Top 5 Growth Opportunities in the Nano Silica Market

Networking |

2026-03-31 10:58:07

PW Consulting’s new market intelligence brief on the Worldwide Smart Thermometer Patch Market synthesizes five years of historical performance (2020–2025) and offers a seven-year forecast window (2026–2032) designed for executives who must make high-stakes product, regulatory, commercial, and M&A decisions in 2026. The market demonstrated robust expansion from an estimated USD 495.2 Million in 2020 to USD 812.45 Million in 2025, and our modeling projects continued acceleration to approximately USD 1,629.12 Million by 2032 at a compound annual growth rate (CAGR) of 10.45% over the forecast period.

Worldwide Smart Thermometer Patch Market

This briefing highlights the strategic value of the full report: it combines rigorously sourced macro data, primary interviews with market participants, clinical standard assessments, and transaction-level competitive intelligence into a decision-grade playbook. To preserve the commercial value of the underlying datasets and drive informed engagement, this release demonstrates the report’s analytical depth while directing readers to the full study for granular segmentation, regional splits, and configurable financial models.

Worldwide Smart Thermometer Patch Market

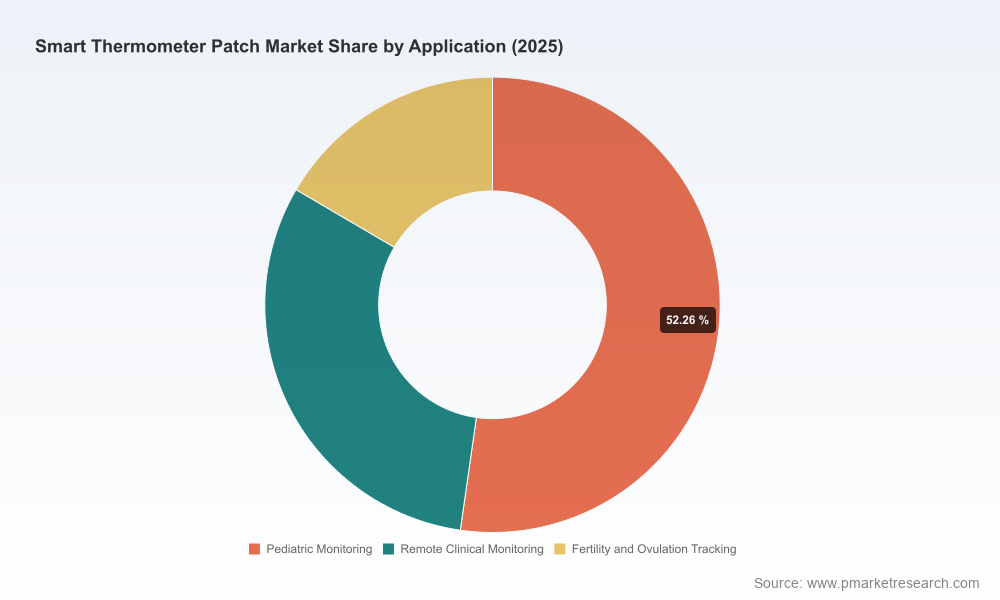

Convergence of clinical-grade sensing and consumer-friendly wearables is creating new care pathways: continuous axillary monitoring solutions are moving beyond hospital bedside use into home-based remote patient monitoring (RPM), pediatric fever management, and women’s health applications such as fertility tracking.

Worldwide Smart Thermometer Patch Market

Regulatory clarity and standards adoption (e.g., expectations under 21 CFR for Class II clinical thermometers and ASTM accuracy requirements) have reduced technical and market-entry uncertainty, accelerating adoption among payors and health systems.

The market’s growth trajectory—double-digit CAGR—creates windows for first-mover advantages in product-platform strategies, connectivity ecosystems, and services monetization (data analytics, RPM integrations, subscription models).

Our topline numbers tell a compelling story for 2026 planning: after near-term recovery and expansion through 2025, the market is set to sustain high-single to low-double digit growth through 2032. This trajectory is driven by three structural forces—technology maturity (sensor accuracy and battery life), regulatory acceptance (clearances and harmonized standards), and care model shifts toward decentralization of monitoring.

For corporate strategists, the implications are straightforward. Capital allocation should prioritize modular, software-enabled platforms that can be certified across jurisdictions; R&D roadmaps should sequence clinical validation for the highest-value use cases; and commercial teams should design channel strategies that balance institutional (hospital/RPM integrators) and consumer (direct-to-consumer, fertility/pediatric) routes to market. The full report contains time-phased scenarios that translate the headline CAGR into revenue and cash-flow implications under differing reimbursement, regulatory, and technology adoption assumptions.

Market sizing and forecasts (historical 2020–2025 and forecast 2026–2032) with bottom-up and top-down reconciliations and scenario sensitivity analyses suitable for board-level planning.

Go-to-market playbooks for institutional and consumer channels: pricing levers, bundle strategies (hardware + subscription), and partnership archetypes with RPM platforms and EMR integrators.

Regulatory and standards roadmap: an actionable checklist for 510(k)/MDR pathways, test protocols aligned to ASTM accuracy standards, and recommendations for clinical validation studies to maximize payer acceptance.

Product and IP benchmarking: feature gap matrices, BOM cost sensitivity, and suggested prioritization of sensor fidelity, power management, and secure connectivity.

M&A and venture diligence kits: target screening criteria, valuation comparables, and integration risk templates—particularly relevant given the market’s emerging consolidation dynamics.

Commercial diligence appendices: channel partner scorecards, buyer personas (health systems, pediatric practices, fertility clinics, direct consumers), and recommended KPI dashboards for pilots and scale-ups.

The market is led by a mixture of specialized medtech innovators and emerging regional suppliers. Competitive concentration data indicates an industry where the top three players control a meaningful share but where the top five capture just over half of market revenues, creating both oligopolistic pressure and opportunity for challengers through niche differentiation.

Blue Spark Technologies (Westlake, OH, USA) — Known for TempTraq, an FDA-cleared Class II disposable wireless patch designed for continuous axillary monitoring (up to 72 hours). Blue Spark’s strength is its regulatory-first approach and positioning for early fever detection in hospital and home-care settings.

VivaLNK Inc. (Campbell, CA, USA; operations in China) — Offers a reusable, rechargeable axillary patch with multi-week battery life and IoT integration. VivaLNK’s cross-border manufacturing and lifecycle model (reusable hardware + connectivity) make it a reference case for subscription and device-as-a-service models.

SteadySense GmbH (Austria) — Differentiates on clinical accuracy (NFC-enabled sensor with ±0.1°C claims), and regulatory quality (ISO 13485, MDR compliance). SteadySense is illustrative of the premium, clinically validated segment that targets hospital buyers and European health systems.

iWEECARE Co., Ltd. (Taipei, Taiwan) — Produces compact Bluetooth-enabled patches cleared by regulators for continuous axillary monitoring, with positioning across fever, fertility, and remote monitoring use cases—an example of multifunction product design.

Guangdong Genial Technology Co., Ltd. (Zhaoqing, China) — A recent entrant to the U.S. regulatory landscape, having obtained FDA 510(k) clearance in October 2024 for its T31 wearable digital thermometer. Genial exemplifies the new wave of Asian manufacturers moving into western markets through regulatory compliance.

Helyxon Healthcare Solutions Pvt Ltd (India) — Focused on pediatric and hospital segments with a continuous Bluetooth temperature monitoring system and real-time alerts, demonstrating how local market needs (cost and ease-of-use) shape product design.

Each of these companies reflects a strategic archetype: regulatory-centric incumbents, platform-oriented reusable-device players, precision clinical suppliers, multifunction consumer-device vendors, and cost-sensitive regional challengers. The full report includes vendor scorecards, go-to-market maps, and partnership matrices to support sourcing, alliance, or acquisition decisions.

United States: Smart thermometer patches are typically regulated as Class II clinical electronic thermometers under 21 CFR (product code FLL), requiring 510(k) clearance that demonstrates substantial equivalence. Companies should plan regulatory timelines and data packages early, as clearance is now a baseline expectation for institutional buyers.

Standards: ASTM E1112-type accuracy expectations (clinical thermometers targeting ±0.1°C or ±0.2°F) are de facto performance thresholds. Meeting these standards materially affects clinical adoption and payer conversations.

Europe and Other Jurisdictions: MDR conformity and ISO 13485 certification remain essential for market access and procurement tenders; early investment in quality systems reduces time-to-market and integration friction with health systems.

Based on our analysis, leadership teams should focus on the following priorities in 2026 to capture growth while managing risk:

Product-platform differentiation: prioritize sensor accuracy, battery strategy (single-use vs reusable), and secure interoperability capabilities that enable seamless integration with RPM platforms and electronic medical records.

Regulatory-first commercialization: bake 510(k)/MDR steps into product roadmaps; invest in robust clinical evidence packages that align with payer and procurement expectations.

Channel choreography: design dual-channel strategies that combine institutional pilots (hospitals, telehealth providers) with consumer-facing propositions (pediatric, fertility) to diversify revenue streams and accelerate unit economics.

Supply chain resilience: diversify manufacturing and component sources and validate quality systems across geographies to support rapid scale-up while protecting margins.

M&A and partnership clarity: use the market’s current concentration profile to justify either consolidation moves (to acquire scale and IP) or focused partnerships that accelerate clinical adoption and data-service monetization.

PW Consulting’s full Worldwide Smart Thermometer Patch Market report is structured to be immediately actionable for strategic planning cycles in 2026, including downloadable financial models, vendor diligence annexes, regulatory checklists, and implementation templates. Executive teams will find the report particularly useful for:

Translating macro growth projections into product-level revenue forecasts and R&D prioritization matrices.

Designing pilot programs and commercial contracts with clear KPIs and rollout timelines.

Preparing regulatory submissions and clinical evidence packages aligned to payer expectations.

To preserve investigative value for buyers, this briefing has shown the analytical approach, headline market trajectory (notably a projected CAGR of 10.45% and growth from approximately USD 812.45 Million in 2025 toward USD 1,629.12 Million by 2032), and competitive/regulatory dynamics. Detailed segmentation, region- and application-level splits, and the full company-level quantitative tables are available exclusively in the full report.

For boards, product leaders, and corporate development teams preparing 2026 strategic plans: request the full PW Consulting report to access the proprietary datasets, scenario models, and operational playbooks that translate market growth into executable initiatives. The full study is the companion you need to de-risk market entry, optimize product portfolios, and identify merger and partnership targets in a fast-moving industry.

For detailed analysis of this topic, please visit the official page:Worldwide Smart Thermometer Patch Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com