North America Space On-board Computing Platform Market Share Comparison

Fitness |

2026-06-11 12:46:03

PW Consulting’s latest market intelligence on the Worldwide Food Encapsulating Technology Market provides executives and strategy teams with a concise, decision-focused preview designed to inform investment, product, and supply-chain choices as companies set priorities for 2026. This briefing distills the study’s headline macro trajectory, competitive dynamics, regulatory and raw-material pressures, and the practical analytic assets contained in the full report — while reserving the granular segmentation tables and value-by-application breakdowns for clients who access the complete dataset.

Worldwide Food Encapsulating Technology Market

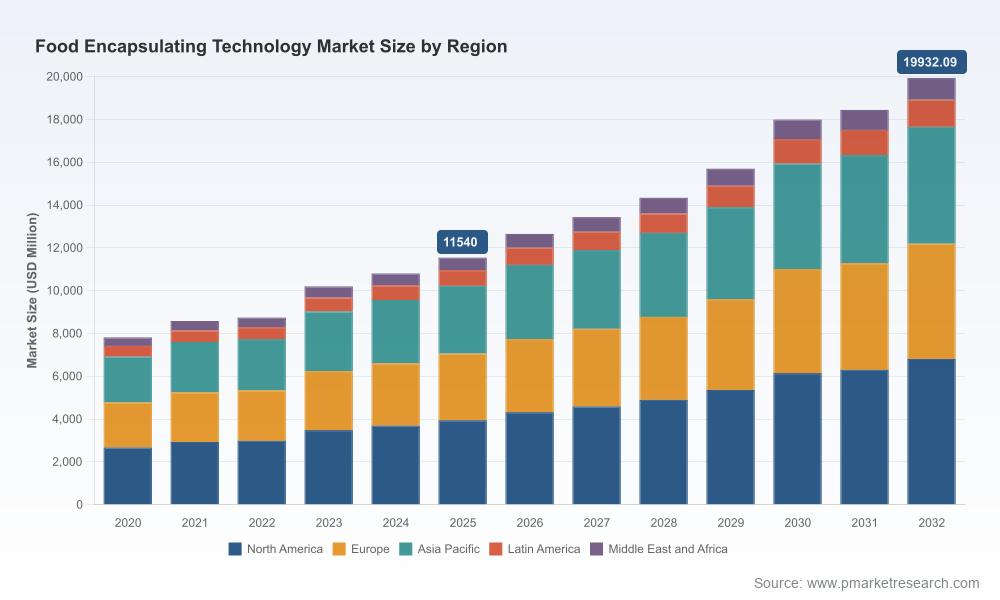

The market for food encapsulation has moved from niche ingredient science into mainstream commercial deployment. Our base-year analysis shows that the industry generated approximately USD 11.54 billion in 2025, rising from about USD 7.81 billion in 2020. Under conservative baseline assumptions, the market is forecast to expand to nearly USD 19.93 billion by 2032, reflecting an underlying compound annual growth rate (CAGR) of 8.12% over the 2026–2032 forecast period. That growth profile positions food encapsulation as one of the faster-growing segments within ingredient technologies, creating a meaningful opportunity window for manufacturers, co-packers, and ingredient formulators over the coming five to seven years.

Worldwide Food Encapsulating Technology Market

For executives planning capital allocation in 2026, two implications are immediate: (1) scale matters — both to capture volume-driven manufacturing economics and to meet demand for multi-ingredient, fortified formulations; (2) technology differentiation — choices around wall materials and release profiles will determine win rates with food manufacturers who are prioritizing stability, label claims and sensory fidelity.

Worldwide Food Encapsulating Technology Market

Market consolidation and scale: The market exhibits moderate concentration, with the top three and top five suppliers representing meaningful shares of industry revenue. This concentration dynamic raises both barriers and opportunities — incumbents can leverage existing customer relationships and scale; challengers must focus on technology specialization, niche end-markets or partnerships to gain traction.

Investment timing: Capital projects announced in 2024–2026 are likely to reach production in the late-2020s. Companies that commit to capacity now will be best placed to supply the mid-market innovation wave that follows early adopters’ commercialization cycles.

Regulatory and claims environment: Nutrient stability and controlled release technologies increasingly support compliance with labeling and fortification mandates. Firms that can demonstrate stability across shelf-life and processing conditions will secure longer-term contracts with consumer-food manufacturers.

Shift from protection to function: Early encapsulation use-cases focused on protecting sensitive actives during processing and storage. The next phase emphasizes purposeful functional delivery — enteric release, targeted sensory release, timed antioxidant delivery — enabling premium product claims and formulations.

Material innovation: Wall materials remain foundational to performance. Polysaccharides (starches, maltodextrins, gum Arabic) and proteins (whey, soy, pea) continue to predominate, but sustainable and plant-protein-based walls are maturing. Peer-reviewed validations published in 2025 illustrate that pea-protein microcapsules can achieve enteric-like protection for fat-soluble vitamins under simulated digestion — a capability of immediate interest to functional-food formulators.

Processing diversity: Spray drying remains a high-volume choice for cost-effective powder formation, while fluid-bed coating, spray chilling and extrusion address specific release and texture needs. Selecting the right processing pathway is increasingly a product-design decision rather than a commodity procurement issue.

Labeling and fortification mandates create demand for reliable encapsulation that preserves nutrient potency through manufacturing and shelf-life, reducing risk for brand owners and shortening validation timelines for new products.

Food-safety applications are expanding: encapsulation of bacteriocin-producing cultures and natural antimicrobials has moved from laboratory research toward pilot trials as a tool to enhance safety of high-risk foods under current regulatory frameworks.

Sustainability and clean-label pressure are pushing R&D toward identifiable, plant-derived wall materials and minimizing synthetic carriers, which in turn influences supplier selection and co-manufacturing agreements.

The competitive set combines large ingredient conglomerates, specialized encapsulation houses, and agile material innovators. Our report evaluates these firms across capability (wall-material science, release technologies), scale (production capacity and geographic reach), and go-to-market (co-development, B2B formulation support, and application labs). Highlights include:

Large ingredient and flavor groups with deep R&D and global supply footprints continue to dominate contract flow for major food manufacturers. These firms leverage carbohydrate science and premix expertise to offer broad portfolios suited to beverage, dairy and bakery formats.

Specialist technology players are differentiating via enteric-release systems, protein-based walls, and pilot-to-commercial scale services. Their agility allows them to serve emerging categories such as personalized nutrition and probiotic-enriched products.

Material suppliers and chemical conglomerates play a dual role — they supply wall materials and co-develop stability solutions for vitamins and carotenoids, combining formulation and regulatory expertise that shorten commercialization cycles.

Notable corporate moves that influence strategic positioning in 2026:

Facility expansion: In December 2025, a leading microencapsulation specialist announced the development of a new high-capacity manufacturing facility in New York state, scheduled to come online later in the decade. This kind of capacity investment is a signal to potential partners and competitors — scale will increase for companies that integrate such projects successfully into their supply chains.

Material validation: In May 2025, a plant-protein microcapsule developer published peer-reviewed data demonstrating protection of fat-soluble nutrients through processing and simulated digestion with enteric release. This validation accelerates commercial interest in plant-based wall systems for fortified beverages and shelf-stable snacks.

The full study is built for executive use. It combines high-resolution market sizing with scenario-based forecasts, competitive benchmarking, and actionable go-to-market frameworks. Key deliverables include:

A validated global market model spanning 2020–2032, with bottom-up drivers and scenario toggles to stress-test price, raw-material and regulation shocks.

Granular segmentation by region, technology, and core-phase ingredient – note that these tables and historic/forecast line items are included in the complete dataset.

Supplier scorecards that rate companies across R&D depth, manufacturing footprint, commercial support and regulatory track record — helping procurement and corporate development teams prioritize partners.

Case-driven playbooks for six go-to-market strategies: (1) capability-led M&A, (2) co-manufacturing partnerships, (3) licensing of proprietary wall formulations, (4) vertical integration for branded-ingredient suppliers, (5) application-focused joint-development with OEMs, and (6) sustainability-driven product repositioning.

Operational checklist for manufacturing scale-up, including recommended pilot runs, sensory validation protocols, and regulatory documentation necessary for cross-border product launches.

Corporate development: Use the market model to size acquisition targets and run quick synoptic valuations under alternative growth scenarios. Prioritize targets with complementary release technologies or unique wall-material IP that can be rapidly integrated into product lines.

R&D and product: Allocate prototyping budgets toward wall-material validation and simulated-digestion testing early in the 2026 product roadmap. Plant-based walls that show validated enteric protection merit priority where “clean label” and vegan claims are strategic.

Supply-chain and procurement: Model two- to three-year capacity commitments with high-capacity suppliers to lock favorable supply terms, while maintaining flexibility through qualified second-source arrangements.

Regulatory and quality assurance: Strengthen dossier requirements for nutrient stability and release testing to reduce market-entry risk and protect product claims across jurisdictions.

The report’s market sizing synthesizes supplier revenue data, public filings, trade interviews and proprietary primary research. Concentration metrics show a moderate level of market share captured by the largest suppliers — an important factor in negotiating commercial terms and assessing competitive exposure. Where public information is limited, our projections apply conservative adoption curves and technology-substitution dynamics validated by industry insiders.

Run a 90-day technical audit to identify which formulations in your portfolio would benefit most from encapsulation upgrades (stability, taste-masking, targeted release).

Engage with two distinct supplier archetypes — a large-scale producer and a technology-specialist — to compare tradeoffs in cost, flexibility and IP exposure.

Prioritize pilot projects that test plant-derived wall systems if your brand strategy emphasizes sustainability or vegan claims; prioritize enteric and simulated-digestion protocols for probiotic or fat-soluble vitamin products.

Allocate competitive intelligence resource to monitor announced capacity expansions and peer-reviewed validations that could change supplier economics or product capabilities.

PW Consulting’s full Worldwide Food Encapsulating Technology Market report delivers the granular tables, supplier scorecards, and downloadable market model required to convert these strategic implications into executable plans. This preview is intended as a directional briefing — clients seeking the complete segmentation, company-level revenues, and downloadable forecasting model can access the full report and supporting data portal for implementation-ready detail.

For detailed analysis of this topic, please visit the official page:Worldwide Food Encapsulating Technology Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com