U.S. Renewable Diesel Market Research Report: Opportunities, Challenges & Forecast

Art |

2026-05-29 07:54:24

PW Consulting today releases a strategic industry briefing drawn from our comprehensive Human ELISA Kits Market report (base year 2025, forecast 2026–2032). The market has expanded from an estimated USD 1,745.2 Million in 2020 to USD 2,385.4 Million in 2025 and is forecast to reach approximately USD 3,646.4 Million by 2032, reflecting a compound annual growth rate (CAGR) of 6.25% over the forecast period. For executives preparing 2026 business plans, this trajectory underscores both growth opportunity and intensifying commercial and regulatory complexity.

Human Elisa Kits Market

Investment prioritization — allocate R&D and capex to assay formats and use-cases that deliver defensible margins and regulatory optionality.

Human Elisa Kits Market

Portfolio strategy — decide which assays to maintain as research-use-only (RUO), which to pursue for clinical translation, and which to sunset.

Human Elisa Kits Market

M&A and partnership screening — identify targets and partners whose capabilities accelerate time-to-ISO/IVD or fill supply-chain gaps.

Commercial go-to-market planning — match channel, pricing and service models to evolving buyer expectations in research and clinical development settings.

Operational readiness — ensure manufacturing quality systems, lot-to-lot consistency, and logistic resilience ahead of demand scaling.

The market’s mid-single-digit CAGR masks differentiated drivers across technology, end-use, and regulatory vectors. Continued investment in biomarker discovery (oncology, infectious disease, immunology), rising demand for quantitative protein assays in translational research, and service expectations from contract research organizations are core growth engines. Simultaneously, a structural shift is underway: a meaningful subset of incumbent suppliers is investing in quality systems and regulatory pathways to migrate select products from RUO to clinical-grade or companion-diagnostic positioning. Our analysis shows moderate market concentration — the top three suppliers account for a material share of market revenues, and the top five extend that dominance — a dynamic that shapes pricing power, distribution reach and innovation diffusion.

Regulatory posture remains a strategic inflection point. Most commercial human ELISA kits continue to be designated RUO and are not intended for diagnostic use; however, the pathway from RUO to FDA-authorized IVD status is being traversed by a growing number of products (a prominent example being a companion diagnostic authorization in mid‑2025). Organizations that fail to define clear regulatory roadmaps risk opportunity loss or delayed market access if customers demand clinical-grade sourcing.

Our vendor mapping focuses on commercial footprint, product breadth, quality certifications, go-to-market models and areas of technical differentiation. Below are high-level strategic profiles of leading suppliers covered in the report; specific vendor scores and segment-level rankings are available in the full study.

Bio-Techne (R&D Systems) — Recognized for a deep catalog (Quantikine, DuoSet) and extensive citation footprint across thousands of targets. Strengths: brand credibility in academic and translational settings; weakness: premium price positioning that may limit adoption in price-sensitive segments.

Thermo Fisher Scientific — Broad platform and distribution strength across Invitrogen-branded kits and reagent ecosystems. Strengths: channel reach and integrated workflows; strategic advantage in bundling reagents with instrumentation and consumables.

Abcam — Rapid citation growth and focus on assay specificity. Strengths: high-sensitivity assays and researcher trust; opportunity: leverage digital content and validation data to accelerate uptake in clinical development teams.

Bio‑Rad Laboratories — Well-positioned in immunology and biomarker research with standardized kits and supportive technical services. Strengths: technical support and assay reproducibility for institution buyers.

Boster Biological Technology — Noted for ISO 13485 certification for kit development and production, signaling readiness for clinical-grade supply. Strengths: certification; implication: attractive partner for companies seeking contract manufacturing with quality credentials.

BioLegend, LifeSpan BioSciences (LSBio), Elabscience — Growing adoption in cytokine and target-specific niches, with investible differentiation in reagent quality and catalog breadth.

Biomatik & ICL Lab — High SKU counts and rapid fulfillment models appeal to research customers needing breadth and speed; strategic focus should be on building validation packages for translational customers.

Proteintech Group — Emphasizes validated kits for natural samples (serum, plasma), addressing reproducibility demands in translational studies.

Surmodics IVD — Supplies critical immunoassay components from ISO-certified facilities, representing an upstream play in the value chain for companies opting to assemble clinical-grade kits.

Recent regulatory developments — notably an FDA de novo authorization for a companion diagnostic ELISA in mid‑2025 — show that IVD pathways are both feasible and strategically impactful. This creates a bifurcated landscape: a broad RUO market with price and speed competition, and an emergent clinical-grade segment with higher entry barriers and margin potential.

Granular market model (2020–2032) by product type and application with bottom-up methodology and sensitivity scenarios.

Vendor scorecards and competitive positioning matrices (quality systems, citation impact, SKU depth, channel reach).

Regulatory matrix mapping RUO/IVD pathways, certification requirements (ISO 13485, 9001) and typical timelines and cost brackets for clinical transition.

Go-to-market playbooks for research vs. clinical segments, including pricing levers, distributor vs. direct models, and service bundles.

Manufacturing and supply-chain risk assessment with mitigation checklists for lot-to-lot consistency, reagent sourcing, and contract manufacturing options.

M&A and partnering pipeline: target screening criteria, due-diligence scorecards, and accretion/dilution modeling templates.

Actionable product launch and commercial scaling templates including P&L impact, NPV/IRR scenarios, and first-12-month operational milestones.

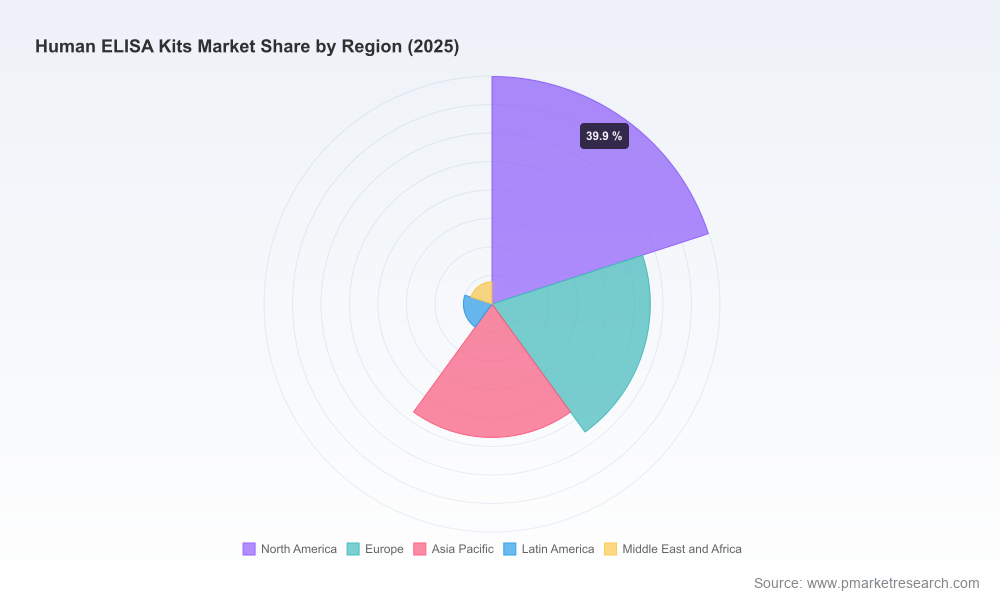

To preserve commercial confidentiality and maintain the strategic “trailer” principle of this release, the report summary here intentionally omits specific segment-level revenue splits, regional breakdowns, and proprietary vendor scores. These detailed datasets and the underlying modeling assumptions are available in the full PW Consulting report.

Define a bifurcated product strategy: Maintain a lean, competitively priced RUO portfolio for broad research adoption while selectively investing in clinical-grade variants for high-value biomarkers where reimbursement or companion-diagnostic positioning exists.

Invest in quality systems now: Achieve or partner for ISO 13485 certification where clinical translation is a priority — this is a multi-quarter program that should be budgeted for 2026 execution.

Prioritize partnerships for speed-to-market: Use contract manufacturing organizations with proven ISO credentials or distribution partners with clinical-channel reach to accelerate access without duplicative capex.

Strengthen validation packages: Publish robust lot-to-lot and matrix validation data to reduce buyer friction in translational settings and to support regulatory submissions.

Use M&A tactically: Target assets that provide regulatory-ready platforms, complementary immunoassay chemistries, or fill distribution gaps — aim for tuck-ins that shorten clinical development timelines.

Differentiate through services: Offer assay optimization, validation services, and digital result interpretation tools to capture higher-margin service revenue and stickier customer relationships.

Quantify supply-chain exposures: Scenario-test single-supplier reagents and long-lead components; secure alternate sourcing in 2026 to avoid production bottlenecks as demand scales.

Boards and executive teams should use the macro projections and playbooks in this briefing to stress-test product investments, regulatory timelines and distributor negotiations. Short-term (Q1–Q2 2026) priorities include committing to quality-system investments where clinical translation is targeted, accelerating validation studies for priority assays, and initiating any M&A or partnership diligence that would be needed to meet late‑2026/early‑2027 commercialization timelines.

For market entrants and incumbents alike, the core strategic choice is clear: compete on cost and speed in the large RUO market, or invest to play in the smaller but higher-margin clinical/companion-diagnostic space. Both strategies can be profitable, but they require different organizational structures, KPIs and capital plans.

PW Consulting’s full Human ELISA Kits Market report contains the complete data tables, segment-level forecasts, vendor scorecards, and executable templates referenced in this briefing. We designed the report to be a practical decision-making tool for 2026 — from head-of-R&D to CFO and corporate development teams. This press release intentionally omits granular segmentation figures and proprietary scores to encourage direct engagement with our analysts and to ensure readers receive the full, validated dataset.

To request an executive briefing or obtain the full report and supporting models, visit the PW Consulting reports portal or contact our industry practice lead. PW Consulting’s analyst team stands ready to run tailored workshops that translate the market model into company-specific financial scenarios for 2026 budget season.

For detailed analysis of this topic, please visit the official page:Human Elisa Kits Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com