America, Electric Detonators and Mining Lead Demand

Other |

2026-06-30 16:55:58

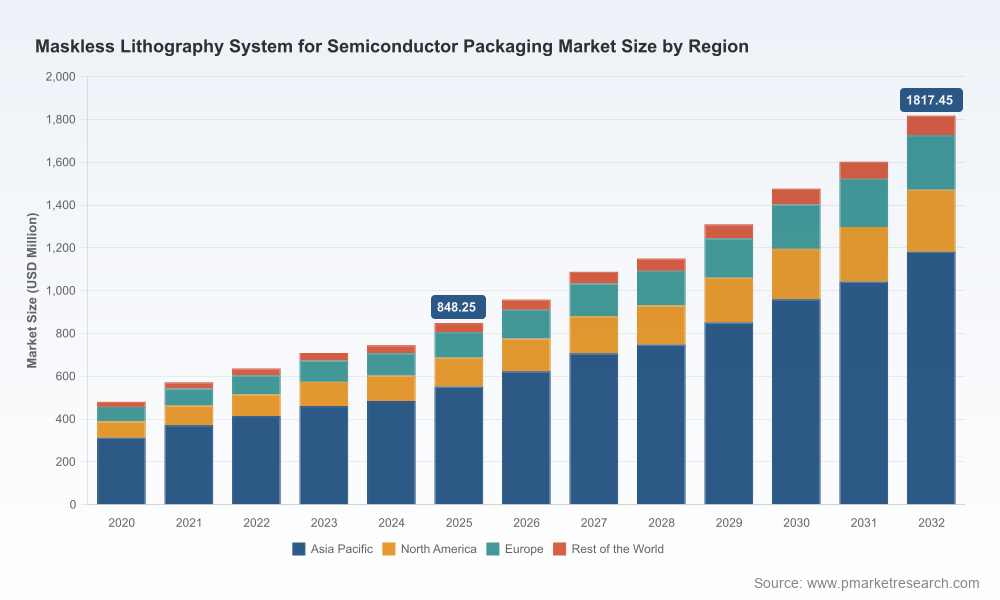

PW Consulting’s latest market research on Maskless Lithography Systems for Semiconductor Packaging positions this technology as a strategic inflection point for companies defining their 2026 investment and product roadmaps. Built on a 2025 base-year assessment and a 2026–2032 forecast horizon, the study quantifies a clear growth trajectory: the global market expands from a mid‑2020s base into a near‑billion dollar opportunity in 2026 and beyond, supported by a robust compound annual growth rate of 11.48% across the forecast window. This preview explains why those topline metrics matter to C‑suite and product leaders, and what operational and go‑to‑market choices they should be prioritizing now.

Maskless Lithography System For Semiconductor Packaging Market

Timing: Advanced packaging cycles in AI, HPC, 5G and automotive are moving from pilot to high‑mix production. Maskless lithography’s ability to remove photomask lead times and enable rapid iteration aligns directly with customers’ need for agility—turning time‑to‑value into a competitive differentiator.

Maskless Lithography System For Semiconductor Packaging Market

Scale and economics: With the market set to breach near‑billion dollar scale in the first forecast year and expand at double‑digit CAGR thereafter, maskless solutions transition from niche R&D tools to capital equipment line items that require formal CapEx planning, supplier qualification, and integration roadmaps.

Maskless Lithography System For Semiconductor Packaging Market

Concentration and supplier power: The market demonstrates meaningful consolidation with a high top‑tier share concentration, creating a landscape where a handful of established vendors materially shape technology roadmaps, channel access, and standards adoption. Procurement and partnership strategies must therefore be calibrated to interact effectively with this upper tier.

Heterogeneous integration & chiplets: The move to disaggregated dies and 2.5D/3D integration is generating requirements for stitch‑free, high‑resolution patterning across warped or large‑format substrates—scenarios where maskless approaches particularly excel.

Process flexibility and speed: Maskless systems remove photomask fabrication lead times and enable rapid customizations (die‑shift compensation, local adjustments), supporting both prototyping and mid‑to‑high volume manufacturing cases where design iteration velocity is paramount.

Enabling technologies: Advances in solid‑state light sources, spatial light modulators (SLMs), and real‑time warpage/die‑shift correction are reducing cost of ownership and increasing throughput—closing the gap versus traditional mask‑based lithography on both performance and sustainability metrics.

Supply chain & geopolitics: Equipment flows remain influenced by global semiconductor trade dynamics. Key vendors are concentrated across Germany, Austria, Japan and the US, while demand is centered in Asia’s advanced packaging ecosystems. Buyers must therefore balance technical fit with supply resilience.

The market’s top vendors fall into two broad cohorts: established global optics and equipment houses bringing projection/SLM expertise, and specialised maskless innovators optimised for packaging workflows. Each group offers distinct value propositions for OEMs, OSATs, and integrated device manufacturers.

Heidelberg Instruments (Heidelberg, Germany; https://heidelberg-instruments.com) — Known for the MLA series, Heidelberg targets wafer‑level packaging needs with systems that emphasize rapid design change, die shift compensation and micron‑scale resolution suitable for mid‑to‑high volume manufacturing without photomasks.

EV Group (EVG) (St. Florian, Austria; https://www.evgroup.com) — EVG’s LITHOSCALE platform and MLE technology focus on high throughput and stitch‑free full‑wafer patterning for heterogeneous integration. Recent trade‑show highlights reinforce EVG’s push toward production‑grade maskless exposure tailored to chiplet and probe card applications.

Nikon Corporation (Tokyo, Japan; https://www.nikon.com) — With systems such as the DSP‑100, Nikon brings SLM‑based direct projection with sub‑micron line/space capability, warpage correction and large‑substrate support—signaling a push to capture back‑end packaging workflows at scale.

SCREEN Holdings (Kyoto, Japan; https://www.screen.co.jp) — SCREEN advances laser direct imaging and maskless systems oriented to IC package substrates, offering a throughput‑focused play aimed at communications and IoT segment production needs.

SÜSS MicroTec (Garching, Germany; https://www.suss.com) — SÜSS integrates maskless exposure within broader lithography portfolios, targeting specialty and flexible integration processes where process adaptability and substrate compatibility are differentiators.

In‑Vision Technologies AG (Austria; https://in-vision.at) — A specialist in digital light engines, In‑Vision positions maskless patterning for micron‑scale wafer and panel‑level applications without photomasks.

Applied Materials (with Ushio) (Santa Clara, USA; https://www.appliedmaterials.com) — By collaborating on Digital Lithography Technology for large glass and package substrates, Applied Materials points toward integration with heterogeneous integration and high‑performance chiplet architectures.

Regional & emerging suppliers — Select Chinese and Japanese providers are advancing direct‑write and maskless offerings to meet local demand, increasing competitive pressure on cost and local service coverage.

Nikon opened orders for a production‑oriented DSP‑100 system, underscoring SLM‑based approaches for large substrate back‑end lithography (orders opened mid‑2025).

EVG showcased the LITHOSCALE XT variant at major trade events through 2025–2026, promoting multi‑fold throughput gains and explicit production positioning for chiplet and advanced packaging use cases.

Heidelberg published application updates on MLA series capabilities for die‑shift and warpage compensation in AI/HPC packaging contexts, reiterating maskless suitability beyond prototyping.

This study is structured to move readers from market context to executable decisions. Key deliverables include:

Market sizing and forward scenario modelling — granular topline forecasts across a 2026–2032 horizon with sensitivity analyses for throughput improvements, adoption curves, and regional demand scenarios.

Commercial playbooks — procurement decision trees, qualification checklists, supplier scorecards, and recommended contractual guardrails to manage uptime, upgrade paths, and IP interoperability.

Technology maturity maps — comparative assessments of laser direct imaging, SLM/projection approaches, and other maskless light sources against metrics that matter for packaging (resolution, stitchability, warpage correction, throughput, TCO).

Use‑case economics — CapEx/Opex models for green‑field fabs and retrofit lines, break‑even analyses for replacing mask‑based flows, and throughput thresholds where maskless becomes accretive.

Competitive benchmarking — vendor capability matrices, commercial positioning, and go‑to‑market implications designed for OEMs, OSATs and tool vendors weighing partnerships or technology investments.

Roadmaps & risk register — timeline recommendations for pilot→scale transitions, technology risk categorizations (supply, manufacturing readiness, standards), and mitigation strategies.

For equipment OEMs: accelerate modular product roadmaps that pair high‑resolution optical engines with adaptive software (real‑time correction, recipe portability). Consider channel partnerships where regional service footprint is a gating factor.

For OSATs and IDM back‑end teams: build pilot programmes now to validate throughput and overlay strategies; establish preferred supplier lists with options for co‑development to secure roadmap alignment.

For investors and corporates: prioritize companies demonstrating scalable throughput improvements, service coverage, and software‑first approaches that enable rapid customer integration; monitor concentration metrics that indicate barriers to new entrants.

Align CapEx cycles to product maturity: use our threshold tables to determine when maskless transitions from a tactical benefit to a strategic production asset for your lines.

Negotiate outcome‑based contracts: performance‑linked service agreements (uptime, overlay accuracy, upgrade paths) de‑risk adoption and align incentives with vendors.

Invest in systems integration capabilities: the value of maskless lithography accrues to organizations that can integrate optics, metrology, and automation into repeatable manufacturing recipes.

PW Consulting’s report synthesizes the market evidence, vendor intelligence and operational playbooks needed to make defensible 2026 decisions. With the market entering an accelerated growth phase and a concentrated vendor base shaping standards and product roadmaps, organizations that move from pilots to production‑grade adoption with clear procurement, integration and risk mitigation plans will capture disproportionate value.

For access to the full dataset, vendor scorecards, detailed modelling scenarios and the actionable playbooks referenced here, please consult the full report on our website. The preview above is intentionally selective: it outlines strategic direction and operational imperatives while guiding qualified readers to the source for the complete, segmented intelligence necessary for procurement and investment execution.

For detailed analysis of this topic, please visit the official page:Maskless Lithography System For Semiconductor Packaging Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com