Buy 10k Gold Jewelry in Texas USA | Best 10k Gold Diamond Jewelry Store-Gold Bar Jeweler

Shopping |

2026-06-05 09:18:20

PW Consulting’s latest market research on the Digital Inclinometer Market provides a pragmatic, board-level blueprint for 2026 decision‑makers. With the market estimated at USD 342.7 Million in the base year (2025) and forecast to expand at a compound annual growth rate (CAGR) of 6.3% through the 2026–2032 horizon, firms face a near-term environment of dependable, technology‑led demand and medium‑term strategic inflection points. This preview explains why the report is essential for product, commercial, and M&A strategies in 2026 — while intentionally reserving detailed segment tables and proprietary scenario outputs for the full report.

Digital Inclinometer Market

Actionable market sizing and forecasting: A clear top‑down and bottom‑up view of historical performance (2020–2025) and a modeled forecast (2026–2032) calibrated to macro drivers. The methodology, assumptions, and sensitivity cases are provided so teams can re-run scenarios against corporate planning assumptions.

Digital Inclinometer Market

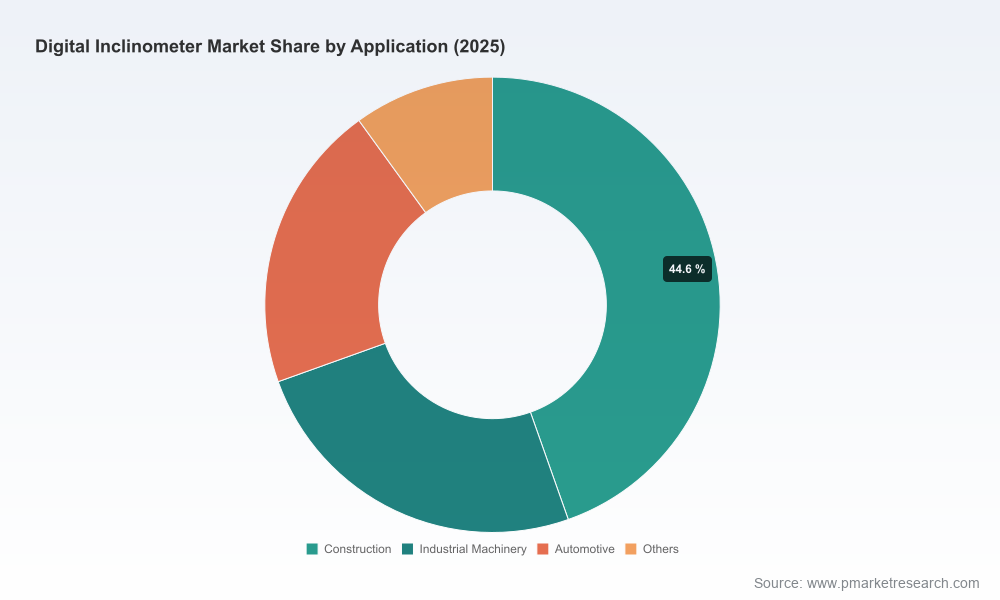

Demand driver mapping: Granular qualitative analysis of the structural use‑cases that sustain adoption — from structural health monitoring and construction instrumentation to solar tracking, heavy machinery and vehicle‑level safety systems — with buyer persona profiles and procurement timelines.

Digital Inclinometer Market

Technology and product playbooks: Comparative assessments of MEMS, force‑balance and optical technologies, including integration considerations (interfaces, calibration requirements, environmental ruggedization), recommended specs for target applications, and go‑to‑market packaging options (sensor + firmware + analytics).

Channel & pricing intelligence: Recommended distribution architectures (OEM vs. system integrator vs. direct sales), commercial terms, and pricing benchmarks for new product launches and aftermarket services.

Supply‑chain & operations risk matrix: Supplier concentration, critical component vulnerabilities (notably MEMS die supply and calibration services), and mitigation playbooks covering dual‑sourcing, inventory policy, and contract structuring.

M&A and partnership opportunity map: Identification of strategic acquisition targets and partnership archetypes by capability gap (sensor IP, ruggedization expertise, systems integration, software/analytics).

Commercial execution toolkit: Templates and checklists — RFP language, technical evaluation scorecards, a 100‑day product launch sprint, and sample SLAs for field calibration & warranty programs.

The industry’s projected CAGR of 6.3% reflects an environment where steady replacement cycles intersect with expanding new‑build demand. Two dynamics are particularly material for 2026 planning:

Technology consolidation around MEMS: MEMS solutions increasingly dominate due to their compact size, low power, cost efficiency and integration ease. This reduces hardware cost pressure and shifts premium capture to firmware, calibration, and analytics — areas where OEMs and integrators can differentiate.

Application breadth expanding beyond classic uses: Structural health monitoring for aging infrastructure, precision solar tracking, industrial automation and vehicle/platform safety are all adding incremental addressable use cases. Buyers prize reliability, ruggedization and standardized interfaces to integrate sensors into broader monitoring ecosystems.

Regulatory and quality signals also matter in 2026: follow‑up ISO audits and quality certifications among manufacturers underscore buyer expectations for consistent production controls and traceable calibration regimes. That focus affects supplier selection and liability exposure in capital projects and safety‑critical systems.

The market sits in a moderate consolidation phase: the top three vendors together account for roughly 38.5% of market value, while the top five capture approximately 52.7%. This structure creates a two‑track strategic environment: established brands defend broader industrial and harsh‑environment applications, while specialist and OEM players pursue deep vertical niches.

Jewell Instruments (Manchester, NH, USA): Strong in MEMS and force‑balance platforms with multi‑interface outputs. Their roadmap and recent product introductions emphasize higher resolution and faster response — positioning them for industrial and harsh environment wins.

GEOKON (Lebanon, NH, USA): A go‑to for geotechnical and in‑place inclinometer systems, with domain expertise in slope stability and structural monitoring — a valuable anchor for infrastructure programs requiring long‑term monitoring and reporting protocols.

US Digital (Vancouver, WA, USA): Known for high‑resolution absolute and networked inclinometers; attractive to solar, dredging and industrial players that require full‑range, high‑precision sensing and networked telemetry.

Level Developments Ltd (Croydon, UK): A strong OEM supplier with product lines tailored to solar tracking and machinery; recent catalog updates show emphasis on temperature compensation and interface parity for industrial integration.

Rieker Inc & Fredericks Company (US): Focused on vehicle/boom monitoring and precision industrial sensors respectively — both hold positions in applications where ruggedness and long‑term drift performance are decisive selection criteria.

TE Connectivity (Schaffhausen, Switzerland): Brings scale and systems‑level integration, with CAN‑enabled tilt products for platform leveling and tip‑over protection — a complement to their broader electro‑mechanical portfolio.

Recent company developments are instructive: product introductions and renewed quality certifications signal incremental innovation rather than disruptive leaps. For example, manufacturers are enhancing resolution and response times, while also formalizing quality processes — moves that raise the bar for enterprise procurement teams but also create tradeable differentiation points for sellers.

For product leaders, service heads and investment committees, our analysis crystallizes into five priority actions for 2026:

Shift margin focus from sensor hardware to value‑added services: With MEMS compressing unit hardware margins, pursue recurring‑revenue services — calibration subscriptions, analytics, lifecycle monitoring and project reporting — to defend gross margin.

Design for systems integration: Standardize interfaces and data models (serial protocols, RS232/485, CAN, Modbus and modern telemetry stacks) and provide robust SDKs so system integrators can reduce integration cost and accelerate time‑to‑value.

Invest selectively in ruggedization & certification: For infrastructure and heavy equipment markets, invest in environmental testing, traceable calibration and quality certifications to shorten procurement qualification cycles.

Pursue bolt‑on M&A and partnerships: Target acquisitions that supply missing capabilities — analytics, edge firmware, geographic distribution or application domain expertise — rather than stand‑alone sensor manufacturers that only add marginal volume.

Operationalize scenario planning: Use the report’s sensitivity models to stress test planning assumptions around MEMS supply risk, price erosion, and accelerated adoption in target verticals — then align inventory, procurement contracts and R&D roadmaps to the prioritized scenarios.

Our Digital Inclinometer Market report is built to move decisions from insight to execution. Beyond the published forecasts and competitive profiles, PW Consulting offers tailored engagements that include:

Customized TAM/SAM/SOM recalibration for your product portfolio and go‑to‑market targets.

M&A diligence and target screening informed by market concentration and capability maps.

Commercial blueprints — channel design, pricing playbooks and a 90‑day tactical launch plan for new sensor or service offerings.

Workshops that convert scenario outputs into P&L and operational KPIs for executive planning cycles.

2026 will shape platform choices and commercial architectures for the remainder of the decade. For companies that want to move from high‑level intent to executable 12–24 month plans, we recommend:

Obtain the full Digital Inclinometer Market report to access the proprietary segmentation matrices, regional/application splits, and downloadable financial models that are intentionally excluded from this preview.

Run one of PW Consulting’s rapid alignment workshops to adapt the report’s scenarios to your balance sheet and product roadmap.

Prioritize quick wins that lock in recurring service contracts (calibration, monitoring), while preparing targeted partnership or acquisition plans for capability gaps.

PW Consulting’s preview demonstrates that the Digital Inclinometer Market is not merely growing — it is maturing into a systems‑centric industry where commercial success depends on integration, services and risk‑managed supply strategies. The full report provides the granular data and executable tools required to translate these strategic insights into measurable 2026 outcomes. To access the complete study and engage PW Consulting on a bespoke engagement, visit our research portal or contact our industry practice team.

For detailed analysis of this topic, please visit the official page:Digital Inclinometer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com