Why Are Digital Infrared Thermometers Remaining Important Beyond Clinical Settings?

Networking |

2026-06-09 12:35:45

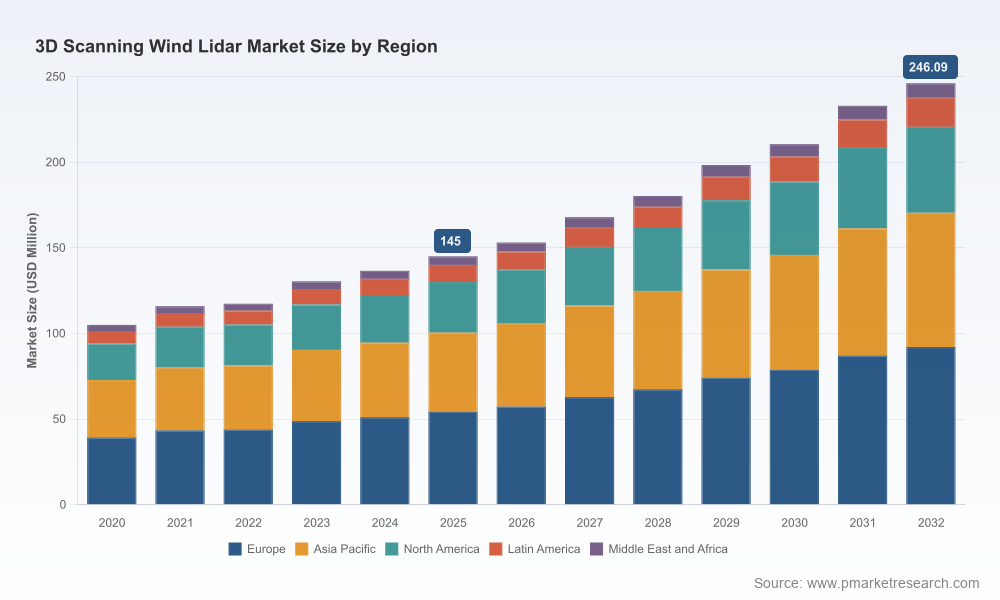

As wind energy projects scale in size, complexity and geographic reach, the instruments that measure, monitor and mitigate wind risk are becoming mission-critical assets. PW Consulting’s new Worldwide 3D Scanning Wind Lidar Market report (base year 2025; forecast 2026–2032) translates market dynamics into boardroom-ready decisions for 2026. The global market for 3D scanning wind lidars stood at approximately USD 145 million in 2025 and enters 2026 with continued momentum — our modelling points to a near‑term market above USD 150 million and a compounded annual growth rate of 7.85% through 2032, when market value is expected to more than approach USD 250 million. This briefing explains why those headline numbers matter, what competitive shifts to watch, and how procurement, R&D and M&A strategies should be adapted in 2026.

Worldwide 3D Scanning Wind Lidar Market

From resource assessment to operational optimization: 3D scanning lidar capability is rapidly moving from “nice-to-have” to “must-have” for large-scale wind projects, particularly where accurate three-dimensional wind-field mapping materially impacts energy yield estimates and turbine load mitigation strategies.

Worldwide 3D Scanning Wind Lidar Market

Regulatory and certification pressures: Independent IEC testing and classification are increasingly central to procurement and validation of lidar systems for project bankability and insurance—technical performance is a core part of commercial risk assessment.

Worldwide 3D Scanning Wind Lidar Market

Supply chain pinch points: Key optical components — notably eye-safe fiber lasers around 1550 nm and specialized photodetectors — are concentrated in a distinct supplier ecosystem. Sourcing risk and lead times for these components are critical inputs to capex planning.

Offshore acceleration: Growth in offshore wind translates into demand for scanning configurations and dual‑lidar deployments that provide 3D mapping across complex, turbulent marine environments—this drives higher-spec instrumentation and integration costs, but also opens premium service models.

Market sizing & forecast model (2020–2032), with scenario runs that stress-test deployment assumptions against variables such as offshore build rates, IEC certification adoption, and component lead times.

Commercial buyer’s toolkit: procurement specifications, IEC‑readiness checklist, testing protocols, and an RFP template that reflects the performance attributes buyers should insist upon in 2026.

Vendor evaluation framework: vendor scorecards and a reproducible vendor shortlisting methodology that combines performance, IEC test history, delivery risk and service coverage.

Supply chain and cost‑curve analysis: mapping of upstream suppliers (lasers, detectors, optics), sensitivity analysis on component pricing, and strategies to reduce BOM concentration risk.

Deployment playbooks: ground, nacelle and marine (buoy) operational considerations, including mounting best practices, data validation routines and maintenance cycles tailored to offshore vs onshore environments.

Investment and M&A scenarios: identification of capability gaps and target profiles for bolt-on acquisitions or strategic partnerships to accelerate sensor performance, geographic reach or software/data analytics capabilities.

Risk matrix and mitigation plans: commercial, regulatory and technology risks with prioritized mitigation actions tied to timeline and estimated spend.

The 3D scanning wind lidar vendor landscape is characterized by a mix of long-standing instrumentation specialists, vertically integrated defense/aviation electronics players, and nimble regional OEMs. Market concentration is moderate: our CR3 indicates a top-three concentration in the mid‑30s percentile range, and a top‑five concentration below 50% — enough to show leadership by a few firms, but with substantial room for competition and new entrants.

Vaisala (Vantaa, Finland) — A market leader in scanning lidar systems with product lines designed for both resource assessment and offshore campaigns. Vaisala’s emphasis on dual-scanning configurations is a strategic response to demand for redundant, high‑resolution 3D wind-field data.

ZX Lidars (United Kingdom) — Known for ground‑based scanning systems that target wind-energy projects. Recent product introductions emphasize IEC-compliant performance envelopes and deployment-readiness following independent testing.

Movelaser (Nanjing Movelaser Co., Ltd.) — A competitive regional supplier providing programmable scanning modes and cost-competitive systems; relevant for firms considering localized supply and faster delivery cycles.

Halo Photonics (Lumibird; UK/France) — Specializes in coherent pulsed Doppler systems, attractive for operators prioritizing high-sensitivity profiling and turbulence measurement across both onshore and nearshore sites.

ZATA (China) — Offers pulse-Doppler 3D scanning solutions with ambitions to scale across regional markets, especially where aggressive pricing and rapid deployment are decisive procurement criteria.

Leonardo (Italy) — With high-end Doppler lidar systems originally marketed for aviation, Leonardo’s technology is relevant for hazard detection and high-fidelity shear/gust characterization in wind farm safety cases.

Windar Photonics (Denmark) — Focused on nacelle‑mounted and scanning products optimized for integration with turbine controls and operational load reduction programs.

Notable recent developments underline how product performance and IEC classification are shaping vendor positioning. In September 2025, ZX Lidars launched an updated ground-based system that achieved IEC classification to greater measurement heights following independent testing. The same month, Vaisala announced a new lidar variant with enhanced performance characteristics for both wind energy and meteorological uses. These moves demonstrate how vendors are using validated performance and certification to differentiate in procurement processes.

Component concentration: Core subsystems such as eye‑safe fiber lasers around 1550 nm and matched photodetectors represent strategic supply nodes. Procurement teams should build supplier roadmaps and qualify secondary sources or consider contractual hedges to manage lead-time and price volatility.

Certification as a commercial filter: IEC independent testing is increasingly embedded in procurement specifications and financing covenants. Systems with documented IEC classifications command pricing premiums and lower market friction during project permitting and insurance underwriting.

Offshore as a demand multiplier: Offshore projects often require dual‑lidar configurations, extended range and ruggedized hardware — this elevates total installed cost but creates services and long‑term maintenance revenue streams for vendors and integrators.

Regional competition and localization: Cost-focused regional vendors are closing feature gaps, which puts pressure on incumbents to demonstrate value beyond price (e.g., data quality, service networks, analytics integrations).

Secure component resilience: Immediately map single-source exposure for 1550 nm lasers and photodetectors; qualify alternatives and consider strategic supplier agreements or small equity stakes for priority access.

Make IEC‑readiness mandatory in RFPs for bankable projects: Require IEC testing documentation and define acceptance criteria tied to financing and insurance milestones.

Pilot dual‑lidar deployments for offshore projects: Fund limited-scale trials that validate paired-sensor workflows and quantify yield/loads improvements — use pilots as a basis for operating-model changes rather than pure technology bets.

Embed lidar data into operational analytics: Treat lidar as a sensor within the digital twin — ensure interoperability, standardize data pipelines and budget for analytics integration to monetize improved forecasts and load mitigation strategies.

Pursue selective M&A or partnerships: Target small OEMs with complementary scanning modes or regional service footprints to accelerate market entry while managing integration risk.

Our full report is designed as a decision‑support package: the dataset and models can be used to stress-test procurement budgets, prioritize R&D allocations and quantify ROI for alternative lidar strategies. The report includes reproducible Excel models, vendor scorecards, procurement templates and a risk/mitigation roadmap calibrated for 2026 timelines. Note: detailed segmentation tables (regional, deployment mode, applications) and company-specific quantitative shares are reserved for the full report and data appendices.

The 3D scanning wind lidar market is at an inflection point where certification, component availability and offshore demand will determine winners and losers. With projected mid‑single‑digit to high‑single‑digit growth through the end of the decade, the time to act is now: secure supply chains, mandate IEC readiness, validate dual‑sensor concepts offshore and integrate lidar-derived insights into operational decision-making. PW Consulting’s Worldwide 3D Scanning Wind Lidar Market report turns market dynamics into executable 2026 strategies — the full dataset, vendor matrices and scenario tools are available in the report for teams preparing capex requests, vendor selections and M&A roadmaps.

To access the comprehensive datasets, vendor scorecards and executable procurement tools that underpin these conclusions, please visit the PW Consulting report page for the full Worldwide 3D Scanning Wind Lidar Market study.

For detailed analysis of this topic, please visit the official page:Worldwide 3D Scanning Wind Lidar Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com