Thermoplastic Conductive Additives: Strategic Imperatives for 2026 — PW Consulting Market Brief

As thermoplastic conductive additives move from niche technical enablers to mainstream design levers across electronics, automotive, packaging and industrial systems, corporate leaders face a pivotal planning year in 2026. PW Consulting’s new market study — built on a 2025 base year with historical analysis covering 2020–2025 and forward forecasts to 2032 — synthesizes the commercial, technological and regulatory signals that will determine winners and losers in the coming investment cycle. The headline: the overall market is sizeable and accelerating, rising from roughly USD 2.52 billion in 2025 to an expected USD 4.73 billion by 2032, with a compound annual growth rate of approximately 9.4% in the 2026–2032 forecast window. This brief highlights the strategic value of the full report for 2026 corporate decision-making while preserving our proprietary subsegment detail to encourage direct engagement with PW Consulting for transaction-level insight.

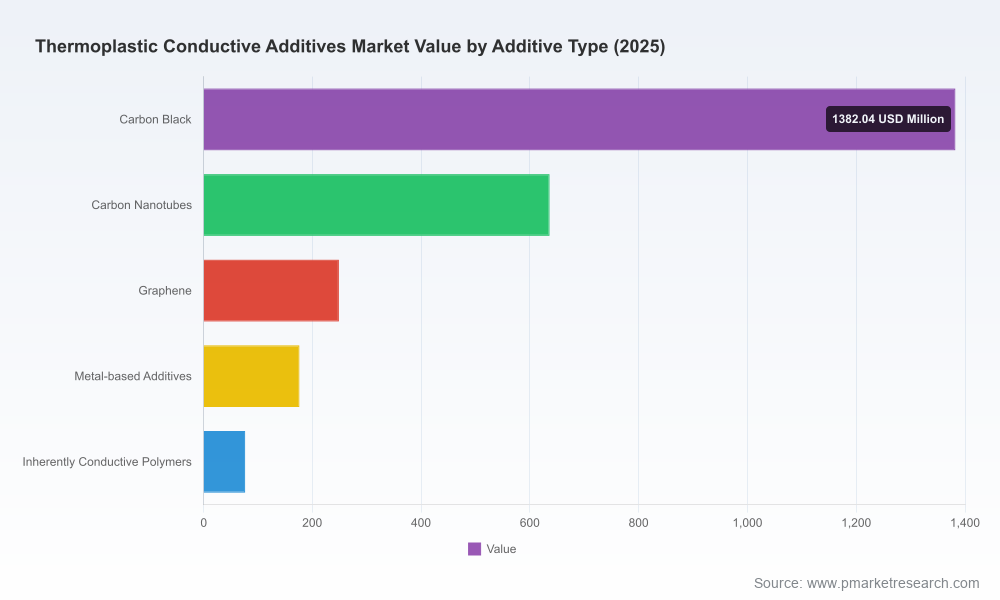

Thermoplastic Conductive Additives Market

Why 2026 Is a Strategic Inflection Point

Three converging forces make 2026 a decision-heavy year for buyers, compounders, and additive providers:

Thermoplastic Conductive Additives Market

- Product-driven demand is maturing — end-markets such as electric vehicles, consumer electronics miniaturization, and industrial electrification are driving higher-performance conductive requirements (thermal management, EMI shielding, ESD control) that push material choices beyond legacy carbon black blends.

- Supply-side evolution — investments in next-generation graphene and nanotube capacity, together with compounder plant additions in North America and other regions, are shifting cost, lead time and formulation dynamics.

- Regulatory and feedstock pressures — scrutiny of certain carbon materials in Europe and volatility in upstream feedstocks raise procurement and substitution risk for incumbent supply chains.

For leaders setting 2026 budgets, these dynamics imply that tactical procurement and product road-mapping decisions will have multi-year consequences for cost, performance and regulatory compliance.

Thermoplastic Conductive Additives Market

What the PW Consulting Report Delivers (Practical, Executable Outputs)

Our study has been designed to convert market intelligence into executable strategy. The full report includes:

- Transparent market sizing and forecasting models (2020–2032) with downloadable model files you can stress-test against your own scenarios.

- Commercial due diligence kits for M&A and JV processes: comparable vendor scorecards, margin and ASP benchmarking, and commercially verifiable growth assumptions.

- Technology and formulation roadmaps that map additive types to achievable electrical/thermal performance bands and manufacturability constraints for key thermoplastic families.

- Supply-chain heat maps and supplier dependency matrices that reveal single points of failure and opportunities for localization or dual sourcing.

- Regulatory impact assessment and mitigation playbooks addressing emerging chemical evaluations and end-market compliance needs.

- Go-to-market playbooks for compounders and material suppliers — pricing levers, channel strategies, co-development templates and specification capture tactics for OEMs.

- Investor-focused intelligence: target lists, transaction case studies and an assessment of market concentration and competitive defensibility.

We deliberately omit raw sub-segment tables from this brief. The full dataset, including regional and application breakouts and additive-type share detail, is available only in the paid report and interactive model — precisely the level of granularity procurement teams and corporate M&A functions require to make 2026 commitments.

Competitive Landscape — Who Matters and Why

The market exhibits moderate concentration, with a small set of global suppliers capturing a substantial share of market value. That topology shapes partnership and acquisition strategies: global compounders and specialist additive manufacturers both play complementary roles in the value chain.

- Cabot Corporation — A global carbon black leader with deep application engineering capability. Cabot’s conductive concentrates and CABELEC compounds remain go-to solutions where established, cost-effective conductivity is required at scale. Strategy implication: Cabot is a defensive supplier for traditional ESD and static-dissipation applications; OEMs should assess longevity under shifting regulatory landscapes and consider parallel sourcing where high-performance applications demand alternative nanomaterials.

- Avient Corporation — Combines compounder scale with proprietary conductive formulations for thermal and electrical management. Avient plays a bridge role between formulation expertise and direct OEM engagement. Strategy implication: joint development or preferred-supplier models with Avient can accelerate time-to-market for OEMs needing validated compound performance.

- RTP Company — Known for customized conductive compounds and flexible production footprints. RTP’s strength is rapid tuning across molding and extrusion platforms. Strategy implication: attractive partner for tier-1 tooling-dependent programs and for firms seeking lower barrier-to-entry productization of conductive masterbatches.

- SGL Carbon and Imerys — Specialty graphite and carbon-based filler suppliers that add thermal conductivity and structure-preserving options. Their materials are critical where processing windows are tight and thermal management is prioritized. Strategy implication: combine these high-conductivity fillers with polymer engineering to trade off loading vs mechanical performance.

- LATI, Teknor Apex, Americhem, SABIC — Compounders and polymer producers with strong application reach (automotive, medical, consumer electronics). They offer scale and multi-material formulations. Strategy implication: these firms are logical co-development partners for OEMs seeking integrated polymer-additive solutions at production scale.

- OCSiAl — A leading single-wall CNT supplier providing low-loading conductivity solutions. Strategy implication: for high-performance, low-influence additive strategies (maintaining mechanical properties while adding conductivity), CNTs are a compelling route but require validated dispersion approaches and supply agreements.

- LEHVOSS, Bekaert — Specialized fillers (metal fibers, high-thermal graphites) that enable niche, high-conductivity or EMI/structural use-cases. Strategy implication: consider these suppliers where composite performance (e.g., EMI + structural) must be delivered from a monolithic part.

Recent industry moves underscore this competitive picture: specialist graphene players announced capacity and compounding partnerships in 2025, and several compounders expanded North American production during the year. These actions signal a transition from early R&D pilots to commercial-scale deployment for higher-performance nanocomposites.

Supply-Chain and Raw-Material Dynamics to Watch in 2026

Raw material and regulatory signals will materially affect supplier economics and substitution dynamics in 2026:

- Upstream feedstock trends are creating price pressure and potential allocation risk for traditional carbon black supply. Procurement strategies must include contingency plans and cost-pass frameworks.

- Carbon nanotubes are entering a phase of capacity growth that supports broader commercial adoption as conductive additives, but integration challenges (dispersion, cost-per-performance) remain a gating item for widespread substitution.

- Regulatory evaluations of certain carbon materials in Europe and other jurisdictions are active on multi-year timelines. Companies should model regulatory scenarios and pre-qualify alternative additive technologies to de-risk product roadmaps.

Recommended 2026 Decision Framework — Three Pragmatic Playbooks

To convert market intelligence into action, PW Consulting recommends three complementary playbooks for 2026:

- Supplier Risk & Cost Resilience

- Implement a dual-sourcing strategy that pairs incumbent carbon-black suppliers with at least one alternative low-loading nanomaterial supplier.

- Build cost-pass and hedging clauses into multi-year supply agreements where feedstock volatility materially impacts margin.

- Performance Platform & Co-Development

- Establish focused co-development projects with compounders or nanotube/graphene technology providers to accelerate validated formulations for high-growth end-markets (EV, EMI shields, thermal solutions).

- Pilot on existing tooling to de-risk scale-up and preserve mechanical performance while achieving required conductivity levels.

- M&A and Capacity Strategies

- Assess bolt-on acquisitions of specialized additive manufacturers or local compounders to secure technology and shorten lead times in critical regions.

- Prioritize targets that enhance proprietary dispersion technology, regulatory compliance capabilities, or regional production presence.

How PW Consulting’s Report Supports Execution

For executive teams, the report is more than a market map — it is a toolkit designed to be operationalized in 2026 planning cycles. Subscribers receive an interactive forecast model (scenario toggles for substitution rates, raw material shocks and regulatory outcomes), a prioritized list of acquisition and partnership targets, and templated commercial agreements and technical acceptance criteria to shorten procurement cycles.

We intentionally avoid publishing the underlying sub-segment numerical tables in this release to protect the commercial sensitivity of our client-grade dataset. If your 2026 decisions hinge on actionable regional, additive-type and application-level splits, supplier-by-supplier market shares, or price/margin benchmarks, the full report and accompanying data model provide that precision.

Next Steps

PW Consulting is offering guided briefings for executive teams and tailored deep-dive workshops aimed at translating the market intelligence into investment roadmaps and procurement actions for 2026. Contact our advisory team to schedule a briefing and obtain the full dataset, interactive forecast, and the proprietary supplier and target lists needed to act decisively this year.

In an era where materials choices determine product differentiation and supply resilience, 2026 will reward organizations that combine proactive sourcing, targeted technology partnerships, and disciplined M&A to lock in performance and capacity. PW Consulting’s Thermoplastic Conductive Additives report is designed to be the operational spine for those decisions.

For detailed analysis of this topic, please visit the official page:Thermoplastic Conductive Additives Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com