Animation Market: Size, Share, and Future Growth

Other |

2026-05-18 06:47:38

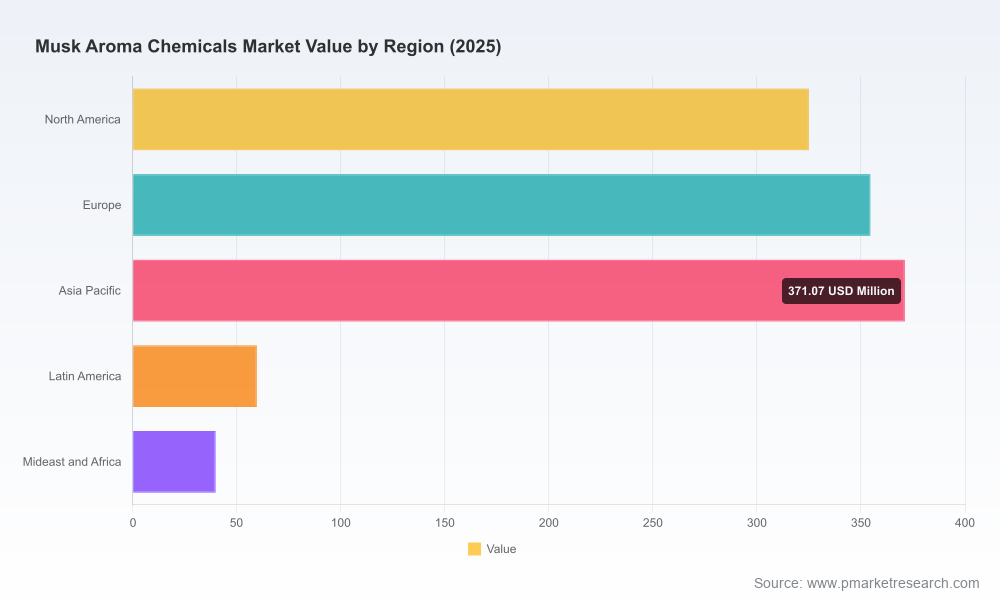

PW Consulting’s latest market research, “Worldwide Musk Aroma Chemicals Market,” delivers a forward-looking strategic blueprint for executives navigating the complex intersection of regulation, sustainability, and innovation in musk scent chemicals. Our analysis—rooted in a robust historical review (2020–2025) and a detailed forecast through 2032—shows the market evolving from a 2025 base of approximately USD 1,150 Million to an expected USD 1,539 Million by 2032, reflecting a compound annual growth rate (CAGR) of 4.25% over the 2026–2032 forecast period. This press release summarizes the report’s strategic value for 2026 corporate planning and highlights the practical tools leaders need to convert insight into action.

Worldwide Musk Aroma Chemicals Market

Several converging forces make 2026 a decision-heavy year for producers, brand formulators, and investors in musk aroma chemicals. Regulators are tightening permissible use levels for legacy compounds, major producers are accelerating capacity for next‑generation biodegradable musks, and synthetic chemistry continues to dominate supply due to cost and consistency advantages. For companies weighing capital allocation, reformulation programs, or M&A, the choices made in 2026 will materially affect competitive positioning for the remainder of the decade.

Worldwide Musk Aroma Chemicals Market

Historical context: The market has shown resilience across 2020–2025, with a recovery from pandemic-era disruptions and a steady migration toward higher‑value, regulatory‑compliant musk chemistries.

Worldwide Musk Aroma Chemicals Market

2026–2032 forecast: Our baseline scenario anticipates steady growth at a 4.25% CAGR, driven by demand in fine fragrances, personal care, and home care, alongside incremental gains from industrial and niche aroma applications.

Market structure: Concentration remains meaningful—our report documents a high level of market share among top suppliers (CR3 and CR5 metrics indicate significant aggregation), underscoring supplier influence over pricing, innovation diffusion, and contract terms.

Policy changes are not peripheral: they are central determinants of product portfolios and R&D prioritization. The IFRA 51st Amendment imposes lower usage ceilings for certain musk ingredients, with compliance timelines influencing product launches and reformulation pipelines. Concurrently, regional regulatory frameworks such as REACH continue to restrict legacy nitro musks and some polycyclic classes due to persistence and bioaccumulation concerns. The practical consequence for market entrants and incumbents is clear—invest in compliant chemistries or face forced substitution with limited lead‑time.

Synthetic dominance: Synthetic musks account for the preponderance of supply (our review indicates roughly an 85% share), favored for their cost profile, quality consistency, and adaptability to evolving regulations.

Biodegradable and macrocyclic innovation: Leading suppliers are deploying new manufacturing capacity and licensing modern macrocyclic and biodegradable platforms to capture reformulation demand. Case in point: a major player completed commissioning new facilities dedicated to biodegradable musk compounds in 2024—an explicit signal of where scale will be built.

Biotech and route diversification: Biocatalysis and fermentation‑derived intermediates are transitioning from pilot to early commercial stages. Expect partnerships between fragrance houses and specialty chemical firms to accelerate commercialization of these routes.

The market is populated by a mix of global fragrance houses, specialty chemistry firms, and regionally focused manufacturers. The top tier of suppliers combines integrated R&D pipelines, regulatory expertise, and scale manufacturing—traits that enable rapid response to reformulation demand and preferential terms with major brand customers.

Givaudan (Vernier, Switzerland): A global leader with a broad portfolio spanning synthetic and macrocyclic musks; positions itself on regulatory-compliant and biodegradable variants and leverages deep customer relationships to influence formulation roadmaps.

dsm‑firmenich (Switzerland): Focused on sustainable macrocyclic chemistries; recent capacity expansions include dedicated units for biodegradable musk ingredients, signaling a push to serve both legacy demand and new regulatory-driven opportunities.

Symrise AG (Holzminden, Germany): Emphasizes performance innovations and regulatory alignment, particularly for personal care and fine fragrance markets where functional performance and compliance are prerequisites.

International Flavors & Fragrances Inc. (IFF) (New York, USA): Leverages integrated supply chains and biotechnology to produce cost‑effective, high‑performance musk fixatives—a model that reduces exposure to traditional petrochemical feedstock volatility.

MANE, Takasago, PFW, LANXESS, SODA AROMATIC, Privi, Robertet and others: These firms contribute differentiated capabilities—proprietary syntheses, regional manufacturing advantages, specialty grades for niche fragrances, and nature‑identical or bio‑based alternatives.

Our report is structured to move executives from insight to execution. It includes:

A transparent market model covering historicals and scenario forecasts through 2032, with sensitivity testing for regulatory shocks and feedstock volatility.

Regulatory mapping and timelines that translate policy clauses into practical product and launch implications.

Supplier heatmaps and capability assessments that identify where scale, innovation, and regulatory expertise reside (we map existing and planned capacity without divulging proprietary contract data).

Technology watch and investment cases for macrocyclic, biodegradable, and biotechnological production routes, including runway estimates and break-even scenarios for greenfield plants versus tolling partnerships.

M&A and partnership playbooks aimed at buyers and acquirers seeking bolt‑on technologies, regional manufacturing footprint, or vertical integration into key intermediates.

Reformulation toolkits and LCA benchmarking templates that allow R&D and regulatory teams to quantify compliance costs and lifecycle benefits when replacing legacy musks.

Commercial strategies and contracting frameworks to mitigate supplier concentration risks highlighted by our CR3/CR5 analysis.

For executives framing priorities this calendar year, PW Consulting recommends a focused set of strategic moves to protect margin and market share while positioning for growth:

Accelerate product stewardship programs: Prioritize ingredients already aligned with IFRA/REACH trajectories and invest in faster reformulation cycles for at‑risk product lines.

Secure mid‑to‑long term supply through diversified contracting: Negotiate flexible offtake deals and consider tolling arrangements or regional dual‑sourcing to reduce exposure to capacity bottlenecks.

Invest selectively in biotechnology and macrocyclic capabilities: Evaluate partnerships or minority investments that provide access to biodegradable musk platforms without the full capex burden of greenfield builds.

Embed regulatory timelines into NPD gating criteria: Ensure product development, marketing claims, and commercialization calendars are stress‑tested against evolving IFRA deadlines.

Use concentration metrics to inform negotiation posture: With a materially concentrated supplier footprint, large buyers should leverage volume aggregation and multi-year contracts to secure preferential pricing and priority supply.

Map your current musk exposure by ingredient class and compliance risk.

Run a supplier dependency heatmap tied to contractual flexibility and geographic risk.

Commission an LCA and cost‑to‑reformulate study for top‑selling formulations.

Engage shortlist partners for biotech pilots or tolling arrangements to de‑risk scale-up timelines.

Prepare a 12–18 month launch contingency for any product lines impacted by IFRA or regulatory reclassifications.

PW Consulting’s “Worldwide Musk Aroma Chemicals Market” report provides the decision‑grade analysis that procurement chiefs, R&D heads, and corporate strategists need in 2026. It pairs quantitative forecasting with qualitative supplier intelligence and executable playbooks—while deliberately reserving the granular segmentation tables, company‑level revenue splits, and proprietary price curves for the full report. These restricted data layers are essential for bespoke scenario modeling and are available exclusively through the report portal.

For executives preparing capital plans, negotiating supplier contracts, or designing compliant product portfolios, the time to act is now. Visit our report page to access the complete dataset, vendor heatmaps, and the implementation toolkits that operationalize the insights summarized here.

For detailed analysis of this topic, please visit the official page:Worldwide Musk Aroma Chemicals Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com