https://www.facebook.com/TrimShiftBloodSupport

Art |

2026-05-15 07:08:29

The Bone Marrow Aspirate Concentrate (BMAC) treatment market is entering a phase of accelerated, structural growth driven by technology refinement, point-of-care adoption, and clearer regulatory boundaries for autologous therapies. Our new market study — covering historical performance through 2025 and projecting to 2032 — quantifies a reliable expansion path and translates that trajectory into practical choices for executive teams planning 2026 investments. On a macro scale, PW Consulting projects the market value to exceed USD 500 million in 2025 and to approach the high hundreds of millions by the end of the forecast period, growing at a compound annual growth rate of 7.65% from the 2026 baseline.

Bone Marrow Aspirate Concentrate Treatment Market

Inflection point timing. 2026 marks the first full planning year after the report’s base year (2025). Companies that align product roadmaps, clinical evidence programs, and commercial channels at the start of 2026 will capture disproportionate share of demand as adoption accelerates over the following 3–5 years.

Bone Marrow Aspirate Concentrate Treatment Market

Evidence-driven commercialisation. Payers remain selective; many BMAC uses are still paid out-of-pocket. Strategic investment in targeted clinical endpoints and real-world evidence in 2026 will materially improve negotiating leverage with high-volume healthcare systems and high-value provider groups.

Bone Marrow Aspirate Concentrate Treatment Market

Technology convergence. Advances range from sensor-driven automation and double-spin concentration to centrifuge-free filtration and aspiration needle design. The next 18–36 months will determine which architectural approaches become dominant in point-of-care workflows.

Regulatory clarity versus regulatory risk. Many BMAC devices qualify under the FDA’s minimally manipulated autologous HCT/P framework (361 pathway) when used homologously; cultured/expanded cell products do not. This creates a two-track competitive landscape where device and consumable players can scale faster if they maintain 361 compliance, while cell-expansion players face higher regulatory overhead.

Market sizing and 2026-2032 forecasts with scenario overlays — base, conservative, and upside — designed to feed commercial and corporate planning spreadsheets.

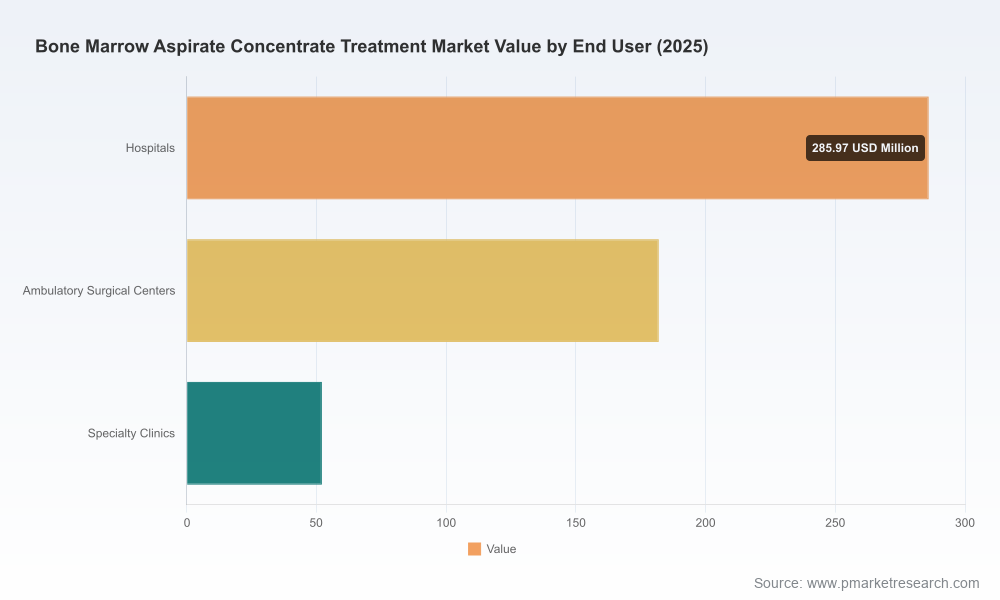

Go-to-market playbooks for hospitals, ambulatory surgical centers (ASCs), and specialty clinics, with channel economics, margin profiles, and consumable-replacement strategies.

Regulatory and reimbursement decision trees: how to position a device under 361 vs. when IND/biologic pathways become unavoidable; coding and billing implications, including practical guidance around CPT usage and the common reliance on unlisted codes for off-label billing contexts.

Clinical evidence blueprints keyed to payer and clinician decision criteria — trial design templates, prioritized endpoints, sample-size heuristics, and real-world evidence deployment plans.

Competitive due diligence and M&A screening: strategic scorecards, valuation sensitivities, and a prioritized list of technology, consumable, and access plays.

Commercial sensitivity and pricing models that reflect current out-of-pocket realities and institutional procurement dynamics, plus bundling strategies to accelerate adoption.

Risk matrix and mitigation playbook covering regulatory shocks, payer policy shifts, supply-chain concentration, and clinical evidence surprises.

The BMAC ecosystem today is populated by established medtech platform providers, niche device specialists, and emerging innovators that target specific nodes in the value chain (aspiration, concentration, processing, and disposables). Market concentration is meaningful but not prohibitive: the top three firms account for a substantive share of revenue, while the top five take a majority share — a structure that supports both incumbent scale advantages and tactical entry by well-funded challengers.

Terumo BCT (Harvest) — known for point-of-care platforms and procedure packs that streamline BMA concentration. Strategic implication: strong distribution and clinical relationships make Terumo BCT a logical partner or consolidation target for players needing global channels.

Arthrex, Inc. — emphasis on automation and customizable formulations through sensor-enabled systems. Strategic implication: offers a blueprint for differentiation via workflow integration and clinician control over formulations.

Zimmer Biomet — markets integrated systems for processing blood and bone marrow, supporting grafting workflows. Strategic implication: incumbency in musculoskeletal surgery provides cross-sell opportunities with implants and biologics.

EmCyte Corporation — double-spin systems that emphasize high-concentration yields. Strategic implication: scientific performance claims can command premium pricing but require reproducible clinical evidence.

Globus Medical, Inc. — products that include platform and aspiration kits; strategy leverages existing orthopaedic footprint. Strategic implication: manufacturing and supply integration are competitive levers.

Ranfac Corporation — specializes in aspiration needles and harvest quality. Strategic implication: harvest-device optimization is an underappreciated value driver for clinical outcomes and differentiation.

SurGenTec — provides centrifuge-free aspiration kits with integrated filtration; received FDA 510(k) clearance in August 2024. Strategic implication: regulatory clearances for novel, workflow-simplifying devices can rapidly disrupt buying patterns in ambulatory settings.

Regulatory pathway: design products and labeling to retain the 361 pathway where possible. If a product strategy requires expansion or culture, plan for IND timelines and budget for the higher regulatory burden.

Reimbursement realities: many musculoskeletal BMAC indications remain outside routine Medicare or major insurer coverage; patients often pay out-of-pocket. CPT coding conventions (e.g., established codes for certain spine aspirations and frequent use of unlisted codes elsewhere) create both revenue and compliance complexity.

Clinical evidence focus: payer-relevant endpoints (functional outcomes, reduction in revision or reoperation, cost-per-quality-adjusted-life-year) are more persuasive than surrogate laboratory markers when negotiating institutional adoption.

Accelerate targeted evidence generation: fund a pragmatic, multi-site registry beginning Q1–Q2 2026 that collects both clinical effectiveness and resource utilization data tailored to high-volume procedures.

Optimize product architecture for point-of-care economics: develop consumable-driven revenue models and clinician-friendly disposables that lock-in recurring revenue while minimizing capital hurdles for ASCs.

Leverage regulatory pathways: where homologous use supports it, standardize labeling and instructions of use to sustain 361 qualification and shorten market access timelines.

Expand channel partnerships: pursue OEM or co-marketing agreements with established orthopaedic supply chains to accelerate scale without full direct-sales expansion.

Evaluate bolt-on M&A: prioritize targets that fill capability gaps (aspiration quality, filtration that avoids centrifugation, or proven consumable franchises) rather than horizontal revenue alone.

Prepare pricing/playbook for cash-pay patients: design transparent, value-communicating packages that reduce sticker shock and improve conversion in elective settings.

Monitor market consolidation and competitive signals: the concentration profile favors both defensive partnerships among incumbents and opportunistic entry by agile innovators; set clear trigger points for accelerated responses.

This press brief highlights the strategic imperatives and competitive context. The full PW Consulting report contains the granular models, detailed scenario outputs, proprietary scoring of suppliers, and downloadable templates designed to be imported directly into corporate planning tools. Detailed segmentation by geography, indication, and end-user — plus company-level shipment models and adoption curves — are intentionally reserved for the full report to preserve the practical competitive value that subscribers expect.

Schedule a brief strategy workshop in Q1 2026 using the report’s scenario decks to align R&D, clinical, regulatory, and commercial teams around a single go-to-market path.

Request the report’s M&A heat map if pursuing inorganic growth; it will accelerate target screening and valuation calibration.

Engage with PW Consulting’s advisory team for a tailored 90-day implementation plan that maps the report’s insights into board-ready investment cases.

PW Consulting combines industry-grade market modeling, clinical and regulatory expertise, and hands-on commercial due diligence to help medtech and life-science executives make high-confidence strategic decisions. For access to the full Bone Marrow Aspirate Concentrate Treatment Market report, data workbooks, and advisory engagements, please visit our official report page or contact our commercial team to arrange a briefing.

For detailed analysis of this topic, please visit the official page:Bone Marrow Aspirate Concentrate Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com