Saudi Arabia Food Fibers Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-24 10:16:46

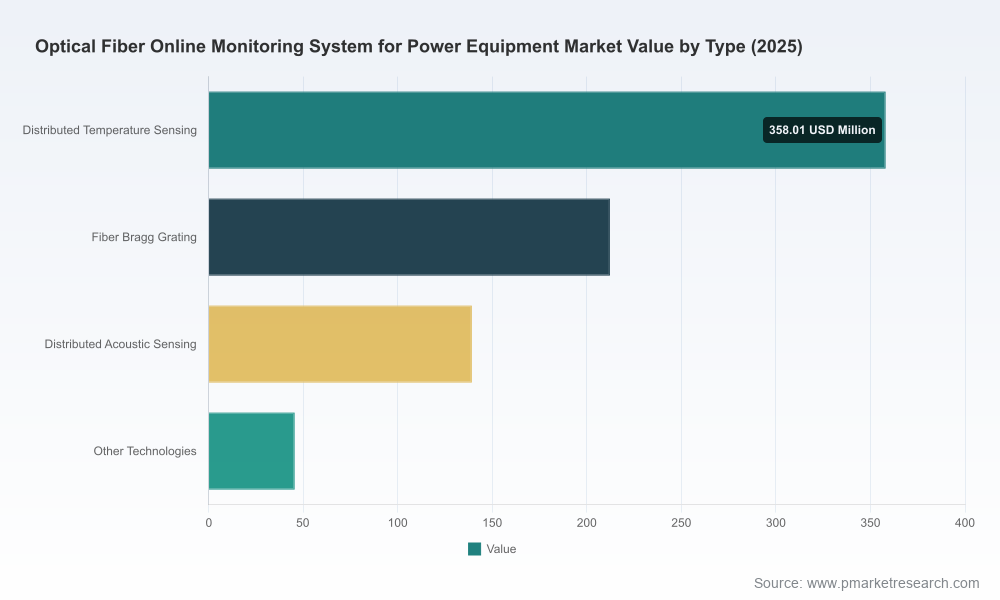

PW Consulting’s latest market brief on Optical Fiber Online Monitoring Systems for power equipment distills five years of historical performance and a seven-year forecast into an actionable strategic roadmap for energy utilities, grid technology vendors, project developers, and investors planning decisions in 2026. The industry is evolving from pilot deployments and point-solutions to integrated, grid-scale sensing platforms that materially change asset-management economics and operational risk profiles. Our analysis shows a clear growth trajectory: the global market expanded from USD 512.45 Million in 2020 to USD 755.0 Million in 2025 (base year), and — driven by accelerating electrification, OPGW integration, and vendor product maturation — is forecast to continue growing across 2026–2032 at a compound annual growth rate (CAGR) of 9.41%, reaching USD 1,417.24 Million by 2032. Figures are expressed in USD Million.

Optical Fiber Online Monitoring System For Power Equipment Market

Historical context: The market demonstrated steady expansion in 2020–2025 as utilities began systematically replacing reactive inspections with continuous fiber-optic sensing for temperature, strain, and acoustic anomaly detection.

Optical Fiber Online Monitoring System For Power Equipment Market

Near-term outlook: PW Consulting projects a 2026 market value of approximately USD 778.65 Million as the technology transitions from niche to mainstream operational deployments.

Optical Fiber Online Monitoring System For Power Equipment Market

Medium-term momentum: By 2027–2030, the market benefits from compounding effects of regulatory emphasis on grid resilience, Dynamic Line Rating (DLR) integrations, and retrofits of existing OPGW and fiber infrastructure, contributing to the higher end of the forecast curve toward USD 1.4 billion in 2032.

Competitive structure: Market concentration is moderate — the three-largest players account for about 32.4% of revenue (CR3) and the top five account for roughly 46.85% (CR5) — leaving room for focused incumbents and specialist challengers.

Moving from pilots to portfolio deployments: Project economics in 2026 favor scaling because unit costs decline with repeatable integration playbooks and the business case for continuous monitoring (reduced outages, deferred capex, safety) becomes easier to quantify.

Regulatory and operational drivers converge: New grid reliability requirements and the need to manage thermal risk in underground/urban corridors elevate demand for continuous DTS and complementary sensing modalities.

Infrastructure leverage: Existing OPGW and telecom fiber strands provide a cost-efficient route to distributed sensing; technology and service bundles that exploit these assets unlock faster ROI.

Vendor differentiation solidifies: Companies that combine sensing hardware with analytics, DLR integrations, and clear TCO models gain decisive competitive advantage.

Decision-ready market sizing and growth scenarios — Base year 2025, historical review (2020–2025), and a detailed forecast window for 2026–2032 with alternative scenarios tied to adoption rates and regulatory shifts.

Commercial playbooks for procurement and deployment — Step-by-step guidance on vendor selection, RFP framing, proof-of-concept templates, integration checklists for OPGW/OPF retrofits, and standard KPIs for operational handover.

TCO and lifecycle models — Financial templates that quantify CapEx, OpEx, avoided outage costs, and service contracts over 10–15 year lifecycles; sensitivity analyses to stress-test assumptions.

Vendor scorecards and partner matrices — Comparative assessment of capability clusters (long-range DTS, distributed strain, DAS/AE, analytics), commercial traction, and scaling readiness; each profile includes strengths, risk vectors, and suggested use-case fit.

Technical deployment guidance — Practical notes on fiber routing, interface with protection/control systems, data latency and cybersecurity considerations, and maintenance regimes that reflect typical field service lifetimes.

Use-case playbooks — Focused modules for power cable hotspots, transmission line dynamic rating, transformer monitoring, and switchgear condition monitoring, each with measurable outcomes and pilot-to-scale roadmaps.

Strategic scenarios — Competitive and regulatory scenario planning designed to support investment committees and corporate strategy teams through 2032.

The market combines specialist sensing manufacturers, optical test vendors, and diversified industrial groups. PW Consulting’s qualitative and quantitative analysis emphasizes product differentiation, field-proven deployments, and integration capabilities rather than headline vendor claims.

AP Sensing GmbH (Böblingen, Germany) — A leading DTS specialist offering real-time temperature profiling for high-voltage assets. Recent strategic partnership activity (February 2026) to combine distributed sensing with Dynamic Line Rating (DLR) signals a market move toward bundled sensing + operational optimization services that enhance line capacity management.

VIAVI Solutions Inc. (Chandler, Arizona, USA) — Brings robust fiber-test and sensing portfolios (including DTS variants) with strong global channel reach. Their strength lies in coupling test instrumentation and continuous monitoring solutions for utility-grade deployments and long-term asset visibility.

Luna Innovations (Roanoke, Virginia, USA) — Developer of long-range distributed strain and temperature systems (EN.SURE) focused on extended monitoring distances. Their technology is relevant for projects that require single-span or long-distance sensing without frequent nodes.

Sumitomo Electric Industries (Osaka, Japan) — Industrial scale supplier offering fiber-integrated sensing products designed for embedded cable monitoring and asset lifecycle integration, targeting utility and OEM partnerships.

Prisma Photonics (Israel) — Notable for solutions that convert existing OPGW/telecom fiber into distributed sensors; a significant deployment in California (December 2025) demonstrates the commercial viability of retrofit strategies at utility scale.

Bandweaver (UK) — Offers DTS platforms tailored for grid and cable monitoring; player model focuses on turnkey sensing platforms and integration into utilities’ SCADA ecosystems.

OSENSA Innovations (Canada) — Specialist in fiber temperature monitoring for switchgear and stator windings; strong position in targeted equipment-level monitoring where close-coupled sensors provide high diagnostic value.

Yokogawa Electric Corporation (Tokyo, Japan) — Markets distributed temperature sensing systems with an emphasis on safety, operational continuity, and industrial controls integration.

EXFO (Quebec City, Canada) — Provides OTDR-based remote fiber testing and monitoring solutions that complement sensing deployments by ensuring fiber health and rapid fault localization.

Regulatory tailwinds: Fiber-optic sensing solutions (DTS and DAS) mitigate electromagnetic interference concerns and provide continuous profiles that support grid reliability mandates as electrification increases.

Infrastructure enablers: OPGW integration turns transmission assets into sensing platforms capable of measuring temperature, strain, and acoustic events over hundreds of kilometers — a crucial cost lever for utilities evaluating retrofit strategies.

Service life and maintenance: Optical fiber sensing technologies such as Fiber Bragg Gratings and DTS variants have long in-service lifetimes; DTS systems can require minimal maintenance for 10–15 years in typical grid environments, lowering long-term ownership costs.

Embed sensing in capex planning: Treat fiber-based monitoring as a portfolio-level enabler that can reduce near-term O&M spend and defer certain replacement projects. Use the report’s TCO models to quantify trade-offs.

Prioritize pilots that validate value chain handoffs: Design pilots that produce operational KPIs usable by protection engineers, asset managers, and commercial planners — not just laboratory performance metrics.

Choose vendors by capability clusters: Shortlist suppliers based on technical fit (long-range vs. distributed strain vs. equipment-level), analytics maturity, and proven field deployments rather than vendor size alone.

Plan for fiber-health management: Incorporate OTDR-based testing and service-level agreements that ensure sensor network availability matches the criticality of the monitored asset.

Integrate with DLR and grid-optimization tools: Look for bundled offers (or partnerships) that combine sensing with Dynamic Line Rating and analytics to unlock immediate operational value, as exemplified by recent vendor alliances.

Factor regulatory changes into scenario planning: Use the report’s scenario modules to stress-test adoption under varied regulatory and electrification pathways.

This “trailer” is designed to demonstrate the analytical depth and practical utility of PW Consulting’s full report while preserving the proprietary granularity that supports executable procurement and investment plans. The full report contains the detailed regional and application segmentation, granular vendor benchmarking, downloadable financial models, and implementation templates that operational teams and C-suite executives need to commit capital in 2026.

For procurement teams, we recommend starting with the report’s RFP template and vendor scorecard. For strategy teams, use the scenario outputs and TCO models to align board-level capital decisions. For vendors, the competitive analysis and use-case gaps will help prioritize product development and partnership strategies.

As utilities and grid operators reframe asset management around continuous sensing, 2026 represents a pivotal year to convert experimental pilots into enterprise programs. PW Consulting’s Optical Fiber Online Monitoring System For Power Equipment market report provides the evidence base, practical instruments, and strategic scenarios necessary to make those decisions with confidence. Access the full dataset and proprietary appendices on our website to unlock the vendor-level details and segmentation required for transaction-ready planning.

For detailed analysis of this topic, please visit the official page:Optical Fiber Online Monitoring System For Power Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com