Seaweed-Based Packaging Market: Strategic Insights for 2026 — PW Consulting Report Preview

PW Consulting’s forthcoming Seaweed Based Packaging Market report (base year 2025) consolidates the most actionable intelligence available for corporates, investors, and public-sector buyers evaluating seaweed-derived alternatives to fossil plastics. This preview outlines why the market matters for 2026 decision cycles, how the category’s macro trajectory reshapes sourcing and product strategies, and where C-suite and business unit leaders should focus immediate attention. The full report delivers the granular data, regional and application splits, and modelled scenarios underlying the conclusions summarized here.

Seaweed Based Packaging Market

Executive snapshot: a market accelerating to scale

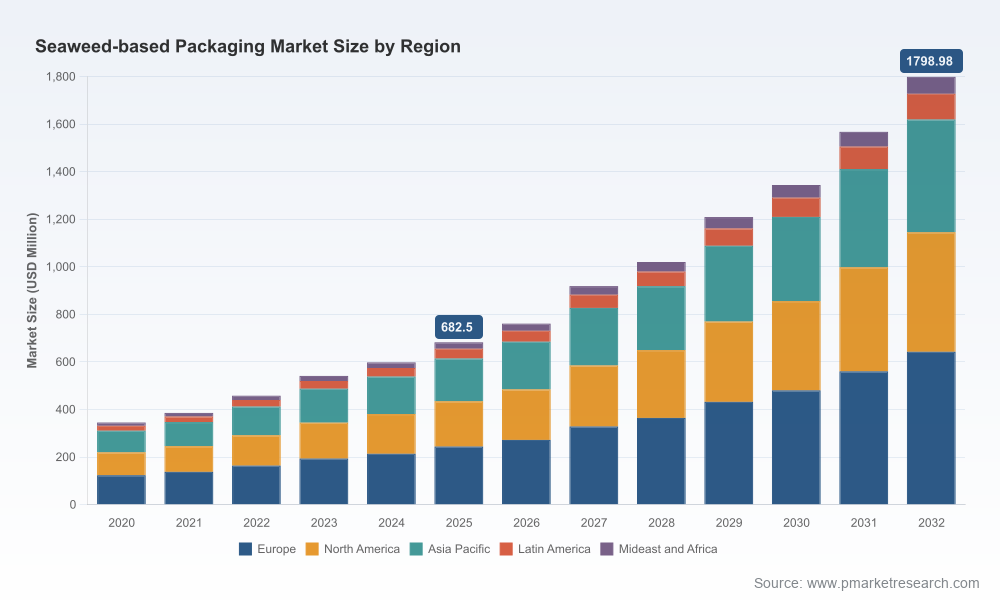

Seaweed-based packaging is moving from proof-of-concept to commercial adoption. PW Consulting’s model projects global market revenues rising from USD 682.5 million in 2025 to approximately USD 1.80 billion by 2032 — a compound annual growth rate (CAGR) of 14.85% over the forecast period. The sector’s growth is driven by converging forces: regulatory pressure on chemical additives and PFAS, rising Extended Producer Responsibility (EPR) fees tied to recyclability, stronger retail and brand commitments on packaging sustainability, and rapid innovation in formulation and manufacturing that improves performance parity with conventional polymers.

Seaweed Based Packaging Market

Why this matters for 2026 corporate decision-making

- Timing of regulatory inflection points: From mid-2026, new enforcement and labelling regimes (notably the EU’s Packaging and Packaging Waste Regulation) restrict PFAS and tighten food-contact requirements. Companies with multi-year procurement cycles must align specifications now to avoid costly reformulation or compliance-driven product delays.

- Cost and margin calculus: Raw-material volatility — particularly for alginate- and carrageenan-derived feedstocks — has raised unit costs and supplier risk profiles. Near-term procurement strategies will determine whether teams optimize for total landed cost or prioritize lower-carbon / PFAS-free alternatives.

- Operational readiness: Scale-up investments for extrusion, thermoforming, coating and conversion tooling differ across seaweed formulations. Decisions on co-manufacturing partnerships and pilot investments made in 2026 will materially affect 2027–2028 time-to-market.

- Competitive positioning: Early adopters who convert legacy mono-material packaging to certified seaweed blends — or who integrate edible/coating concepts for new SKUs — can capture premium shelf placement and meet retail sustainability scorecard thresholds gaining traction in EPR frameworks.

Market dynamics: drivers, constraints and inflection points

- Regulatory push-pull: The EU’s PPWR phase-in (including PFAS limits in food-contact materials) and tightening EPR schemes in the UK and several U.S. states materially increase the economic attractiveness of PFAS-free seaweed solutions. These regulations effectively recalibrate the lifecycle cost of packaging options.

- Raw-material supply and price pressure: Supply tightness in seaweed feedstocks has elevated the market cost base for key inputs. Refined carrageenan and alginate price movements have been pronounced in recent quarters, and procurement teams should assume continued volatility until cultivation and processing scale improve.

- Technology transition: A wave of formulation breakthroughs and resinization efforts is improving barrier properties and thermal stability. At the same time, some seaweed-based materials remain best suited to specific use-cases (coatings, sachets, flexible films) rather than universal replacement, which informs a selective product roadmap.

- Fragmented supplier landscape: Market concentration remains low: the top three suppliers account for a minority share of global sales, and the top five do not yet approach consolidation levels typical of mature polymer markets. This creates both opportunity and risk — numerous agile innovators versus a limited number of scale-focused players.

Operational implications for value-chain players

PW Consulting identifies discrete actions for exporters, converters, brands and investors seeking to de-risk adoption and accelerate commercialization:

Seaweed Based Packaging Market

- Brands & retailers: Fast-track packaging specifications around PFAS-free and compostability claims, pilot multi-pack SKUs with seaweed coatings, and update vendor scorecards to reflect emergent EPR fee structures.

- Converters: Prioritize retrofittable processing lines and standardize testing protocols for barrier and shelf-life performance to reduce customer onboarding friction.

- Seaweed suppliers & cultivators: Invest in vertical integration for drying and refining capacity; partner with resinizers to deliver consistent rheology and compound-grade feedstocks.

- Investors: Focus on scale-enabling plays: manufacturing capacity, bio-resin platforms compatible with existing extrusion equipment, and service providers that accelerate regulatory compliance.

Competitive landscape — who’s shaping the category

The space combines heritage innovators, deep-tech startups, and scaling ventures. PW Consulting’s competitive review profiles leading and promising players across technologies and geographies. Representative entities analyzed in the report include:

- Notpla Limited (London): Known for seaweed-coated food containers, biodegradable cutlery and the Ooho liquid pods, Notpla is advancing fully natural, home-compostable coffee cup concepts with multi-partner EU funding.

- Sway Innovation Co. (California): Focused on home-compostable flexible films and a thermoplastic resin intended as a direct replacement for single-use plastic films; notable for partnerships with apparel brands and distributor-driven market entry.

- Evoware (Indonesia): Specialises in edible sachets and films for dry foods and instant noodles, leveraging regional seaweed supply strengths for cost-competitive formats.

- LOLIWARE (US): Developing edible and compostable single-use items aimed at beverage and event markets, with strong brand positioning.

- B'ZEOS, Zerocircle, FlexSea, Kelpi, Uluu, PlantSea: A mix of EU, UK, India, Australia and Switzerland-based innovators covering films, coatings, resins, and scaled manufacturing efforts — each pursuing different technical and go-to-market paths.

Recent funding and partnerships underscore investor interest and commercialization momentum: examples include multi‑million funding rounds for production scale-up, government-backed R&D consortia to replace plastic linings in cups, and brand partnerships piloting seaweed polybags and retail films.

What the PW Consulting report contains (practical, executable content)

The full report is constructed to inform Board- and investor-level decisions and to be directly usable by procurement, packaging development and sustainability teams. Key deliverables include:

- Granular historic and forecast market modeling (2020–2032) with sensitivity scenarios tied to raw-material price trajectories and regulatory adoption timelines.

- Go-to-market playbooks for five archetypal buyers (large CPGs, regional retailers, contract packagers, ingredient suppliers, and private equity investors) including pilot KPIs and procurement checklists.

- Technology readiness assessments mapping barrier performance, thermal processing constraints and recyclability/compostability certification pathways.

- Supply-chain risk maps and a shortlist of contract-manufacturing and co-packing partners by region.

- Commercial due-diligence templates and an M&A valuation primer tailored to seaweed-based assets.

- Regulatory matrix covering EU, UK and U.S. state-level EPR/food-contact developments and recommended compliance roadmaps.

To preserve commercial value for report subscribers, the document intentionally summarizes high-level segmentation and scenario outcomes in this preview while reserving detailed regional, application and type-level splits for the full report.

Strategic recommendations for 2026

- Prioritize compliance-first pilots: Launch product pilots that specifically address PPWR and EPR exposure points — e.g., food-contact SKUs with demonstrable PFAS-free claims and certified end-of-life pathways.

- Lock in feedstock hedges: Negotiate medium-term procurement contracts with cultivated seaweed suppliers and blended feedstock providers to mitigate raw-material price spikes while supporting traceability requirements.

- Invest in modular scale-up: Rather than greenfield facilities, prefer modular retrofit investments that allow switching between seaweed resins and conventional polymers to manage demand uncertainty.

- Embed lifecycle economics: Rework packaging TCO models to internalize EPR fees, waste management costs, and potential shelf-premium capture from sustainability-labelled SKUs.

- Monitor consolidation catalysts: Track capital flows — especially Series A/B rounds targeting manufacturing capacity and resin platforms — that could compress supplier fragmentation and alter bargaining dynamics.

How PW Consulting can help

For organisations preparing 2026 capital plans or product roadmaps, the full PW Consulting report supplies the quantitative foundations and execution playbooks required to move from exploration to commercial roll-out. Our engagement options include customised market-sizing for client-specific product portfolios, procurement strategy workshops, and technical matchmaking between converters and seaweed resin developers.

Next steps

This preview highlights strategic conclusions and the operational decisions companies must confront in 2026. For the detailed regional and application-level forecasts, scenario model files, supplier scorecards and the full set of templates and checklists, visit the PW Consulting report landing page or contact our advisory team to schedule a briefing and obtain subscriber access.

For detailed analysis of this topic, please visit the official page:Seaweed Based Packaging Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com