CuCr Contact Material Market to Reach USD 2.65 Billion by 2034

Other |

2026-07-01 07:56:41

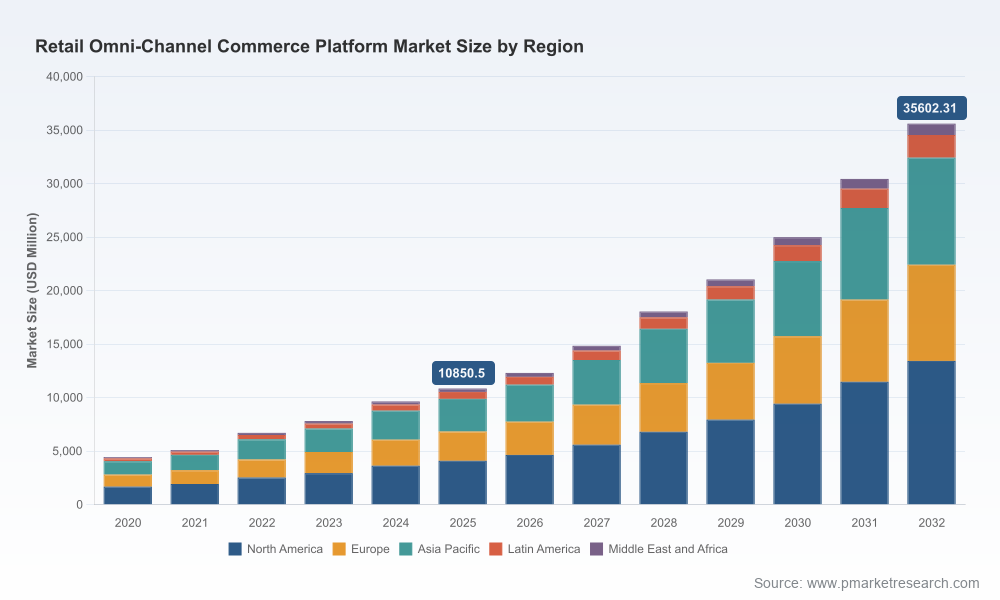

PW Consulting’s latest market research on Retail Omni‑Channel Commerce Platforms provides strategic clarity for executive teams planning investments and vendor selection in 2026. After analysing historical trends (2020–2025) and projecting through 2032, the study demonstrates sustained, double‑digit expansion driven by cloud migration, composable architectures, and AI‑native merchandising and fulfillment. The global market crosses the USD 12 billion threshold in 2026 and is forecast at a compounded annual growth rate (CAGR) of 18.5% through the 2026–2032 horizon. This briefing outlines the report’s value to boardrooms, CIOs, and transformation leaders while intentionally withholding detailed sub‑segment figures to encourage practitioners to consult the full report for granular project planning and procurement outputs.

Retail Omni Channel Commerce Platform Market

Timing: 2026 is a pivot year for retailers. A wave of platform renewals, rising infrastructure costs, and a new layer of state and cross‑border privacy rules create both urgency and opportunity. The decisions you make now define your omnichannel TCO, speed to value, and regulatory exposure for the next technology cycle.

Retail Omni Channel Commerce Platform Market

Risk‑calibrated investment: The market’s robust growth masks significant variation in implementation complexity. Our research maps out practical approaches — from cloud lift‑and‑shift to composable, API‑first transformations — enabling technology leaders to size investments against expected operational benefits, not vendor marketing claims.

Retail Omni Channel Commerce Platform Market

Vendor selection with intent: With platforms maturing along differing vectors (headless, CRM‑integrated, POS‑centric, or inventory‑first), vendor choice must be a strategic lever. The report supplies a repeatable vendor evaluation framework tuned to strategic fit, integration footprint, and roadmap alignment.

Our topline modelling shows the omni‑channel commerce platform market accelerating into the mid‑2020s and remaining a high‑growth segment through 2032, underscoring continued enterprise prioritisation of unified commerce capabilities. The drivers are multifold: retailers seek to eliminate order and inventory fragmentation; brand owners are expanding direct‑to‑consumer channels; and digital commerce paradigms (headless, composable, MACH principles) are reshaping integration and development economics.

For 2026 planning, the implication is clear — organisations should budget for platform modernization as a multi‑year program rather than a one‑off project. Capital allocation must incorporate not only license and implementation fees but also ongoing cloud, data, and integration run costs that have become material to total cost of ownership (TCO).

Prioritise composability where it reduces business risk. Adopt modular patterns for customer experience, catalog, and fulfillment so that parts of the stack can evolve independently without full rip‑and‑replace.

Bias toward API‑first vendors with mature integration patterns for POS, OMS, and third‑party marketplaces. A narrow focus on feature parity alone will increase future integration debt.

Embed data governance and privacy‑by‑design into the procurement and architecture phases. Emerging state laws and increasing data‑sovereignty controls require explicit mapping of customer data flows and cross‑border dependencies.

Model infrastructure inflation into TCO. Rising data centre and colocation costs, plus cloud premiuming for high‑performance workloads, mean that run costs can outpace initial implementation spend if not actively managed.

Establish a two‑speed roadmap: secure immediate commercial outcomes via proven packaged capabilities while incubating innovation (AI personalization, visual search, predictive fulfilment) in isolated, composable services.

The vendor landscape remains diverse: global software giants, specialised commerce platforms, POS incumbents, and emerging composable vendors each occupy distinct strategic positions. Our analysis profiles leading and challenger firms across product maturity, enterprise readiness, partner ecosystems, and innovation cadence. Key takeaways:

Enterprise suites (CRM/ERP incumbents) — firms that bundle commerce with CRM, ERP, or supply‑chain suites offer deep end‑to‑end capabilities and are attractive to large, process‑driven retailers that prioritise operational consolidation. Their strength is integration breadth; the trade‑off is often agility and modularity.

Headless/composable vendors — these players excel where speed of innovation, front‑end experimentation, and multi‑channel experiences are table stakes. They are the natural choice for digitally native brands and retailers that purposefully decouple experiences from core commerce engines.

POS and store systems specialists — companies with a long heritage in physical retail provide robust store operations, payments, and in‑store fulfilment capabilities. Their advantage is mature retail workflows and hardware integrations.

Mid‑market platforms — simpler to deploy and cost effective for scaled SMBs and smaller banners, these vendors accelerate omnichannel adoption but may lack the enterprise features required for complex global operations.

Notable vendor signals in early 2026 — such as new platform integrations, partnerships extending marketplace reach, and updates enabling tighter headless commerce integrations — confirm two trends: consolidation of ecosystem value around headless and multi‑region commerce, and vendor differentiation through partner networks rather than feature parity alone. Organisations should evaluate vendors based on ecosystem fit as much as core functionality.

Privacy and data residency have moved from compliance checkbox to strategic enabler or constraint. New state‑level privacy laws and intensified scrutiny on cross‑border transfers are forcing architecture choices that affect latency, analytics capability, and global master data strategies. The report includes a compliance matrix and recommended architectures to balance global customer experiences with local legal obligations.

On infrastructure, higher data centre construction and operational costs are pressuring both cloud and colocation budgets. Retailers must evaluate options such as committed consumption models, workload right‑sizing, and edge caching to control marginal cost growth while preserving performance.

Proven vendor selection framework — weighted criteria tailored for typical retail archetypes, plus scenario‑based scorecards to accelerate RFP shortlists.

Implementation playbooks — step‑by‑step approaches for greenfield, replatform, and lift‑and‑shift programs including integration patterns for POS, OMS, inventory, and CRM.

TCO and ROI models — configurable templates that incorporate licensing, professional services, cloud run costs, and incremental operational savings to produce multi‑year financials for executive approval.

Risk register and compliance checklists — focused on data privacy, cross‑border data flows, and vendor lock‑in scenarios, with mitigation plans and governance KPIs.

Use‑case benchmarks and KPIs — empirically derived performance baselines for conversion uplift, fulfillment latency, and cost per order across representative deployment archetypes.

Partner ecosystem maps — recommended systems integrators, managed services providers, and ISV partners appropriate for different platform strategies.

We intentionally withhold detailed regional and vertical segment tables in this briefing. These granular breakdowns, segmentation dynamics, and company share matrices are included in the full report — essential inputs for procurement negotiation and regional roll‑out planning.

Boards: adopt a three‑year strategic horizon for omni‑channel platform investments, with annual gating and capability milestones tied to measurable commercial outcomes (revenue lift, fulfillment cost reduction, customer lifetime value improvement).

CFOs and procurement: require vendor proposals to present a 5‑year TCO that includes infrastructure inflation scenarios and a clearly defined exit strategy to avoid long‑term lock‑in penalties.

CIOs and CTOs: build a modular target architecture that enables incremental modernization while protecting legacy investments critical to supply‑chain stability.

CMOs and heads of commerce: prioritise personalization and measurement capabilities that link experiences to unified customer profiles compliant with evolving privacy rules.

2026 will be characterised by faster execution of omnichannel programs, heightened attention to regulatory and infrastructure cost realities, and clearer differentiation between platforms that accelerate business outcomes and those that merely add technical complexity. PW Consulting’s Retail Omni‑Channel Commerce Platform Market report is designed to be an operational manual for executives — combining strategic market context, practical procurement tools, and vendor intelligence. For teams preparing capital asks, negotiating RFPs, or finalising a phased deployment plan, the full report provides the granular segmentation, vendor scoring, and financial templates necessary to de‑risk decisions and accelerate value capture.

Access the complete report to obtain the full segmentation tables, vendor scorecards, implementation templates, and the downloadable ROI/TCO models referenced in this brief. PW Consulting is available to run bespoke vendor shortlists, TCO workshops, and implementation readiness assessments tailored to your retail archetype and regional footprint.

For detailed analysis of this topic, please visit the official page:Retail Omni Channel Commerce Platform Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com