Brazil Elderly Care Market Overview: Key Drivers and Challenges

Other |

2026-05-26 07:49:10

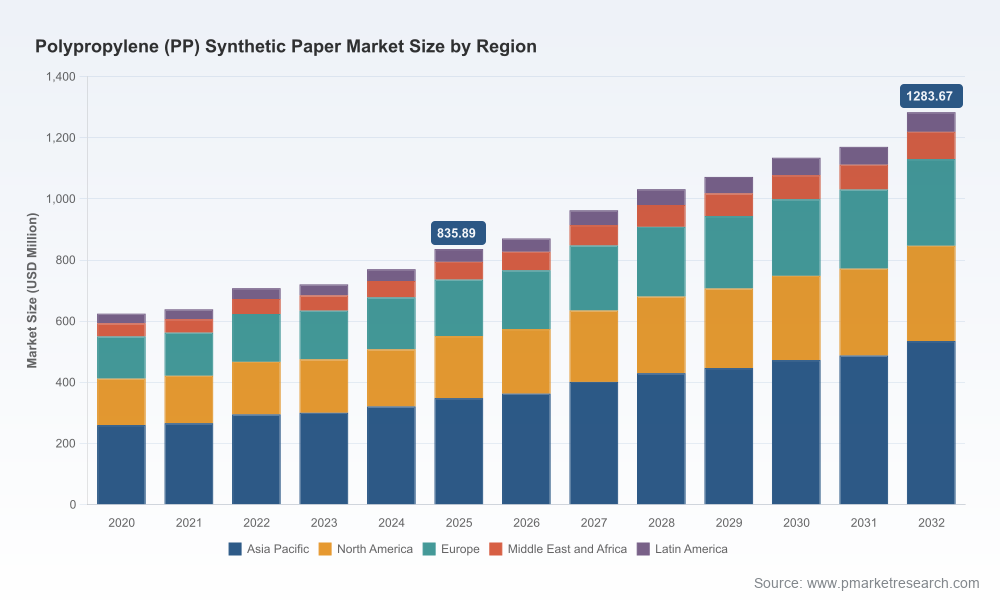

PW Consulting’s latest market research on Polypropylene (PP) Synthetic Paper provides a concentrated, decision-focused briefing for executives preparing strategy in 2026. Our independent analysis combines historical performance (2020–2025), forward-looking projections for 2026–2032, and practical playbooks for procurement, product development, and go-to-market moves. Key macro takeaways: the global PP synthetic paper market reached a base size of approximately USD 836 million in 2025 and, under our central case, is forecast to expand at a compound annual growth rate (CAGR) of about 6.32% through 2032 — reaching a projected market value north of USD 1.28 billion by the end of the forecast horizon.

Polypropylene Pp Synthetic Paper Market

Timing: 2026 is a pivotal inflection year. Raw material volatility and accelerating end-market demand (labels, packaging, specialty printing, and security applications) are reshaping supplier economics and product roadmaps.

Polypropylene Pp Synthetic Paper Market

Competitive posture: The market structure is moderately concentrated, with a handful of global leaders and a broader group of regional specialists. That concentration dynamic creates windows for consolidation, premium product positioning, and selective capacity expansion.

Polypropylene Pp Synthetic Paper Market

Actionability: This preview distils the report’s strategic outputs — scenario-tested recommendations, supplier risk heat maps, and go-to-market playbooks — enabling rapid embedding into 2026 budgeting and capex cycles.

After steady growth through the early 2020s, the sector entered 2025 with momentum from sustainable packaging mandates, demand for durable and moisture-resistant substrates, and innovation in digital print compatibility. Our forecast assumes continued adoption across commercial printing, labeling, and specialty fields. At a roughly 6.3% CAGR, total market expansion will be meaningful but not explosive; the growth profile favors companies that can optimize margins through formulation innovation, downstream integration, or differentiated channels such as digital print-ready grades.

For corporate strategists, three high-impact implications stand out:

Margin resilience will hinge on feedstock and conversion efficiency. Price shocks in propylene and naphtha directly compress margins for unwary producers; cost pass-through and hedging frameworks must be re-examined for 2026 budget cycles.

Product premiumization is a durable path to higher returns. Certifications (e.g., food contact, environmental management), printability assurances for digital presses, and specialty formulations (tear-resistant, stiff lay-flat, UV compatibility) command differential pricing and buyer loyalty.

Channel and application focus can outpace raw capacity expansion. Targeted commercialization into growing subsegments — driven by packaging sustainability and demand for weatherproof printed materials — offers faster ROI than indiscriminate capacity builds.

Market sizing and scenario forecasts (base year 2025, central-case CAGR to 2032) with sensitivity analyses tuned to feedstock price swings and demand-side adoption curves.

Commercial playbooks: price realization strategies, procurement contracting templates, and channel prioritization matrices for label converters, flexible packaging suppliers, and print houses.

Supplier risk assessments and negotiation tactics, including counterparty scorecards that blend capacity, technological differentiation, certification footprint, and geographic exposure.

Product roadmaps and R&D priorities: formulation levers to improve printability for digital presses, water and chemical resistance, and recyclability claims compatible with evolving regulations.

M&A and partnership diagnostics: opportunity heat maps for bolt-on acquisitions, joint ventures, and toll-manufacturing agreements across priority regions.

Appendix of primary-source interviews, technical test protocols, and a compact benchmarking model you can plug into internal financial plans.

The sector blends global brand leaders with strong regional operators. The players highlighted in our report represent the strategic choices available to buyers and investors: global incumbents focused on innovation and scale, regionally entrenched producers with technical breadth, and specialized film manufacturers extending into synthetic-paper grades.

Yupo Corporation — The largest global manufacturer, YUPO’s multi-grade portfolio and market presence (including North America operations) make it the go-to partner for high-consistency, specialty-print grades. Its trade show activity into 2025–2026 signals continued customer engagement and product innovation pipelines.

Nan Ya Plastics (Formosa group) — Strong PEPA capabilities and a wide product variety position Nan Ya as a capacity and compliance leader; ongoing environmental certifications and FDA-compliant options increase appeal for food-contact and regulated applications.

Nekoosa — Focused on printable, foldable, and weather-resistant grades for North American converters, Nekoosa’s certified digital-print offerings illustrate the premium niche strategy that yields higher ASPs.

Profol / American Profol — Profol’s custom cast films and branded synthetic-paper products give it differentiated product attributes in tear and chemical resistance — an attractive profile for industrial tagging and durable graphics.

Arjobex (Polyart), PPG, Cosmo Films, Taghleef, Jindal — These players combine regional scale, film-manufacturing capabilities, and sustainability credentials. Collectively they present acquisition or partnership targets for companies seeking faster market entry or proprietary grades.

Our competitive analysis goes beyond logos and product claims — we model supplier economics, capacity elasticity, and innovation cadence to predict who will be able to sustain price premiums and who will be forced into volume competition as feedstock pressure intensifies.

Feedstock volatility: Early-2026 data show material cost pressure with regional propylene and naphtha price upticks driven by supply disruptions and geopolitics. Companies that lack robust hedging or flexible feedstock strategies will see margin erosion sooner than demand softening would suggest.

Certification and restrictions: Environmental management systems and restrictions on hazardous additives (lead, hexavalent chromium, mercury, cadmium, certain phthalates) are increasingly table stakes for major converters and brand owners. Suppliers with active ISO 14001 processes and documented compliance are advantaged in food-contact and regulated markets.

End-customer sustainability demands: Demand for recyclable, tree-free substrates is creating both a pricing premium for verified claims and a product development imperative for new PP formulations that balance recyclability with print performance.

For producers: Prioritize margin protection by investing in conversion efficiency and selective product premiumization (digital-print certified grades, high-brightness coatings, and medical/security substrates). Consider flexible contracts that pass-through feedstock costs while preserving volume commitments.

For buyers (brands & converters): Re-assess supplier panels with an emphasis on proof-of-compliance, dual-sourcing in geographies exposed to feedstock shocks, and locking-in digital-print grades that reduce waste and time-to-market.

For investors and M&A teams: Target assets that bring formulation IP, certification footprints, or regional distribution that fills current portfolio gaps. The market structure favors bolt-on acquisitions that deliver immediate channel access and technical breadth.

This “trailer” highlights strategic direction and practical implications, but intentionally omits the detailed segment-level breakdowns, regional-weighted forecasts, and exact share-by-application figures that are essential for tactical execution. The full PW Consulting report contains those detailed tables, supplier scorecards, and downloadable financial models that allow teams to map scenarios directly into 2026 operating plans.

Integrate the forecast envelope and sensitivity scenarios into your Q1 procurement and pricing reviews.

Use supplier risk heat maps to triage contracts for renegotiation or contingency sourcing ahead of peak seasonal ordering windows.

Prioritize R&D spend on printability and recyclability features that unlock higher-margin channels and reduce obsolescence risk.

For boards and investment committees: use the M&A diagnostics to test three acquisition cases (scale, capability, and channel) and quantify payback under varied feedstock scenarios.

PW Consulting’s full Polypropylene Synthetic Paper Market report is designed to convert market insight into executable plans for 2026. For access to the complete dataset, full segmentation tables, and the downloadable strategic playbooks referenced above, please visit the report landing page (link available from PW Consulting) or contact your account representative.

For detailed analysis of this topic, please visit the official page:Polypropylene Pp Synthetic Paper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com