Automotive Battery Box Market — Strategic Imperatives for 2026 Decision‑Makers

PW Consulting’s latest Automotive Battery Box Market Research (base year 2025; forecast period 2026–2032) delivers the actionable intelligence executives need to make capital, sourcing, and product-architecture decisions in 2026. Our analysis shows the market expanding rapidly — from early‑decade levels in the low‑billions to an anticipated market exceeding USD 21 billion by 2032, representing a compound annual growth rate of 18.52% across the forecast window. This trajectory creates both near‑term execution challenges and multi‑year opportunity windows for OEMs, Tier‑1s, material suppliers, and private investors.

Automotive Battery Box Market Research

Why this report matters for 2026 planning

- Time‑sensitive capacity decisions: Suppliers and OEMs must reconcile aggressive demand growth with long lead times for tooling, certified production lines, and qualified materials.

- Material and architecture tradeoffs: Weight, safety, manufacturability, and recyclability drive mutually conflicting priorities; the right portfolio strategy materially affects vehicle range, cost, and crash performance.

- Regulatory and safety compliance: Evolving test standards and battery regulations require early investment in validation and digital traceability to avoid market access delays.

- Partnership and M&A timing: The market’s moderate concentration and ongoing technology shift mean first‑mover integration advantages can lock in scale and margin.

What the report contains — practical modules for fast decisioning

- Concise market sizing and scenario forecasts by year (2020–2032) with sensitivity cases tied to EV penetration, average pack voltage, and vehicle segmentation assumptions.

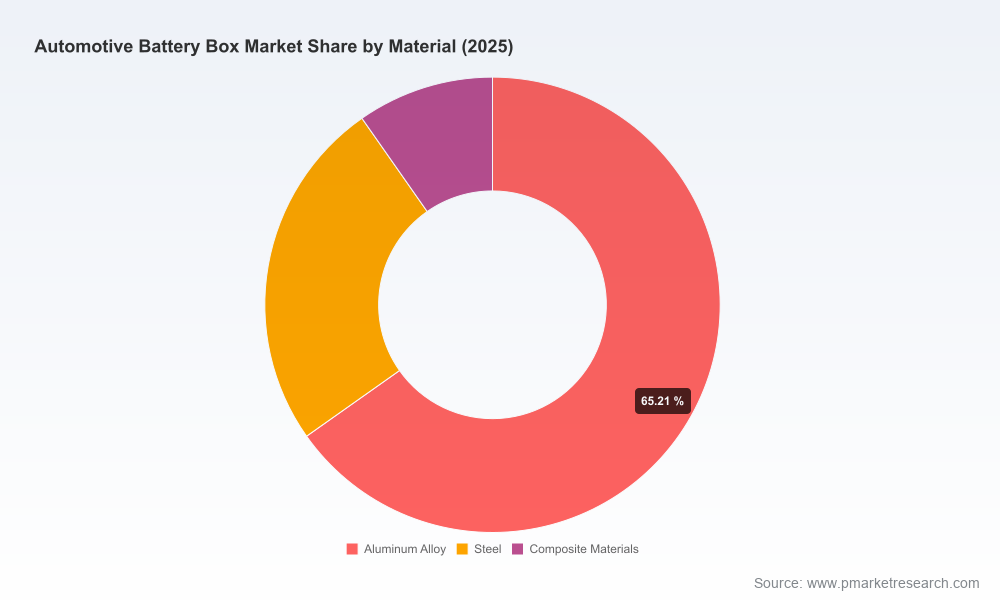

- Material‑technology playbook: comparative TCO frameworks for aluminum, steel, composite, and thermoplastic enclosures incorporating weight, manufacturability, cost trajectory, and end‑of‑life recovery.

- Regulatory & safety matrix: mapped obligations under major jurisdictions, plus independent material screening and thermal‑runaway test guidance for procurement and validation teams.

- Competitive benchmarking: capability maps, manufacturing footprint considerations, and supplier scorecards to inform RFP shortlists and JV negotiations.

- Manufacturing & automation playbook: capex and throughput models, preferred forming/joining routes, and ramp templates for modular and scalable production lines.

- Commercial and go‑to‑market strategies: OEM procurement hedges, service‑layer opportunities (thermal management, integration), and aftermarket/remanufacturing cases.

- Risk & mitigation dashboard: raw material volatility, regulatory shocks, safety incidents, and supply concentration scenarios with contingency playbooks.

- Primary research annex: interview summaries, supplier visit notes, and methodological transparency to support board‑level decisioning.

Competitive landscape — who matters and how they are positioned

The supplier ecosystem is evolving beyond simple metal forming. Strategic implications for 2026 center on capability breadth (materials, integration), validated production experience, and proximity to volume OEM platforms.

Automotive Battery Box Market Research

- Magna International Inc. (Aurora, Canada) — systems integrator with steel, aluminum, and proprietary one‑piece forming designs. Strength: end‑to‑end engineering and global assembly capabilities that accelerate OEM qualification cycles.

- Novelis Inc. (Atlanta, USA) — advanced aluminum alloys and roll‑formed frame solutions. Strategic edge: material tech delivering substantial weight reduction versus steel; attractive for OEMs prioritizing light‑weight architectures and efficiency gains.

- SGL Carbon (Wiesbaden, Germany) — carbon/glass‑fiber composites in serial automotive quality. Opportunity: composites now compete on cost and cycle time for high‑value programs, enabling differentiated thermal and crash behavior.

- Teijin Mobility (Japan) — multi‑material enclosures with automotive‑grade properties. Advantage: integrative know‑how across polymeric and fiber‑reinforced systems for mixed‑material architectures.

- Constellium (Paris, France) — structural aluminum and full enclosure solutions including cast and extruded elements valuable for crash‑resistant and thermally managed designs.

- Kautex (Textron) (Bonn, Germany) — fully composite Pentatonic™ enclosures for cell‑to‑pack and module configurations. Position: targeted solutions for OEMs seeking radical weight reduction and design freedom.

- Trinseo (Berwyn, USA) — thermoplastic, flame‑retardant grades (halogen‑ and PFAS‑free) suited to high‑volume LFT‑D processing. Relevance: polymer routes that meet tightening environmental and safety requirements.

- voestalpine Metal Forming (Linz, Austria) — specialist forming technologies (hot/cold/roll), valuable where metal process maturity and dimensional control matter most.

- BENTELER (Salzburg, Austria) — modular, size‑scalable battery trays with proven series production history; attractive for OEMs seeking off‑the‑shelf scalability.

- Linamar International Inc. (Guelph, Canada) — North American manufacture and system supply presence; relevant to regional content strategies and near‑market sourcing.

These profiles reveal a market where material innovation and integration capability create differentiated competitive moats. Our competitive chapter overlays technical KPIs (mass efficiency, crash performance, manufacturability), certification readiness, and demonstrated ramp history to produce prioritized supplier lists for program managers.

Automotive Battery Box Market Research

Recent developments and what they signal for 2026 buyers

- OPmobility’s February 2026 contract to supply more than one million 350V battery packs (including enclosures) for a North American OEM signals rapid scale commitments by OEMs to hybrid architectures and underscores the need for suppliers to demonstrate high‑volume readiness at short notice.

- A 2025 facility investment by a major components manufacturer (Transair piping / Parker case) highlights the ongoing wave of capacity investments at the plant and sub‑system level — a cue for OEMs to secure long‑lead manufacturing slots and for investors to evaluate brownfield vs greenfield tradeoffs.

Key dynamics shaping procurement and product choices in 2026

- Material substitution is no longer academic: second‑generation aluminum alloys and serial composites are shifting the cost‑performance frontier, enabling weight reductions and new integration geometries.

- Regulatory tightening and standardization: the EU Battery Regulation and emergent test methodologies (including UL‑based Battery Enclosure Material Screening) raise the bar for validated materials and digital traceability requirements such as the battery passport.

- Moderate supplier concentration: the market exhibits a degree of market share consolidation among leading suppliers (CR3 ~42.15%; CR5 ~58.4%), meaning procurement teams need a two‑track strategy — secure scale with established partners while cultivating specialized niche vendors.

- Manufacturing economics: automation, joining technologies, and modular design reduce per‑unit cost but require upfront capital and validated supply chains; tradeoffs between localization and unit economics are program‑specific.

- Safety and certification are commercial bottlenecks: validated performance in thermal‑runaway events and flame‑retardancy testing is increasingly prerequisite for program awards.

Actionable strategic playbook — priorities for 2026

- Adopt a dual‑track materials strategy: fast‑follow aluminum for immediate programs while piloting composites/thermoplastics on targeted vehicle platforms to hedge technology risk.

- Lock in validated suppliers early: prioritize partners with demonstrated series production, test‑report transparency, and regional capacity to meet ramp timelines.

- Invest in testing & certification infrastructure: establish or partner for UL‑aligned material screening and thermal‑runaway test capability to shorten OEM validation cycles.

- Design for modularity & scalability: favor architectures that allow platform commonality and late‑stage differentiation to protect volume flexibility.

- Embed circularity and compliance: account for end‑of‑life recovery, recyclability targets, and digital battery passport requirements in supplier contracts to avoid future retrofit costs.

- Model supply concentration risk: use scenario planning to understand the business impact of supplier service interruptions given observed market concentration metrics.

- Pursue targeted M&A and JV plays: acquire or partner for missing capabilities (e.g., validated composite serial production, advanced aluminum alloys, or thermoplastic flame‑retardant grades).

How PW Consulting’s report accelerates your 2026 roadmap

Our research stitches together primary supplier interviews, factory visits, independent materials testing references, and a revenue‑backed forecast model to produce a playbook that is both strategic and executable. For procurement leaders, program managers, and corporate strategy teams, the report translates market growth and technology signals into prioritized actions, procurement templates, and financial sensitivities tied to critical choices (material selection, localization, and supplier structure).

Note: this summary purposefully omits the full segment tables, regional and application splits, and detailed company revenue breakdowns to preserve the decision‑grade value of the complete study. The full report includes granular segmentation, supplier revenue estimates, program‑level cost models, and downloadable scenario models to support board presentations and execution planning.

To access the full dataset, supplier scorecards, and the downloadable financial models that underpin our 2026 scenarios, please visit PW Consulting’s Automotive Battery Box Market Research page or contact our industry team for an executive briefing.

For detailed analysis of this topic, please visit the official page:Automotive Battery Box Market Research

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com