Transfer Glove Box Market: Strategic Imperatives for 2026 — A PW Consulting Preview

PW Consulting’s new market study on Transfer Glove Boxes establishes the evidence base senior executives need to make confident capital, R&D and commercial decisions in 2026. Built on a 2020–2025 historical baseline (base year: 2025) and a 2026–2032 forecast horizon, the study synthesizes regulatory, technological and financial drivers to produce an actionable roadmap for suppliers, OEMs, pharmaceutical manufacturers, and hospital systems. At the macro level the market demonstrates steady expansion with a compound annual growth rate (CAGR) of 6.15% through the forecast period — a profile that supports both sustained organic investment and selective inorganic moves.

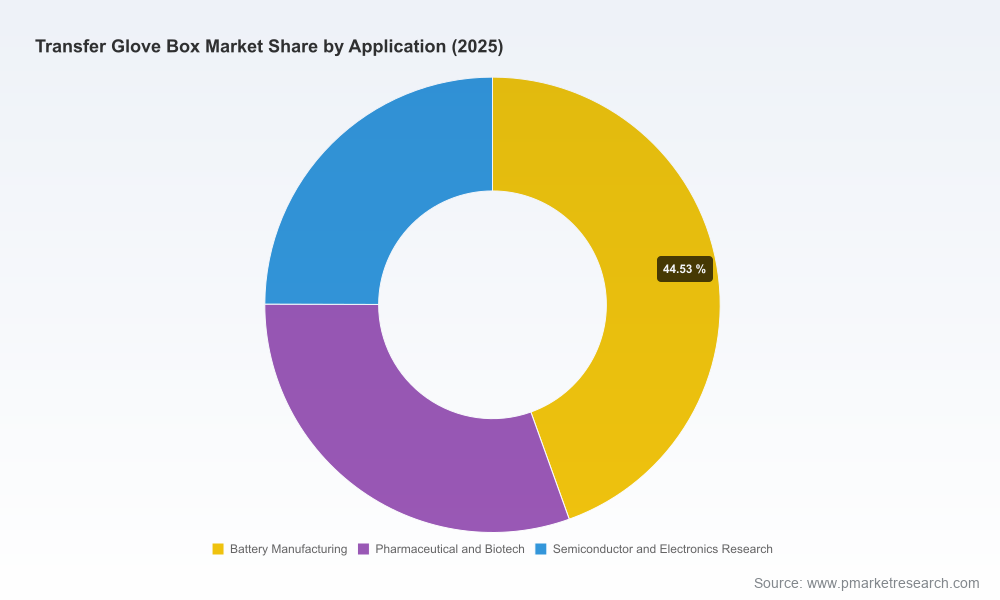

Transfer Glove Box Market

Why this preview matters to executive decision-makers

- Clarity under complexity: Transfer glove boxes intersect regulated aseptic processing, hazardous-material containment, advanced battery manufacturing and sensitive R&D workflows. Our study pares this complexity into decision-ready scenarios that link regulation, CapEx cycles and adoption barriers to revenue and margin implications.

- Timing for capital allocation: With hospital and institutional CapEx dynamics shifting, the report helps CFOs and strategy teams determine when to accelerate procurement, lease, or partner for turnkey solutions versus keep investment on hold.

- Competitive and M&A signal-setting: The analysis provides concentration metrics and competitor positioning that inform bolt-on M&A, technology licensing, and distribution partnerships without exposing confidential customer-level data.

Market overview — what the headline numbers tell us

Using USD (revenue unit: Million) and a base year of 2025, our longitudinal model captures the market trajectory from 2020 through 2025 and projects through 2032. After resilient recovery and growth in the early 2020s, the market enters a sustained growth phase driven by cross-sector demand for controlled transfer and containment solutions. The modeled 6.15% CAGR underpins a near-term environment where incremental product innovations, compliance-driven refresh cycles and capacity expansion investments will be the dominant revenue levers.

Transfer Glove Box Market

Two implications flow directly from the headline dynamics: first, suppliers should expect predictable, mid-single-digit top-line growth that enables multi-year product roadmaps; second, buyers should use the growth window to negotiate service-linked procurements and lifecycle contracts that protect operating margins as regulatory expectations tighten.

Transfer Glove Box Market

Key market drivers and dynamics

- Regulatory tightening and quality expectations: Updated and long-standing standards (for example, FDA guidance on sterile drug products and EU GMP Annex 1 requirements for ISO 5 critical zones) continue to push pharmaceutical and compounding customers toward isolator-based transfer solutions. Parallel updates to compounding and containment standards (e.g., USP <797>, USP <800>) are prompting procurement cycles among hospital pharmacies and specialty drug manufacturers.

- Capital intensity and warranty/service economics: Health-system capital expenditure pressures are visible — hospital CapEx metrics and aging facility backlogs are creating both urgency and procurement complexity for isolators and glove boxes. For vendors, this raises the strategic value of flexible financing, uptime-guarantees and field-service networks.

- Cross-industry adoption: Beyond pharma, battery manufacturing and semiconductor R&D are adopting transfer-enclosure technologies to control particulate, moisture and contamination risks. These adjacent applications create volume pools but also require differentiated product specifications and aftermarket approaches.

- Concentration and market structure: The market shows moderate concentration among established legacy suppliers and specialist engineering houses. This creates durable niches for differentiated materials (e.g., stainless steel, polymer modules) and integrated vacuum or transfer systems, while leaving room for new entrants with unique IP or service models.

Competitive landscape — who to watch

The competitive map combines globe-spanning industrial OEMs and specialist containment engineers. Core players include longstanding European engineering houses that specialize in stainless-steel isolators and transfer systems, as well as U.S. manufacturers focused on sterile compounding and biological containment. Several firms have recently refreshed their product portfolios with application-specific launches — for example, specialized containment units for radiopharmaceutical synthesis and aseptic isolators designed to meet the most recent Annex 1 expectations. These product moves underscore two trends: (1) manufacturers are racing to certify and demonstrate regulatory compliance as a market entry barrier, and (2) modularity and integration (e.g., transfer ports with downstream filling/lyophilization interfaces) are increasingly table stakes.

- Strategic positioning: Some vendors emphasize full-system isolator approaches that replace cleanroom footprints; others prioritize configurable modules for retrofits. Buyers should map supplier capabilities to their tolerance for facility disruption, validation timelines and lifecycle cost constraints.

- Recent product activity: The market has seen targeted launches for high-potency containment and radiopharmaceutical handling in the past 12–18 months, reinforcing a near-term surge in demand from niche, high-value applications.

- Consolidation opportunity: With a modest top-tier concentration and a fragmented mid-market, strategic M&A and distribution partnerships remain viable levers for rapid geographic expansion or capability acquisition.

What the PW Consulting report contains — practical, transaction-ready assets

This report is deliberately operational. It combines quantitative market projections with executable tools that procurement, R&D, and corporate development teams can use immediately:

- Validated market-sizing model (historical 2020–2025, forecast 2026–2032) with scenario toggles for regulatory shock, supply-chain volatility, and accelerated adoption.

- Competitive scorecards and technology mapping that compare materials, transfer mechanisms, containment certifications, and service footprints — enabling supplier shortlists matched to client-specific specs.

- CapEx and lifecycle TCO templates to run vendor-neutral “buy vs. lease vs. service” analyses over typical equipment lifecycles.

- Regulatory impact matrix linking Annex 1/USP/FDA expectations to product validation requirements, person-hours for qualification, and recommended documentation templates.

- Commercial playbooks for OEMs and distributors: go-to-market segmentation, prioritized account lists (by opportunity index, not disclosed in this preview), pricing levers and service-contract design.

- M&A diligence checklist focused on IP, validation history, spare-part availability and field-service KPIs that matter to acquirers.

Actionable recommendations for 2026

- For suppliers: Prioritize investments in validated, Annex 1-ready product lines and field-service capacity. Build modular platforms that reduce installation and validation time for customers with live production lines. Consider captive financing or outcome-based service contracts to lower customers’ procurement barriers.

- For pharmaceutical manufacturers and hospital systems: Use 2026 as a window to negotiate multi-year service-level agreements and bundled validation services. Where capital budgets are constrained, explore leasing and vendor-managed maintenance models to preserve working capital without accepting excessive lifecycle cost premiums.

- For corporate development teams: Focus on tuck-in targets that expand either regulatory-certification capabilities (e.g., isolator validation) or geographic service coverage. Mid-market consolidation remains an efficient route to scale without competing head-to-head on core engineering IP.

- For procurement and quality: Insist on supplier evidence for ISO 5/Annex 1 compliance and availability of protocol templates. Insist on spare-parts continuity and remote-support capabilities as part of the procurement evaluation.

How to use the full report (and why it matters)

This preview intentionally omits detailed regional and application-level splits and proprietary vendor scorecard ratings — those datasets and the underlying transaction-level assumptions are included only in the full report and dataset deliverable. For decision-makers preparing 2026 budgets, the full package provides the granular inputs needed for board-ready CapEx proposals, supplier negotiations and M&A term sheets.

PW Consulting’s methodology triangulates primary interviews with OEMs, end-users and service providers, validated public filings, and our proprietary adoption model. The deliverable includes an editable financial model so clients can substitute their own uptake assumptions and generate tailored forecasts and sensitivity analyses.

Next steps

- Download the full report and interactive model to access regional, segment and application breakdowns, vendor scorecards, and our recommended supplier shortlists.

- Contact PW Consulting for a tailored executive briefing and scenario-run workshop focused on your product roadmaps, procurement calendar and M&A priorities.

In an environment where regulatory expectations and cross-industry adoption create both opportunity and complexity, rigorous market intelligence is a force multiplier. PW Consulting’s Transfer Glove Box market study translates that intelligence into the practical tools executives need to act decisively in 2026.

For detailed analysis of this topic, please visit the official page:Transfer Glove Box Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com