Worldwide High-capacity NFC Chip Market: Strategic Imperatives for 2026 — PW Consulting Snapshot

Executive preview

The high-capacity NFC chip market is transitioning from a niche enabling technology to a core building block for secure identification, IoT onboarding, supply-chain provenance, and premium consumer interactions. PW Consulting’s new Worldwide High-capacity NFC Chip Market report (base year 2025, forecast 2026–2032) quantifies this transition and converts it into decision-ready intelligence for corporate leaders preparing procurement, product, and go-to-market strategies for 2026 and beyond.

Worldwide High-capacity NFC Chip Market

At the macro level, the market has expanded rapidly — from roughly USD 365 million in 2020 to an estimated USD 664 million in 2025 — and is projected to continue on a double‑digit trajectory. Our forecast shows the market growing to approximately USD 1.53 billion by 2032, reflecting a compound annual growth rate (CAGR) of 12.71% across the 2026–2032 period. Those headline figures capture a powerful mix of technology maturation, broadened application sets, and rising per-unit functionality requirements.

Worldwide High-capacity NFC Chip Market

Why this matters for 2026 decision-makers

- Procurement and supply continuity: Lead‑time extension and pricing pressures are real and measurable. Sourcing teams must move beyond single-year spot buys to multi-year agreements and strategic buffer policies.

- Product roadmaps and architecture choices: High-capacity NFC chips are no longer a commodity add-on. Choosing capacity, security feature sets, and interface options now materially affects user experience, certification timelines, and BOM costs.

- Security and compliance: Edge security capabilities — secure key storage, digital signature support, and multi-protocol cryptography — increasingly determine which vendors qualify for enterprise and regulated verticals.

- Commercial models: Emerging service and subscription models (device onboarding-as-a-service, lifecycle authentication) hinge on consistent NFC capabilities; product and commercial teams must align on minimum device specs.

What the report delivers — practical, operational intelligence

Our report is designed to be immediately actionable for executives, product managers, and procurement teams. Key deliverables include:

Worldwide High-capacity NFC Chip Market

- Market sizing and validated demand curves from 2020–2025, with forward-looking forecasts through 2032. These provide a quantitative foundation for capital allocation and program prioritization.

- Technology and use-case mapping that translates chip-level capabilities (memory, crypto engines, interface types, read performance) into implementation templates for ticketing, product authentication, secure onboarding, cold-chain telemetry, and premium consumer experiences.

- Vendor capability profiles and a practical supplier selection framework that balances performance, security certifications, supply resilience, and total cost of ownership over product life cycles.

- Procurement playbook: recommended contracting structures, inventory hedging strategies, and lead-time mitigation tactics tailored to NFC ICs with medium-to-high capacity requirements.

- Regulatory and trade-risk impact analysis with scenario planning that quantifies likely disruptions and prescribes mitigation levers for manufacturers with cross-border operations.

- Implementation checklists and reference architectures (hardware, firmware, and cloud integration) that shorten time-to-market and lower integration risk for teams building NFC-enabled products in 2026.

Competitive landscape — who matters and why

The high-capacity NFC IC space is dominated by a set of established semiconductor and systems players that combine IP depth, customer ecosystems, and manufacturing scale. Rather than presenting raw share tables, we synthesize competitive positioning and the strategic implications:

- NXP Semiconductors (Eindhoven): Strong in tag IC performance and RF optimization. Recent product introductions emphasize higher user-memory footprints and features that improve read reliability and tamper detection — capabilities that accelerate adoption in IoT labeling and secure asset tagging.

- STMicroelectronics (Plan‑les‑Ouates): Broad memory-density portfolio with recent moves into secure onboarding for smart‑home ecosystems. Their new product family targeting modern standards for device commissioning positions ST as a strategic partner for consumer device OEMs aiming to streamline out-of-box experiences.

- Infineon Technologies (Neubiberg): Combines secure-flash technology and multi-protocol support, making its devices suitable where payments-grade security or industrial robustness is required.

- Broadcom (Palo Alto): Focused on combination connectivity silicon (Bluetooth + NFC), appealing to handheld and portable devices that demand integrated connectivity with constrained power budgets.

- Samsung Semiconductor (Suwon): Delivers mobile-optimized NFC ICs with embedded crypto and multiple host interfaces, aligning with handset and wearable manufacturers.

- Sony (Tokyo): With FeliCa-compliant ICs, Sony remains a compelling choice in transit and payment ecosystems where that standard dominates.

Collectively, these firms offer differentiated value along read-speed, memory density, security primitives, and ecosystem integration. For buyers, the decision matrix is increasingly about aligning vendor strengths to the target vertical’s certification and lifetime support requirements, not just unit price.

Recent product and market developments shaping 2026

- High-performance tag ICs: Vendors are releasing devices with markedly larger user memories and advanced RF tuning features optimized for fast read rates and densified deployments. These changes reduce friction in dense transit environments and enable richer data payloads for authentication and maintenance records.

- Secure, battery-less commissioning: The move toward on‑chip digital signatures and secure key storage for tap‑to‑pair workflows is real — a trend that will simplify mass-market IoT onboarding and shift implementation risk from software stacks to silicon capabilities.

- Price and lead-time dynamics: Recent industry price adjustments and prolonged semiconductor lead times (notably for wafers and substrates) are impacting procurement economics. Expect higher average selling prices for advanced high-capacity variants and longer supplier lead times unless mitigated through contractual and design strategies.

- Regulatory friction and geo-risk: Trade restrictions and export controls affecting semiconductor flows introduce an operational dimension for companies with China-based manufacturing or supply dependencies. Risk-aware sourcing and multi-sourcing strategies should be implemented immediately.

Strategic imperatives for 2026 — what to do next

We recommend a three‑track approach for companies that want to convert market trends into advantage in 2026:

- Design for resilience: Embed modularity in product designs so that alternate NFC ICs with different form-factors or interface footprints can be qualified quickly. Where possible, adopt abstraction layers in firmware to decouple higher-level services from chip-specific drivers.

- Lock critical supply and capabilities: Transition from single-batch purchases to multi-year supply contracts for critical high-capacity parts. Negotiate performance and security SLAs in contracts, and build inventory buffers aligned with product launch timelines.

- Elevate security requirements: Specify minimum on-chip security capabilities (e.g., secure key storage, signature verification, anti-tamper features) as non-negotiable procurement criteria for any NFC chip used in authentication or payments paths.

- Operationalize vendor selection: Use a scorecard that weights supply continuity, ecosystem support (OS and stack integrations), certification histories, and TCO elements — not unit price alone.

- Plan for regulatory shock: Run scenario stress tests to quantify the financial and schedule impact of supply interruptions tied to export controls or localized manufacturing constraints; implement dual-sourcing and geographic diversification where feasible.

How PW Consulting’s report helps you act

This report is constructed as a playbook — combining quantitative forecasting with qualitative, practical tools that directly support procurement negotiations, product design decisions, and go-to-market planning. Clients receive:

- Actionable vendor shortlists mapped to vertical scenarios (transport, healthcare, consumer, industrial), with recommended fallback sourcing plans;

- Implementation-ready checklists for security, onboarding, and certification milestones that shorten procurement-to-deployment cycles;

- Scenario models that quantify the cost and timeline implications of lead-time extensions, price inflation, and trade-related disruptions so finance and operations can set realistic reserves and contingency budgets;

- Prioritized roadmap guidance for R&D and product teams to align silicon choices with emerging standards and ecosystem trends.

What we intentionally withhold here (and why)

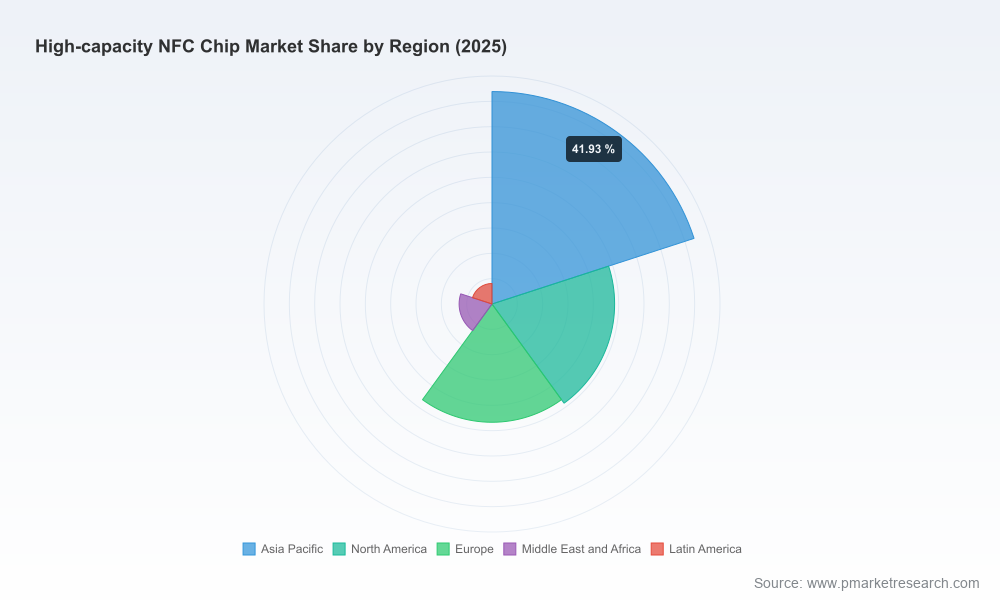

To preserve the strategic utility of the report for paying clients, we are providing a high-level synthesis in this release while withholding granular segmentation tables, detailed regional and application share breakdowns, and unit-price trajectories. These detailed datasets are essential for precise procurement modeling and competitive benchmarking; they are included in the full report and accompanying data appendix available through our website.

Final note — timing matters

Decisions taken in 2026 about supplier commitments, product architecture, and compliance posture will lock in costs and capabilities that affect P&L and customer experience through the end of this decade. With the market projected to more than double from 2025 levels by 2032 at a robust CAGR, companies that act early — aligning sourcing flexibility, security standards, and design modularity — will capture disproportionate upside.

For firms preparing business cases, negotiating supply agreements, or revising product roadmaps in 2026, PW Consulting’s Worldwide High-capacity NFC Chip Market report provides the data, the playbooks, and the vendor-grade analysis needed to navigate an accelerated, risk-prone market. Visit our report portal to access the full dataset, vendor scorecards, and downloadable implementation templates.

For detailed analysis of this topic, please visit the official page:Worldwide High-capacity NFC Chip Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com