Synthetic Pesticide Inert Ingredients Market: Insights and Competitive Analysis

Other |

2026-04-08 08:44:24

PW Consulting’s latest market study on Distilled Gum Turpentine delivers a concise, decision-grade intelligence package for executives preparing strategic moves in 2026. The distilled gum turpentine market has demonstrated steady expansion through the first half of the decade — rising from a resilient base in 2020 to an estimated global market of USD 742.6 Million in 2025 — and is forecast to continue growing at a compound annual growth rate (CAGR) of 4.81% through our 2026–2032 horizon, reaching an expected market size above USD 1.03 billion by 2032. This briefing outlines the strategic value of our full report and highlights the operational and competitive dynamics corporate leaders must account for when setting priorities this year.

Distilled Gum Turpentine Market

Actionable horizon: 2026 marks a pivot year where procurement, product, and sustainability strategies converge with regulatory re‑assessment and feedstock volatility. Our report converts market forecasts into executable short‑term (12–18 months) and medium‑term (3–5 years) actions.

Distilled Gum Turpentine Market

Risk-to-opportunity translation: we quantify how upstream supply shocks and downstream formulation shifts translate into margin pressure or premium product windows (e.g., pharmaceutical‑grade or ultra‑high‑purity alpha‑pinene derivatives).

Distilled Gum Turpentine Market

Concentration and supplier dynamics: the market exhibits mid‑level concentration (top 3 players ≈ 38.5%; top 5 ≈ 52.4%), which creates asymmetric negotiation leverage and targeted M&A corridors—insight crucial for both buyers and investors.

Regulatory inflections: evolving regulatory frameworks in key jurisdictions are increasing compliance costs and labeling obligations; businesses that anticipate and operationalize compliance early will preserve market access and avoid costly reformulation cycles.

Executive synthesis: a tight, board‑ready briefing that maps market size trajectories, key scenario outcomes, and prioritized strategic recommendations for 2026.

Proprietary market model: demand and supply balancers across 2020–2032 with price sensitivity runs and elasticity testing to stress‑test procurement strategies and capital plans.

Supplier scorecards: comparative assessments of manufacturing footprint, quality credentials (including pharmaceutical rectification capability), sustainability practices, risk exposure and readiness for long‑term contracting.

End‑use insight matrix: differentiated demand dynamics across core applications, and the commercial levers each end‑market uses that affect turpentine pricing and required specifications.

Regulatory & compliance playbook: roadmap to manage REACH‑related requirements, U.S. labeling obligations, and export/regulatory permutations that affect product claims and packaging.

Procurement playbook: strategies for hedging, long‑term offtake, inventory policy optimization, and supplier co‑investment that preserve margins under raw‑material fluctuation scenarios.

M&A and partnership targets: screening criteria and a short list of strategic acquisition and JV archetypes tailored to secure feedstock, technical know‑how, or premium downstream differentiation.

CapEx & plant optimization guidance: incremental investments and process upgrades with quantified payback windows to reach pharmaceutical or ultra‑high‑purity grades.

Upstream feedstock volatility: tapering rosin processing and variations in tapping yields have driven episodic tightness in resin‑derived streams. These upstream movements materially influence distillation economics and margin compression for commodity turpentine sellers.

Price cycles and margin squeeze: recent years saw sharp year‑on‑year price surges in major origin markets, tightening margins for commodity processors while opening windows for premium‑grade suppliers. Firms without flexible pricing mechanisms or raw material hedges faced operational stress.

Product differentiation via purification: investments in advanced fractionation and rectification enable premium positioning (pharmaceutical and high‑purity alpha‑pinene). Recent capacity upgrades and product launches by industry players signal that premiumization is an active route to higher margin streams.

Regulatory pressure and labeling risks: EU substance registration and ongoing assessments, alongside U.S. labeling requirements for consumer‑facing products containing turpentine, create non‑negotiable compliance timelines that affect formulation, packaging and go‑to‑market plans.

Sustainability and source transparency: buyers increasingly require traceability for pine resin sourcing and management practices. Producers that can demonstrate responsible forest management and low environmental impact capture preferential procurement slots.

The market is a blend of long‑standing regional producers, specialized processors, and vertically integrated players. The competitive topography includes household names and nimble regional suppliers; this mix defines the tactical choices available to manufacturers, formulators and traders.

Legacy large producers: firms with long experience in steam or traditional distillation maintain reliable supply channels for standard grades. Their strengths lie in scale and established commercial relationships; however, they must invest to move up the value curve.

Specialist fractionators and bio‑chemicals players: companies investing in modern fractionation and high‑purity streams are capturing the premium end‑markets. These moves are accelerating the shift from commodity to specialty revenue pools.

Family‑run, on‑farm producers: smaller agribusinesses continue to serve niche customers with traceable supply chains and distinctive sustainability credentials, appealing to premium end‑users seeking verified origin stories.

Recent company actions to watch: select capacity upgrades and product launches announced over the past 18 months illustrate the dual trend of (a) capacity rebalancing to serve higher‑purity markets and (b) product portfolio expansion toward bio‑renewable intermediates. These strategic moves create new sources of supply but also increase competitive intensity for premium grades.

Secure hybrid supply: combine long‑term offtake with strategic spot purchases to capture upside from transient price spikes while ensuring continuity for formulations that cannot tolerate feedstock variability.

Prioritize quality‑upgrade options: evaluate upgrading or partnering for rectification/fractionation capability if your roadmap includes pharmaceutical‑grade or high‑purity intermediates; the incremental margin justifies capital or JV pathways in most scenarios.

Adopt adaptive contracting: incorporate indexation clauses and force majeure clarifications to manage raw material volatility and logistics disruptions without forfeiting commercial flexibility.

Embed regulatory foresight: allocate resources to track REACH and national labeling regimes; early compliance is a market access enabler and can be leveraged commercially.

Explore targeted M&A: mid‑sized suppliers with strong traceability, niche purification tech, or regional feedstock control represent high‑conviction opportunities for bolt‑on acquisition to secure supply and accelerate premium moves.

Operational de‑risking: implement a quantified risk register that links upstream weather, tapping yield variability and rosin processing rates to inventory and margin scenarios — and trigger pre‑defined mitigation actions.

Short‑term (0–12 months): prioritize supply assurance, contract renegotiation and regulatory compliance audits. Execute low‑cost hedges and conditional buy options for tactical price stabilization.

Medium‑term (12–36 months): validate CapEx for purification capabilities, pursue selective partnerships or asset acquisitions, and implement sustainability verification for premium placement.

Investment triggers: pursue M&A or greenfield only if projected IRR thresholds are met under multiple price scenarios and if the asset materially improves feedstock security or margin uplift via product premiumization.

Our full study translates the market’s macro trajectory and structural dynamics into executable playbooks: supplier negotiation scripts, capex prioritization, an investable M&A pipeline, and regulatory compliance calendars. The report’s proprietary demand/supply model and supplier scorecards enable firms to run company‑specific simulations and quantify P&L impact under three bespoke scenarios tailored to your business model.

Read the full PW Consulting Distilled Gum Turpentine Market report to access the proprietary datasets, segmentation analytics, and supplier mapping that underpin the executive recommendations summarized here.

Engage our advisory team for a tailored 90‑minute executive workshop where we overlay this market intelligence on your supply chain, commercial and M&A priorities and produce a short list of immediate actions for Q3–Q4 2026.

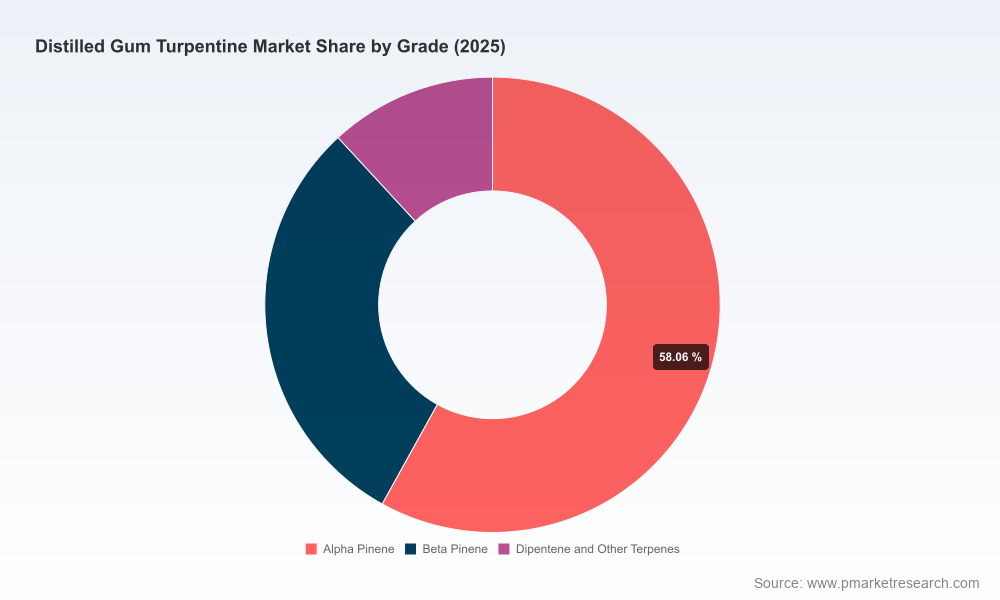

Note: this briefing highlights high‑level trends and practical recommendations while intentionally omitting detailed regional and application split figures to preserve the full report’s analytical value. The complete dataset, granular segmentation, and interactive modeling tools are available in the full PW Consulting publication and via our advisory engagement channels.

For detailed analysis of this topic, please visit the official page:Distilled Gum Turpentine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com