you get reliable GitHub accounts that are stable

Health |

2026-05-29 22:45:24

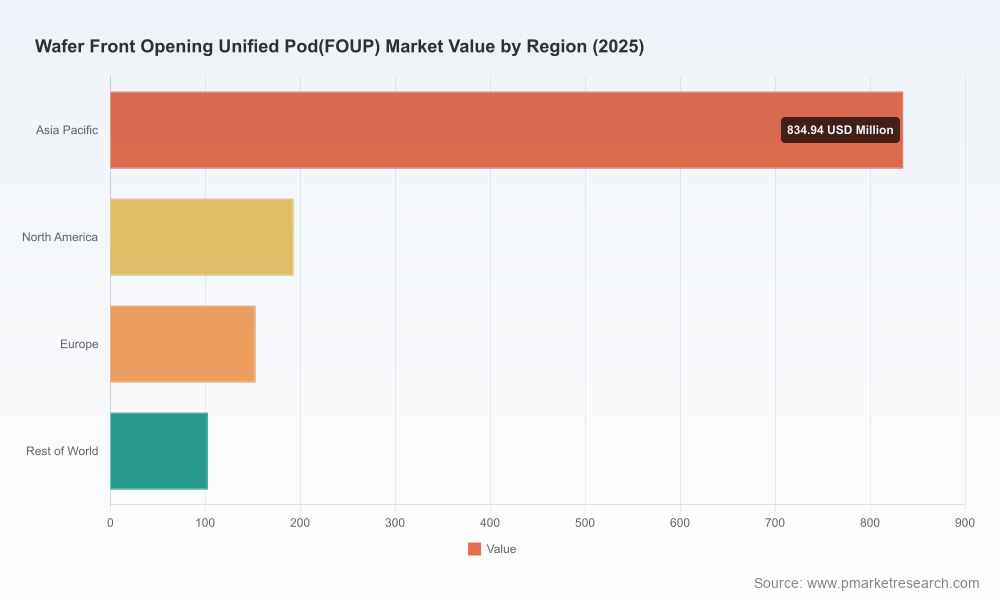

PW Consulting’s latest market study on the Wafer Front-Opening Unified Pod (FOUP) market provides a focused, decision-centric briefing for executives planning capital allocation, supply-chain strategy, and fab upgrades in 2026. Built on a 2020–2025 historical series and a 2026–2032 forecast horizon, the report quantifies the addressable market and projects a compound annual growth rate (CAGR) of 8.19% through 2032. The aggregate market expands from a mid‑single‑hundred million dollar base in 2020 to more than two billion USD by the end of the forecast window, with 2025 serving as the analytical base year for our models.

Wafer Front Opening Unified Podfoup Market

Procurement and capital timing: The FOUP market is at the intersection of fab automation refresh cycles, advanced-node transitions, and increasing adoption of non‑standard substrates (thinned, warped, 3D‑stacked). Understanding market trajectory and vendor capabilities is essential to time procurements to minimize obsolescence and maximize AMHS compatibility.

Wafer Front Opening Unified Podfoup Market

Risk management and supplier concentration: The market exhibits high concentration among leading suppliers, creating both negotiation leverage for large buyers and supply‑risk exposure for those with single‑source dependencies. Buyers that integrate supplier scorecards and scenario planning into sourcing decisions will materially reduce schedule and yield risk.

Wafer Front Opening Unified Podfoup Market

Technology and process alignment: As wafers evolve (EUV, advanced packaging, thinned wafers), FOUP design constraints—microenvironment control, purge options, interface standards—become binding design decisions for tool vendors, integrators, and fab owners alike.

Regulatory and standards compliance: SEMI standards remain the baseline for dimensional accuracy, automation interfaces, and cleanroom compatibility; compliance is non‑negotiable for full AMHS integration and cross‑vendor interoperability.

Market sizing and forward curves: A granular top‑down and bottom‑up market model covering 2020–2032, including sensitivity runs reflecting different fab spend and node‑migration scenarios.

Supplier scorecards and capability maps: Comparative assessments of product portfolios, microenvironment control, materials engineering, automation interfaces, and manufacturing footprint.

Total cost of ownership (TCO) and procurement playbooks: Lifecycle cost models, maintenance and cleanroom service templates, negotiated contract clauses, and a recommended sourcing process for single vs. multi‑supplier strategies.

Technical integration guides: Practical checklists to validate FOUP–AMHS compatibility, purge system integration, load‑port compliance, and test protocols for non‑standard substrates.

Scenario and stress testing: Supply‑shock simulations (raw‑material price spikes, capacity constraints), component lead‑time modelling, and contingency roadmap templates for fab planners.

Commercial benchmarking and M&A scouting: Valuation frameworks, target screening criteria, and integration playbooks for acquirers seeking strategic consolidation or capability buys.

The FOUP vendor landscape is shaped by a mix of global incumbents with deep materials and contamination‑control expertise, specialist suppliers focused on cost and dimensional accuracy, and regional manufacturers serving local fabs. Leading global players differentiate on microenvironment control, material science for contamination mitigation, automation compatibility, and support for non‑standard wafers.

Entegris (United States) — Differentiates with advanced microenvironment control systems and wafer isolation technologies designed to handle thin, thick, or warped substrates while maintaining automation compatibility. Their product focus shows the premium end of the market where contamination control and lifecycle service are prioritized.

Shin‑Etsu Polymer (Japan) — Known for precision molding and materials engineering, serving customers that require high dimensional accuracy at volume. Their manufacturing footprint and material know‑how support stable long‑run supply to major fabs.

Miraial (Japan) — Emphasizes strict SEMI compliance and material selection to deliver long‑term dimensional stability, a key selling point for fabs with stringent automation and yield requirements.

ePAK International (United States) — Offers modular eFOUP systems with multiple purge configurations and explicit AMHS compatibility; appeals to fabs seeking configurable rather than bespoke solutions.

Gudeng Precision (Taiwan) — Aggressively expanding product showcases and trade‑show presence with diffuser FOUPs and purge‑enabled solutions, signaling intensified competition in Asia for next‑gen handling products.

Regional players — A set of specialist manufacturers in South Korea, Taiwan, Japan, and Europe compete on cost, lead time, and localized service. The presence of credible regional suppliers constrains pricing power for global incumbents but also fragments the aftermarket services market.

Strategically, the market’s concentration metrics indicate that a small number of suppliers control a dominant share — buyers should therefore adopt dual approaches: consolidate long‑lead strategic buys with preferred partners while keeping tactical flexibility through qualified secondary suppliers.

Raw material volatility: Polycarbonate remains the dominant structural material for FOUPs. Recent regional price divergence has been observed—softening in Northeast Asia and tightening in parts of Europe—creating short‑term cost differentials that can materially affect unit economics and regional sourcing decisions.

Standards and compliance: SEMI standards (covering dimensional accuracy, automation interfaces and cleanroom compatibility) remain the operational baseline. Compliance audits and supplier qualification cycles should be factored into procurement lead times.

Substrate evolution: Continued adoption of thinned and 3D‑stacked wafers is driving iterative FOUP design changes to accommodate non‑planar and fragile substrates without compromising contamination control.

Automation uptake: Increasing AMHS penetration in fabs raises the bar on FOUP mechanical tolerances, purge systems, and interface standardization; incompatibility is a common root cause of integration delays.

Market concentration effects: Consolidation among top suppliers raises both strategic partnership opportunities and systemic supply risks. High concentration supports premium pricing for differentiated products but creates windows for targeted entrants where incumbents under‑serve niche needs.

0–6 months: Initiate a supplier qualification sprint focused on AMHS interoperability and SEMI compliance. Run a TCO scan across current installed base to identify near‑term replacement or retrofitting candidates. Lock in critical long‑lead components where supplier capacity is constrained.

6–18 months: Execute pilot programs for FOUP variants designed for thinned/3D wafers in representative process flows. Negotiate outcome‑based contracts (service SLAs tied to contamination and throughput metrics) with primary suppliers and establish contractual secondary sources for contingency.

18–36 months: Align capex cycles to the forecasted market growth window by scheduling major purchases to coincide with platform upgrades. Evaluate strategic M&A or joint‑development with targeted suppliers to secure differentiated features (advanced purge systems, integrated monitoring sensors) that will be required for next‑gen fabs.

Raw‑material shock: A sustained rise in polycarbonate prices in a major sourcing region would compress supplier margins and could lead to supply reshuffling; include material‑price escalation clauses in contracts and re‑price TCO models quarterly.

Standards change or enforcement tightening: Any retroactive enforcement of SEMI interface requirements can force costly retrofits; maintain active standards‑monitoring and supplier audit programs.

Supplier consolidation: M&A among key vendors can reduce choice and delay deliveries; preserve options through multi‑year framework agreements with service continuity clauses.

PW Consulting’s study blends quantitative forecasting with practitioner tools: templated procurement contracts, supplier scorecards, integration checklists, TCO models and risk‑adjusted scenarios. The deliverable is intentionally operational — designed for sourcing, operations, and corporate strategy teams to convert market intelligence into executable plans. To preserve the competitive value of the report’s detailed segmentation, vendor benchmarking matrices, and negotiated pricing simulations, this release summarizes the strategic implications while the full dataset and downloadable models are available through PW Consulting’s report portal.

For executives making capital allocation and sourcing decisions in 2026, this market study is a compact playbook: it frames where procurement leverage exists, identifies the vendor capabilities that matter for advanced‑node and non‑standard wafer programs, and delivers the tactical instruments — contracts, pilots, and scenario models — you can deploy immediately.

Access the complete report and interactive models on PW Consulting’s report page or contact our industry team to arrange a tailored briefing and data package customized to your fab‑level roadmap.

For detailed analysis of this topic, please visit the official page:Wafer Front Opening Unified Podfoup Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com