Fiduciary Wealth Management: Trusted Strategies for Long-Term Financial Growth

Other |

2026-05-27 04:52:08

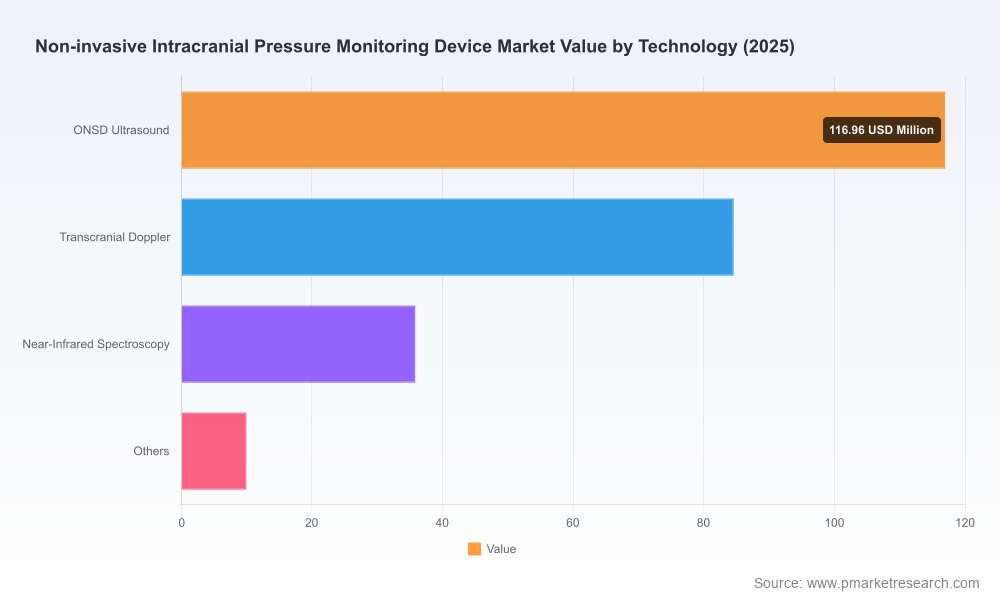

The non‑invasive intracranial pressure (ICP) monitoring market is entering a strategic inflection point. After steady expansion through the first half of the decade, the global market has moved from an early validation phase to an adoption phase that combines regulatory momentum, accumulating clinical evidence, and growing payer interest. Our PW Consulting report (base year 2025; historical window 2020–2025; forecast 2026–2032) quantifies that trajectory: the market grew from approximately USD 169.5 Million in 2020 to about USD 247.26 Million in 2025 and is forecast to approach USD 419.67 Million by 2032 — a compounded annual growth rate of 7.85% across the projection window. For executive teams planning 2026 decisions, understanding the interplay among clinical validation, regulatory pathways, reimbursement readiness and competitive positioning is now table stakes.

Non Invasive Intracranial Pressure Monitoring Device Market

Shift from niche to mainstream: Non‑invasive ICP technologies are moving from proof‑of‑concept to operational use in neurocritical care and related settings. Decision makers must decide whether to invest in organic product development, partner with emerging vendors, or pursue M&A to secure time‑to‑market.

Non Invasive Intracranial Pressure Monitoring Device Market

Regulatory and consensus pressure: Recent regulatory clearances and consensus statements are reshaping acceptable use cases. These influences materially affect product development timelines, clinical trial design and commercialization strategies.

Non Invasive Intracranial Pressure Monitoring Device Market

Commercial opportunity size and tempo: The mid‑ to long‑term revenue opportunity is substantial and predictable enough to support strategic investments in manufacturing scale, clinical support networks and payer engagement—provided firms align near‑term activities with expected clinical adoption curves.

Clinical evidence is accelerating but uneven. High‑quality, large‑cohort publications are beginning to appear; for example, a 2025 publication demonstrated strong relative performance of a cranial expansion sensor against other non‑invasive methods in absolute ICP estimation. Such studies validate the category but also reveal variability in accuracy across devices and patient subgroups—creating opportunities for first movers that can demonstrate both accuracy and consistent clinical utility.

Regulatory trajectories are favorable yet exacting. Regulators are clarifying expectations: existing standards (e.g., device accuracy bands) remain reference points for clinical acceptability, and some innovators are receiving expedited regulatory pathways. A Breakthrough Device designation for a telemetric non‑invasive system underscores how regulators will prioritize patient‑impact innovations, particularly for long‑term hydrocephalus management and telemonitoring use cases.

Consensus guidelines and multimodal recommendations are accelerating clinical uptake. The recent B‑ICONIC consensus advocates multimodal non‑invasive approaches for traumatic brain injury management in settings where invasive monitoring is unavailable—raising the value proposition for vendors that can offer integrated or interoperable solutions.

Payer and hospital economics are increasingly supportive. Reimbursement environments are moving from neutral to constructive for validated non‑invasive solutions, especially when devices reduce ICU stays, enable outpatient management, or substitute invasive procedures without compromising outcomes.

The competitive field is a mix of specialized startups with disruptive sensing modalities and established medtech incumbents with deep clinical relationships. Market concentration metrics indicate moderate fragmentation: the top three companies account for a meaningful but not dominant share, and the top five tighten that position—creating a market structure that supports both independent growth and acquisitive consolidation.

brain4care — A differentiated wearable cranial expansion sensor with FDA 510(k) clearance and a large clinical publication in 2025. Strengths: real‑world validation, regulatory precedent, and a clear go‑to‑market starting point. Strategic implication: a potential acquisition or partnership target for companies seeking rapid market entry with an FDA‑cleared platform.

Crainio — Early commercial entrant developing a forehead probe that combines low‑power infrared photoplethysmography and machine learning for real‑time ICP estimation, targeting clinical availability around 2027. Strengths: ML‑driven estimator and low‑cost sensor form factor. Strategic implication: watch for clinical validation milestones and plan channel strategies around a likely 2027 entry.

Nisonic — Ultrasound‑based transorbital imaging approach focusing on optic nerve and sheath analysis. Strengths: leverages established ultrasound pathways and clinician familiarity. Strategic implication: attractive for partnerships with companies seeking to bundle non‑invasive imaging with analytics.

Viasonix & NovaSignal — Vendors with TCD (transcranial Doppler) expertise offering cerebral blood flow monitoring systems useful for ICP‑related assessment. Strengths: strong clinical recognition in vascular and neurocritical settings. Strategic implication: incumbents to consider for multimodal integration or distribution partnerships.

Natus, Integra, Medtronic — Established neurotechnology players with invasive ICP platforms and complementary non‑invasive adjuncts. Strengths: deep hospital penetration, purchasing relationships, and integrated critical care portfolios. Strategic implication: these incumbents can accelerate adoption by bundling or cross‑selling non‑invasive modalities; they are also natural acquirers.

Executives should approach 2026 as a year to close gaps and set scale‑up moves for 2027–2029. The following actions prioritize de‑risking and optionality:

Prioritize clinical validation with regulator‑aligned endpoints. Allocate budget to prospective studies that benchmark device accuracy against accepted standards and demonstrate incremental clinical utility (e.g., reduced invasive monitoring, improved triage, or shortened length of stay). Design trials to satisfy both regulators and payers.

Accelerate regulatory engagement. Early meetings with FDA and other authorities can clarify evidence expectations. Consider Breakthrough or equivalent pathways for truly novel telemetric or long‑term monitoring solutions; for others, focus on robust 510(k)/CE evidence packages.

Build a reimbursement dossier now. Real‑world evidence (RWE), health economics models, and pilot collaborations with health systems will shorten time‑to‑coverage. Demonstrate downstream cost offsets and clear clinical pathways for adoption.

Pursue interoperable multimodal strategies. Consensus bodies increasingly recommend multimodal non‑invasive assessment. Whether through partnership, OEM agreements, or software integration, offering multimodal capability will be a competitive differentiator.

Prepare for consolidation. Moderate concentration suggests mid‑market M&A activity is probable. Maintain a pipeline of potential targets—startups with differentiated sensors, analytics firms, or regional distribution assets—that can be integrated quickly into clinical channels.

Invest in explainable AI and robustness. Where ML is used to estimate ICP, prioritize transparency, bias testing, and clinical interpretability. These capabilities materially reduce regulatory and adoption friction.

Accuracy and clinical confidence risk — mitigation: fund large, multicenter validation studies and publish in high‑impact journals.

Reimbursement lag — mitigation: engage early with payers and develop value dossiers demonstrating cost offsets and care pathway improvements.

Incumbent competitive responses — mitigation: secure strategic partnerships with hospital systems and consider defensive M&A where appropriate.

Our report is built to be operationally useful to strategy, clinical affairs, regulatory and BD teams. It contains:

Market sizing and high‑granularity forecasts through 2032 with scenario analyses calibrated to adoption inflection points.

A regulatory and consensus map that translates standards and recent guidance into concrete evidence requirements for pathway selection.

A clinical evidence primer that ranks devices by validation maturity and identifies critical gaps sponsors must close to win clinician acceptance.

Commercial playbooks for go‑to‑market sequencing: direct hospital sales, distributor strategies, OEM tie‑ups, and managed service models for telemonitoring.

Reimbursement and health economics templates, including payor engagement scripts and pilot study designs to generate coverage decisions.

Competitive profiles and acquisition target screens assessing technological differentiation, regulatory status and claimed clinical performance.

Sensitivity analyses and investment case modeling to support capital allocation and M&A valuation discussions.

In 2026, leadership teams should stop treating non‑invasive ICP monitoring as an experimental adjunct and instead treat it as a strategic product class with clear commercialization pathways. The market growth trajectory supports meaningful investment, but success will favor organizations that can close evidence gaps, secure regulatory clarity, construct payer value propositions, and move rapidly to clinical scale through partnerships or acquisitions.

PW Consulting’s full market study contains the detailed segmentation, device‑level data, and execution templates required to translate these insights into boardroom decisions. We have intentionally withheld sensitive granular splits in this release to preserve the competitive advantage contained in the full analysis. For the complete dataset, scenario models and tailored advisory engagement options that will inform your 2026 commercialization roadmap, please consult the full PW Consulting report.

For detailed analysis of this topic, please visit the official page:Non Invasive Intracranial Pressure Monitoring Device Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com