Europe Construction Adhesive Market Overview: Key Drivers and Challenges

Other |

2026-06-24 03:27:57

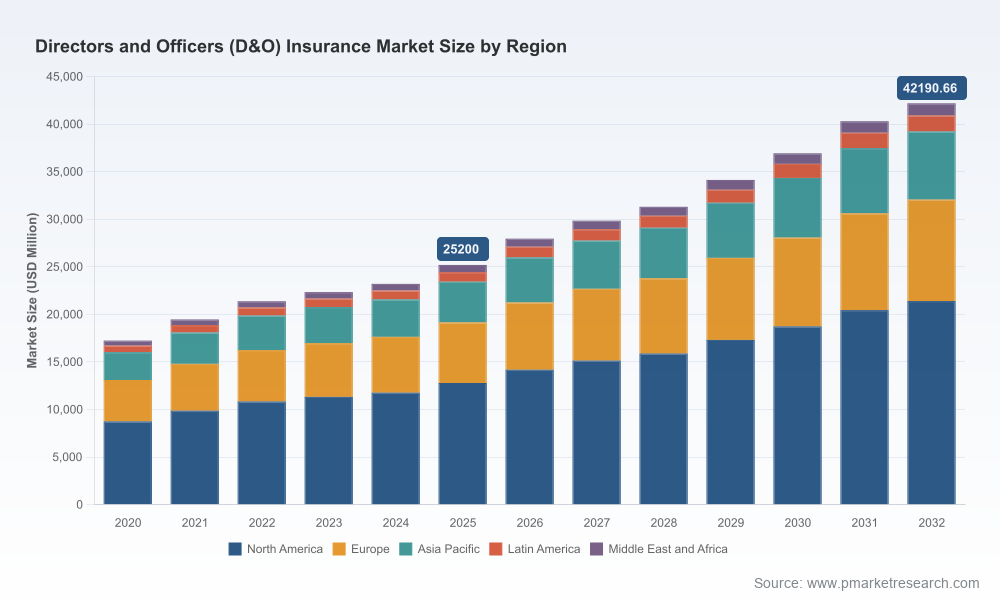

PW Consulting’s latest Directors and Officers (D&O) Insurance Market report is released at a moment of strategic inflection for corporate leadership and financial lines underwriters. The global D&O market reached approximately USD 25.2 billion in 2025 and, under our scenario-based forecasting, is projected to grow at a compound annual growth rate (CAGR) of 7.64% through the 2026–2032 horizon—driving the market toward the low‑to‑mid‑40 billion USD range by the end of the forecast period. For executives making 2026 budgets, risk-retention decisions, or partner-selection choices, this study distils the commercial, regulatory and litigation forces that will determine coverage availability, pricing dynamics and claims volatility over the next seven years.

Directors and Officers (D&O) Insurance Market

Actionable foresight for boards: The report maps how rising insolvencies, regulatory intensification and evolving oversight responsibilities (AI, ESG, cyber) translate into measurable D&O exposure scenarios. Boards can use these scenarios to stress-test governance, disclosure and litigation preparedness.

Directors and Officers (D&O) Insurance Market

Underwriting and pricing clarity: Amid a market that is stabilizing but still adjusting to claim-severity trends, our analysis offers insurers and brokers a framework for balancing rate adequacy against market share objectives—highlighting where discipline and accommodation will be required.

Directors and Officers (D&O) Insurance Market

Capital allocation and reinsurance planning: Insurers and reinsurers will find our forward‑looking loss-cost assumptions and concentration metrics essential when setting capital buffers and treaty structures for the 2026 renewal cycle.

Corporate purchaser playbook: For risk managers and CFOs, the report translates market trends into negotiation levers—coverage terms, retentions, and claims management protocols that materially affect total cost of risk.

Executive dashboards: Consolidated market sizing and trend indicators for quick boardroom briefings, including scenario outputs for stress cases and baseline growth paths through 2032.

Underwriting toolkits: A set of modular checklists and scorecards for evaluating corporate risk profiles (governance, litigation history, cyber posture, insolvency risk) designed for underwriting teams and broker panels.

Claims modelling and playbooks: Detailed loss-mode breakdowns, escalation protocols, and defence‑cost containment strategies—written for legal, claims, and risk transfer teams to integrate into incident response plans.

Scenario-based pricing sensitivities: Monte Carlo and deterministic scenarios that link macro shocks—economic contraction, sectoral insolvency spikes, regulatory enforcement surges—to premium and loss-ratio outcomes, enabling more defensible renewal strategies.

Competitive intelligence templates: A practical framework to evaluate carrier offerings, product features and service differentiation without exposing confidential segment-level metrics—enabling procurement teams to compare vendors on governance of coverage and speed of claims handling.

Regulatory and litigation heatmaps: Region- and sector-agnostic analysis identifying where regulatory scrutiny and securities litigation risk are concentrated, accompanied by recommended mitigation steps.

Several converging dynamics create a nuanced operating environment for D&O stakeholders in 2026. First, macroeconomic strain and a measured uptick in business insolvencies are creating a persistent tail-risk for directors—creditors’ claims, restructuring litigation and fiduciary disputes are on insurers’ radars. Concurrently, litigation severity has trended higher in recent years: median class-action settlements in securities matters rose materially, reinforcing the need for robust defence-cost management in policy design.

Second, the cost structure for claims has shifted. Legal-services inflation has been a notable driver—cumulative increases in defence costs since 2020 have materially eroded working-layer protections, forcing underwriters and insureds to rethink retentions and service strategies. Third, the regulatory and oversight remit for boards is expanding. AI governance, ESG disclosures and geopolitical risk management are transitioning from strategic priorities to potential sources of personal liability for directors.

Finally, market dynamics are being shaped by insurer behaviour and recent industry commentary. Several major market participants and industry watchers have signalled stabilization in pricing and stricter underwriting discipline. Independent market outlooks and insurer releases at the turn of 2025–2026 emphasize moderation in rate declines, vigilant claims management, and product innovation focused on emerging risk exposures—each of which influences renewal negotiations and product structuring in 2026.

The D&O insurance market continues to be influenced by a group of global insurers that combine multinational placement capabilities with specialized product offerings. Leading carriers—each with distinct strengths—are actively shaping product evolution and distribution practices. Our report profiles these firms to help purchasers and counterparties evaluate strategic fit:

Chubb — Multinational D&O solutions with emphasis on governance and securities claim defence; significant local presence in numerous jurisdictions supports complex placements.

AIG — Broad suite of D&O products catering to public, private and nonprofit entities; strong expertise in handling regulatory and shareholder disputes.

Travelers — Pragmatic coverage and claims handling for diverse organizational sizes, with operational emphasis on defence-cost management and settlement strategies.

Liberty Mutual / Ironshore — Focus on complex risk solutions and higher-limit placements for challenging exposures.

Allianz — Insight-driven offerings that integrate geopolitical and cyber risk perspectives into coverage design.

Zurich Insurance Group — Emphasis on multinational program capabilities that align with mid-market and multinational risk profiles.

AXA XL — Specialty enhancements for emerging risks within financial lines portfolios.

Beazley and Hiscox — Niche strength in cyber-exposed and SME segments, offering tailored management-liability products.

Berkshire Hathaway Specialty Insurance — Financially robust capacity for high-limit, complex D&O placements.

The report complements these profiles with recent market developments—firm and market-level announcements during late 2025 and early 2026—that provide signals on underwriting posture, price movements and risk appetite. Together they create a near-term view of how capacity and terms may evolve during the 2026 renewal season.

For boards and risk officers: Integrate scenario-driven D&O exposure assessments into your 2026 strategic planning cycle. Prioritise improvements in AI governance, ESG disclosure processes and insolvency contingency planning to reduce tail exposure and improve insurer reception at renewal.

For CFOs and procurement: Use structured carrier scorecards and consolidation options to extract service value, not just price. Focus negotiations on defence-cost control, crisis support services and clarity around exclusions as much as on headline premium.

For insurers and brokers: Recalibrate underwriting models to incorporate higher legal-cost inflation and shifting litigation severity. Develop product modularity that allows buyers to select governance‑support services alongside traditional capacity.

For reinsurers: Stress-test treaty terms against concentrated sectoral insolvency shocks and litigation escalation scenarios. Consider capacity-tiering strategies that preserve market access while protecting balance sheets from correlated litigation events.

Our approach combines quantitative market sizing and forecast modeling with qualitative, practitioner-led intelligence. The report synthesizes historical performance (2020–2025), our base-year assessment (2025), and robust scenario outputs for the 2026–2032 forecast window. It provides the templates, checklists and scenario mechanisms that allow boards, insurers and brokers to convert insight into operational change—whether that is tightening underwriting criteria, redesigning policy wordings, or reforming internal governance practices.

Importantly, the report is designed as a decision-ready resource rather than an academic compendium. It presents a concise set of leading indicators and operational playbooks that accelerate the path from analysis to implementation.

We have intentionally presented the strategic contours and actionable implications of the D&O market without disclosing the segmented, line-item intelligence that drives renewals and competitive positioning. The full report contains the granular modelling, carrier benchmarking templates and scenario outputs that procurement and underwriting teams need to operationalize these insights. For renewal committees, risk-transfer designers and capital allocators preparing for 2026, the full report is the reference toolkit that turns industry dynamics into defensible decisions.

Contact PW Consulting to schedule a tailored briefing where we will walk executive and underwriting teams through the scenarios most relevant to your sector and risk appetite, and demonstrate how to apply our underwriting checklists and claims playbooks to upcoming renewals.

For detailed analysis of this topic, please visit the official page:Directors and Officers (D&O) Insurance Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com