Hard Facility Management System Market Size, Share, Trends, Growth Opportunities and Competitive Outlook

Other |

2026-06-02 14:21:12

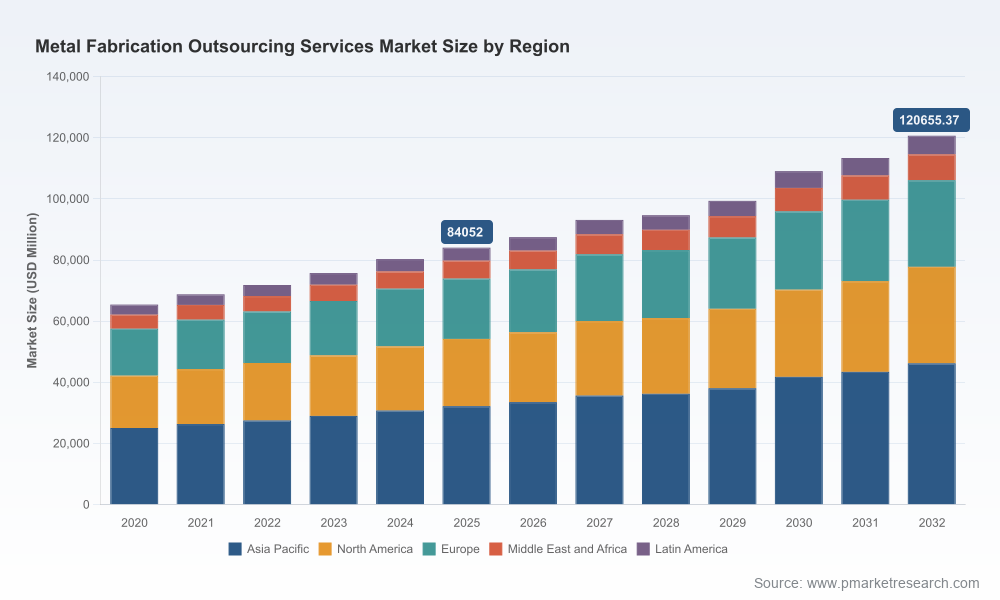

PW Consulting’s latest market study on Worldwide Metal Fabrication Outsourcing Services (base year 2025, forecast period 2026–2032) provides frontline intelligence designed to shape buying, sourcing, and capital-allocation decisions for manufacturing and industrial services leaders in 2026. With the global market growing at a steady compound annual growth rate (CAGR) of 5.29% from the base year and projected to expand meaningfully through 2032, our report synthesizes macro drivers, supplier-level competitive dynamics, cost and commodity pressures, and practical playbooks for near-term action. This release highlights the strategic value of the study without revealing the detailed segmentation tables and supplier scorecards reserved for subscribers.

Worldwide Metal Fabrication Outsourcing Services Market

Market momentum and investment timing: The market’s mid-single-digit CAGR signals predictable demand expansion but also rising capital intensity as fabricators invest in automation, digital workflows, and prefabrication assets. Procurement and operations leaders need to prioritize multi-year supplier roadmaps and capacity booking well before 2027 to avoid bottlenecks.

Worldwide Metal Fabrication Outsourcing Services Market

Continue reshoring and supply-chain diversification: Geopolitical shifts and tariff uncertainty are driving manufacturers to de-risk single-source strategies. The report frames decision trees for evaluating nearshoring versus offshore outsourcing under multiple geopolitical and cost scenarios.

Worldwide Metal Fabrication Outsourcing Services Market

Cost-structure sensitivity: Commodity and labor dynamics imply asymmetric cost exposures across suppliers and end markets. Our forward-looking scenarios quantify the impact of steel and ore price moves, and outline hedging and contract-design approaches to stabilize margins.

Technology-driven differentiation: Automation, digital quoting, and rapid-turn CNC/sheet-metal platforms are emerging as primary competitive levers. Buyers must align sourcing KPIs with supplier capability roadmaps rather than transactional unit pricing alone.

Market-sizing and scenario forecasts: A transparent build-up of the market from historical years through 2032, including a baseline forecast and sensitivity cases that reflect commodity, labor, and macro shocks.

Supplier capability matrix and playbooks: Operational scorecards that cover design-for-manufacturability (DFM), prototyping speed, automation intensity, quality systems, and logistics propositions—used to construct segmented sourcing strategies (strategic, tactical, spot).

Make-versus-buy decision frameworks: Cost models and decision trees that integrate total landed cost, risk-adjusted lead time, IP constraints, and capacity resilience for prioritized components.

Investment and M&A roadmaps: Prioritized capability targets for buyers and service providers—what to build, where to partner, and where to acquire—under three investment horizons (0–12 months, 12–36 months, 36+ months).

Procurement negotiation templates: Contract structures including indexation clauses for metal price volatility, automation performance SLAs, and flexible capacity arrangements suitable for 2026 procurement cycles.

Regional and end-market playbooks: Actionable guidance for positioning in high-growth segments and for adapting to region-specific regulatory, labor, and logistics realities (summarized, with full tables available in the report).

Commodity volatility and cost pass-through: Benchmark steel prices and related raw-material inputs remain a central concern. As of April 2026, industry benchmarks show continued upward pressure on some steel indices, while iron-ore and coking-coal projections suggest moderation into 2026. Procurement teams should expect mixed signals—opportunities for negotiated reductions where ore and coal ease, alongside continued spot volatility in finished steel—necessitating flexible contract mechanisms tied to transparent indices.

Labor scarcity accelerates automation: Persistent shortages of skilled welders and fabricators are pushing capital deployment into robotic welding, laser cutting automation, and digital inspection systems. Buyers should evaluate suppliers on not just installed automation but on workforce transition strategies and multi-skilled supervisory labor that ensures uptime.

Digital platforms and rapid manufacturing: On-demand digital marketplaces and rapid-turn platforms are changing expectations for prototyping and low-volume production. These platforms reduce time-to-first-part and reshape supplier selection criteria for design-intensive buyers.

Energy transition and regulatory drivers: Decarbonization goals are altering supplier investments and M&A patterns. Prefabrication and shop-floor efficiency that reduce on-site construction emissions are areas seeing disproportionate strategic investment.

Fragmented supplier landscape: The market remains widely fragmented with limited share concentration among the largest players—this creates both opportunity and complexity for buyers seeking scale, reliability, and innovation in a single partner.

Our analysis profiles incumbent industrial fabricators, integrated raw-material suppliers, OEMs with internal fabrication capabilities, and digital marketplaces. Below are distilled strategic positions of selected industry players that matter to procurement and corporate development teams.

Mayville Engineering Company, Inc. (MEC) — A U.S.-based specialist that has effectively pushed from heavy fabrication into light-gauge sheet metal and enclosure solutions through recent capability expansion. MEC’s acquisition-driven approach is a template for regional consolidation and fast capability stacking; buyers should watch its ecosystem play for enclosure and small-component supply chains.

O’Neal Manufacturing Services — Focused on heavy structural components and value-added assemblies, O’Neal’s strength is in vertical integration and scale for construction and mining equipment. Its proposition suits buyers prioritizing structural integrity and end-to-end supply continuity.

BTD Manufacturing Inc. — Niche precision sheet-metal and stamping expertise positions BTD favorably for agricultural and recreational vehicle segments where tolerances and repeatability are critical.

ThyssenKrupp AG and Liebherr Group — Large European engineering groups that combine global service footprints with deep forming and processing know-how. Their strengths are complex engineering, quality certification, and multi-industry exposure—suitable partners for high-specification and safety-critical components.

Nucor Corporation and Caterpillar Inc. — Represent two different vertical plays: Nucor leverages a steel-centric manufacturing network to offer integrated value on alloys and fabrications, while Caterpillar blends internal production with external outsourcing to optimize total cost and spare-parts strategies.

XCMG Group and ArtisanMetal — Major providers from China that deliver large-scale structural fabrications, often competing on capacity and lead time for heavy infrastructure projects. Their scale is attractive for large programs but requires careful evaluation of logistics, compliance, and IP safeguards.

Protolabs and Xometry — Digital-first providers serving rapid prototyping and on-demand manufacturing. Their platforms shorten product development cycles and lower first-article risk, making them strategic partners for product-engineering teams.

Prioritize supplier segmentation by strategic value, not just price. Allocate long-term commitments to partners that demonstrate roadmaps for automation and digitalization, and reserve flexible, spot capacity for platform-based rapid suppliers.

Embed commodity-indexed terms in new contracts and design strict trigger points for renegotiation. Use a combination of fixed-price windows, pass-through indices, and capped adjustments to balance risk between buyer and supplier.

Accelerate pilot investments in robotic welding and automated bending/press cells where skilled labor shortages threaten throughput. Structure vendor partnerships with co-investment clauses to share adoption risk.

Design supply-chain diversification plans with decision matrices that quantify lead-time trade-offs, logistics cost penalties, and geopolitical risk premiums. Nearshoring should be evaluated with real landed-cost models that incorporate carbon and regulatory costs.

Use M&A selectively to acquire capabilities (light-gauge rapid fabrication, digital quoting, automation specialists) rather than volume alone. Our M&A roadmap identifies capability gaps that unlock margin and service improvements within 18–36 months.

The study combines a robust market-sizing engine with tactical procurement templates and supplier scorecards that translate insight into executable plans. It is purpose-built to support: sourcing directors preparing 2026 RFQs, COOs planning capital deployment, and corporate-development teams evaluating bolt-on acquisitions. While this release outlines the directional intelligence and recommended actions, the complete report contains the granular segmentation, region- and application-level sizing, and vendor-level data needed to operationalize these recommendations.

To access the full dataset, supplier scorecards, and scenario models that underpin our 2026 playbooks, request the report via PW Consulting’s market research portal. Subscribers gain immediate access to downloadable models, negotiation templates, and an interactive scenario tool tailored to your company’s end-market exposure.

For detailed analysis of this topic, please visit the official page:Worldwide Metal Fabrication Outsourcing Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com