Strategic Preview — Water Treatment Equipment in Power Market: PW Consulting’s 2026 Decision-Grade Outlook

As power producers, equipment OEMs, and industrial investors finalize capital and operational plans for 2026, the water treatment equipment market serving the power sector has moved from a technical footnote to a strategic fulcrum. Our new market study — based on a 2025 industry baseline, a six‑year historical assessment (2020–2025) and a forward forecast to 2032 — synthesizes market scale, supplier dynamics, regulatory vectors and actionable playbooks that commercial and engineering leaders need to make high‑confidence decisions this year.

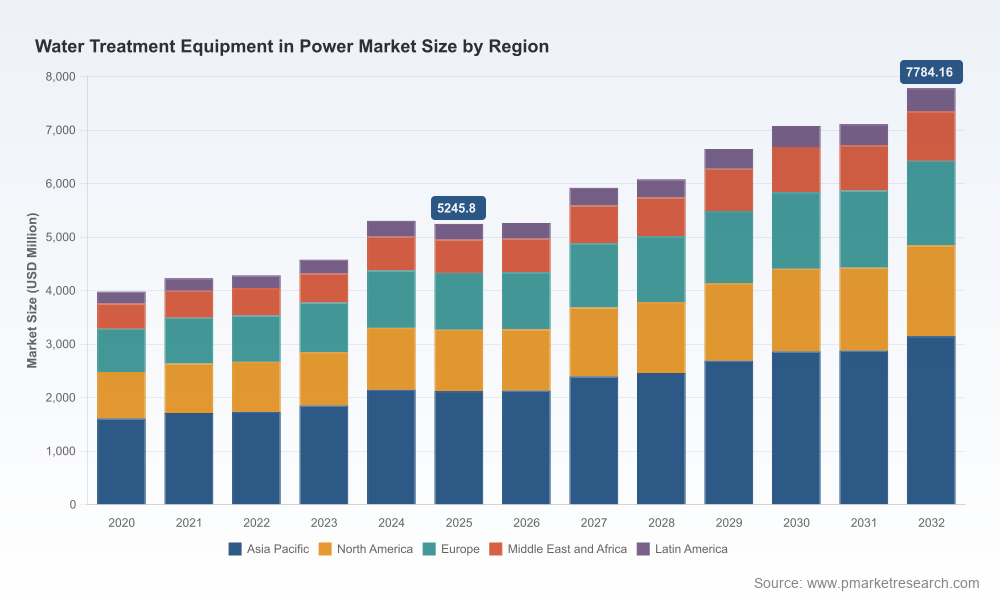

Water Treatment Equipment In Power Market

Market snapshot: size, trajectory and what it means for planning

At the end of the report’s base year (2025) the market for water treatment equipment in power was on the order of multiple billions of US dollars. Our forecast shows a steady expansion through 2032, with a compound annual growth rate of 5.8% across the 2026–2032 horizon and a projected market value approaching the high single‑digit billion mark by the end of the period. This trajectory is not uniform: growth is being driven by a mix of regulatory pressure, plant reliability programs, and increasing adoption of higher‑recovery and closed‑loop water architectures.

Water Treatment Equipment In Power Market

For 2026 decision‑makers this macro picture has three practical implications:

Water Treatment Equipment In Power Market

- Budget windows must reflect medium‑term growth expectations. Capital approval processes that assume flat demand for treatment equipment risk supply lead‑time and cost shocks as OEMs ramp projects to capture the expanding market.

- Technology selection should be evaluated against a seven‑year TCO horizon. The equipment choices you make this year will interact with evolving regulatory standards and reuse requirements through 2032.

- Supply chain and materials risk is no longer peripheral. Core inputs such as ion exchange resins and activated carbon are subject to capacity constraints and regulatory-driven demand spikes.

Key market dynamics shaping 2026 decisions

The market’s near‑term dynamics combine structural, regulatory and technological forces:

- Regulatory acceleration: Stricter contaminant controls (notably around emerging contaminants) and tightened discharge limits are increasing the need for granular activated carbon (GAC) processing and advanced polishing stages. These rules create near‑term demand for both permanent systems and interim/mobile solutions.

- Water scarcity and reuse: Water stress in many power basins is prompting operators to prioritize reuse, high recovery treatment trains and zero liquid discharge (ZLD) pilot programs. Projects now commonly weigh freshwater procurement costs against capital and operating costs for reuse systems.

- Operational reliability and purity needs: Boiler and cooling circuits require increasingly precise chemistry control to avoid scaling and corrosion. This is driving uptake of integrated solutions that bundle chemical programs, membranes, ion exchange, and digital monitoring into end‑to‑end offerings.

- Supply chain concentration and capacity shifts: The competitive landscape shows moderate concentration among leading suppliers, with the top three and five firms together representing a significant share of installed capacity. Simultaneously, suppliers and raw‑material manufacturers are announcing capacity projects and product launches to capture new demand.

- Digital and services convergence: Equipment sales are increasingly accompanied by digital monitoring, predictive maintenance and performance guarantees. Buyers are putting a premium on partners who can demonstrate measurable uptime and chemical/energy savings.

What the PW Consulting report gives you — practical, decision‑ready content

This study is designed for practitioners who need to move from insight to action in 2026. Highlights include:

- Validated market sizing and a granular, scenario‑based forecast framework (2026–2032) that supports both base and stress scenarios for capex planning.

- A technology primer and comparative performance benchmarking (membrane systems, ion exchange, filtration, evaporation/crystallization, disinfection/chemical treatment), including failure modes, recovery tradeoffs and typical footprint and energy implications.

- Procurement and contract templates: vendor shortlisting criteria, KPIs and contract structures (fixed price, milestone payments, performance‑based contracts, rental and mobile plant options) tailored to thermal, combined‑cycle and nuclear assets.

- Site‑level decision tools: water balance templates, simple payback calculators and a seven‑year TCO model to quantify CapEx vs OpEx tradeoffs for reuse, ZLD and high‑recovery membrane trains.

- Supply chain risk register: raw‑material concentration analysis, lead‑time scenarios and mitigation levers (dual sourcing, buffer stocks, service contracts, local reactivation services for GAC).

- Vendor assessment and partnership playbooks: scorecards and negotiation playbooks for strategic alliances, OEM supply agreements and MRO frameworks.

To uphold the “trailer” principle, the report demonstrates how to use these tools in real contracting and asset‑management decisions, while directing readers to the full report and our interactive dashboard for the underlying segment‑level datapack and vendor scorecards.

Competitive landscape — positioning and strategic moves

The competitive field comprises global system integrators, specialist membrane and chemical players, and equipment builders offering modular and mobile solutions. Our analysis highlights several archetypal strategies and what they imply for buyers and investors:

- Full‑system integrators (examples include large global engineering and water technology houses): these companies are competing on end‑to‑end capability — membranes, ion exchange, chemical programs and service contracts — and tend to win large EPC and long‑term service agreements. Their scale supports financing and risk transfer for large reuse and ZLD projects.

- Digital and monitoring leaders (companies with strong sensing, analytics and service platforms): their differentiation is operational optimization and availability guarantees. Buyers who prize performance‑based contracting should prioritize partners with validated digital stacks and demonstrated energy/water savings in power environments.

- Specialist materials and high‑purity suppliers: these players (including resin and activated carbon specialists) are critical to boiler feed and condensate polishing markets. Recent product introductions targeting nuclear‑grade applications and announcements of capacity expansions underscore a market in which materials availability and specification compliance matter as much as core equipment.

- Modular and mobile solution providers: rental, mobile and skidded systems are increasingly used as tactical responses to plant outages, retrofit windows and regulatory compliance deadlines. They offer an attractive option to bridge gaps while permanent solutions are delivered.

Recent market events illustrate these strategic vectors: several suppliers have launched nuclear‑grade resins and mobile treatment offerings targeted at high‑purity applications, while reactivation and reprocessing capacity announcements by carbon manufacturers are beginning to reshape raw‑material availability. For 2026 planners, these moves translate into tangible levers — vendor consolidation risk, options for interim compliance, and a clearer path to secure critical inputs.

Actionable recommendations for 2026 decision‑makers

Based on the market dynamics and supplier landscape, we recommend the following priorities for teams making capital, sourcing and operational choices this year:

- Adopt a two‑track procurement approach: secure immediate compliance via modular/mobile solutions and negotiate long‑lead permanent systems with performance guarantees to manage both near‑term risk and long‑term economics.

- Stress‑test supplier continuity: include raw‑material availability clauses, local reactivation options and dual‑sourcing among your procurement requirements, particularly for ion exchange resins and GAC.

- Embed digital deliverables in contracts: require data‑driven KPIs, remote monitoring and predictive maintenance provisions tied to financial outcomes (e.g., reduced chemistry usage, reduced unplanned outages).

- Quantify water‑risk economics at the site level: use the report’s site water balance and 7‑year TCO model to decide between increased freshwater sourcing and investments in reuse/ZLD — factor in expected regulation and freshwater cost escalation.

- Pursue partnerships, not just suppliers: look for technology partners who offer co‑funding, pilot programs and staged rollouts to reduce proof‑of‑concept risk and accelerate deployment.

- Prioritize retrofit‑friendly designs: modular, skidded and containerized systems reduce outage time and enable phased integration into complex plant operations.

How to use the full PW Consulting deliverables

The public executive summary accompanying this preview outlines the strategic implications. The full study contains the decision‑support assets that operational teams need to act in 2026: downloadable TCO and site‑water templates, vendor scorecards with detailed assessment criteria, and an interactive scenario dashboard that lets you test sensitivity to regulation, freshwater cost inflation and technology adoption curves.

For buyers, the immediate use cases are supplier selection, capital planning and compliance gap closure. For investors and OEMs, the report supports market entry assessments, M&A target screening and product development prioritization. For service providers, it identifies where to bundle digital services and performance guarantees to capture higher margin, recurring revenue streams.

Final note — a guarded invitation

PW Consulting’s Water Treatment Equipment in Power Market study is intentionally calibrated to be both practical and provocative: it surfaces the levers that will move procurement and engineering agendas in 2026 while reserving detailed segment datapacks and vendor scoring for the full subscriber report and our interactive portal. If you are preparing a capital plan, negotiating supplier terms, or building a technology roadmap for next year, this report is designed to be the operating manual for those decisions.

Visit the PW Consulting website or contact your account lead to access the complete dataset, vendor scorecards and scenario tools that underpin this strategic preview.

For detailed analysis of this topic, please visit the official page:Water Treatment Equipment In Power Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com