How Industrial Safety Regulations Are Fueling the Cut-resistant Gloves Market

Gardening |

2026-06-30 12:52:56

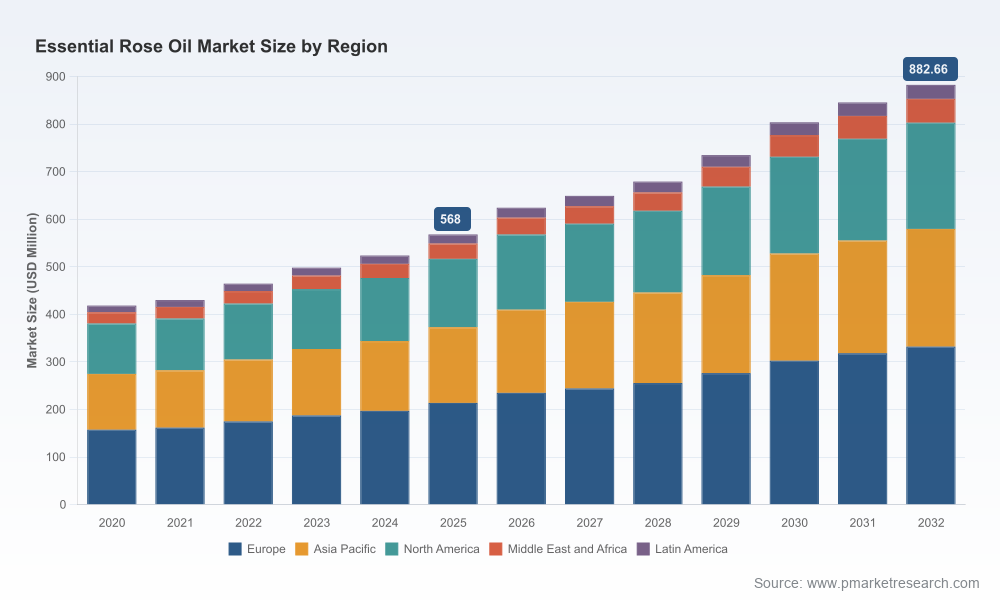

PW Consulting’s Essential Rose Oil Market study (base year 2025) arrives at a decisive moment for commodity and ingredient strategists. After expanding from a mid-single‑hundreds million USD market in 2020 to an estimated USD 568.0 Million in 2025, the sector is projected to continue robust growth into the next decade — the report’s forecast horizon shows expansion toward the high‑single to low‑triple‑digit millions by 2032 at a compounded annual growth rate of 6.5% (2026–2032). For executives planning 2026 investments, sourcing commitments, product roadmaps or M&A activity, this research delivers the market, operational and risk intelligence required to convert growth into margin and resilience.

Essential Rose Oil Market

Demand and premiumization converge. Rising consumer appetite for natural, origin‑transparent and organic fragrances and aromatherapy applications continues to lift willingness to pay for traceable rose oil variants. This structural demand trend intersects with growing interest from pharmaceutical and high‑end F&B formulators seeking certified natural aromatics.

Essential Rose Oil Market

Supply-side constraints persist. Rose oil remains one of the most labor‑intensive essential oils: conventional industry estimates indicate that several thousand kilograms of rose petals are required to yield a single kilogram of oil. Production is highly concentrated in traditional cultivation geographies, harvested in a short seasonal window with a large, predominantly seasonal workforce. These characteristics amplify the sector’s sensitivity to labour availability, weather shocks and price volatility.

Essential Rose Oil Market

Price and premium signalling. Market participants have seen dramatic price moves in recent seasons — for example, biological Bulgarian rose oil reached premium price levels in 2024 — underscoring how certification, traceability and vintage can materially affect supplier economics and buyer margins.

Consolidation and concentration dynamics. The market exhibits a moderate top‑player concentration: the three- and five‑firm concentration ratios point to meaningful scale among leading houses while leaving room for specialist growers and niche organic producers to capture premium segments. This structure shapes strategic choices about vertical integration, long‑term contracting and partnership models.

Our research is designed as an operational toolkit for 2026 planning cycles. Beyond market sizing and trend narrative, the report contains:

Executive dashboard with macro scenarios (baseline, upside, downside) and a short‑list of contingent triggers that should change procurement/tactical posture within a 6–18‑month window.

Supply‑chain heat map and supplier segmentation framework that classifies producers and distillers by scale, certification profile, traceability and risk exposure (labor, climate, regulatory).

Price‑shock and margin sensitivity models calibrated to harvest seasonality and input cost drivers — model templates are provided so teams can plug in their own contract terms and run what‑if analyses.

Sourcing playbook and contractual clauses (term sheets) for securing long‑dated supply while preserving flexibility to capture spot premiums or switch suppliers when quality or sustainability metrics deviate.

ESG & traceability implementation checklist including traceability milestones, audit cadence, certification mappings (organic, bio‑trade and GI considerations) and an estimated capex/Opex roadmap for upstream investments (fields, distillation upgrades, farmer cooperatives).

M&A and partnership framework highlighting target archetypes (capacity consolidators, certified organic producers, downstream integrators) and an annotated shortlist of due‑diligence questions tailored to rose oil operations.

Commercial playbook for product and price positioning across fragrance, aromatherapy, pharmaceutical and F&B applications, including go‑to‑market options for single‑origin versus blended claims.

The market map in our study separates the value chain into three roles: primary growers/distillers, specialist processors and global flavor & fragrance houses. Each exhibits distinct strategic priorities and levers.

Primary growers and distillers (notably a cluster of established producers in traditional growing regions) retain direct control over raw‑material quality and harvest timing. Producers with integrated field ownership and proprietary distillation capability are advantaged in traceability and certification roll‑outs; they are natural partners for buyers seeking secure, certified supply chains.

Specialist processors and certified organic houses have leaned into premium niches. Their value proposition is homogeneity, certification and documented chain‑of‑custody. They often command a pricing premium and are attractive targets for strategic offtake agreements or bolt‑on acquisitions by larger buyers.

Large global fragrance and flavor companies operate at scale and increasingly prioritize sustainable sourcing and innovation. Their strategic moves — from public sustainability commitments to targeted acquisitions — signal an expectation that secured, certified supply will be a differentiator in formulations and customer offers.

Selected recent moves illustrate the direction of travel and the strategic implications for buyers and investors:

Major industry players have publicly articulated multi‑year sustainability and sourcing strategies, signalling continued demand for ethically sourced and certified rose oil. These strategies raise the bar for traceability and will increasingly be reflected in procurement scorecards.

Certification milestones among regional producers indicate a bifurcation: premium certified supply is expanding but remains constrained relative to total demand, reinforcing a two‑tier market structure.

Acquisition activity by established distributors and ingredient houses demonstrates a push to broaden portfolios and secure distribution channels — an important consideration for any buyer evaluating forward integration versus dependency on third‑party suppliers.

Operational investments by mid‑sized organic producers to scale certified cultivation and distillation capacity point to a maturing supply base, but ramp timelines remain long and capital intensive.

Companies that translate growth into durable advantage will do three things well: secure supply with differentiated terms, sharpen product and price segmentation, and build operational resilience. Our recommended actions are specific and executable:

Lock in diversified, traceable supply: blend long‑term offtake agreements with capacity‑building partnerships (cooperatives, contract farming) to secure harvest volumes while sharing investment and certification costs with suppliers.

Prioritise certification where it delivers margin: identify SKUs and channels where organic/ethical claims are value accretive, and concentrate certification investments there rather than across the entire supply base.

Use financial hedges and product design to manage volatility: adopt layered pricing strategies (fixed, index‑linked, and call/put structures) and reformulate where appropriate to reduce single‑raw‑material exposure without compromising brand promise.

Assess strategic M&A selectively: targets that offer high traceability, scalable distillation or access to certified field acreage provide the quickest route to supply security; but pay close attention to labour and seasonality risks during due diligence.

Embed community and workforce strategies: given the seasonal and labour‑intensive nature of harvesting, supplier resilience depends on workforce availability and social licence — invest in local skills, mechanisation where feasible, and community programmes to stabilise supply.

Operational readiness for seasonality: ensure inventory and logistics plans are stress‑tested against late or early harvests and regulatory/transport disruptions during the narrow harvesting window.

Procurement teams will find the supplier scorecards and contract playbook immediately useful for RFP and negotiation rounds. R&D and brand teams can use the application roadmaps and sensory‑positioning guidance to prioritise product development resources. Corporate strategy and M&A will benefit from the target archetypes, valuation drivers and scenario models to accelerate deal screening. Sustainability teams will use the traceability templates and certification gap analysis to shape 3‑year implementation plans.

Critically, the PW Consulting report balances market context with executable artefacts — spreadsheets, clause libraries and assessment templates — so that the output translates directly into board papers, procurement tenders and integration plans.

The essential rose oil market is neither niche nor commodity in the classical sense: it is a specialty ingredient market shaped by seasonality, origin value, certification and an evolving set of industrial buyers. Growth is visible and sustained, but so are supply‑side constraints and price cyclicality. Firms that act in 2026 to secure traceable supply, prioritise certification where it creates margin, and embed operational resilience will capture sustainable competitive advantage.

PW Consulting’s Essential Rose Oil Market report provides the granular tools and scenario models boards and operational teams need to make those decisions. For access to the full dataset, segmented analytics, supplier lists and downloadable financial models, consult the report landing page and implement the tailored playbooks that are included as annexes. The headline is clear: 2026 is the year to convert rising demand for premium, verifiable rose oil into secure margins and resilient supply chains.

For detailed analysis of this topic, please visit the official page:Essential Rose Oil Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com