Single-Use Bioreactors for Vaccine Production Market: Size, Share, and Future Growth

Other |

2026-04-13 03:08:45

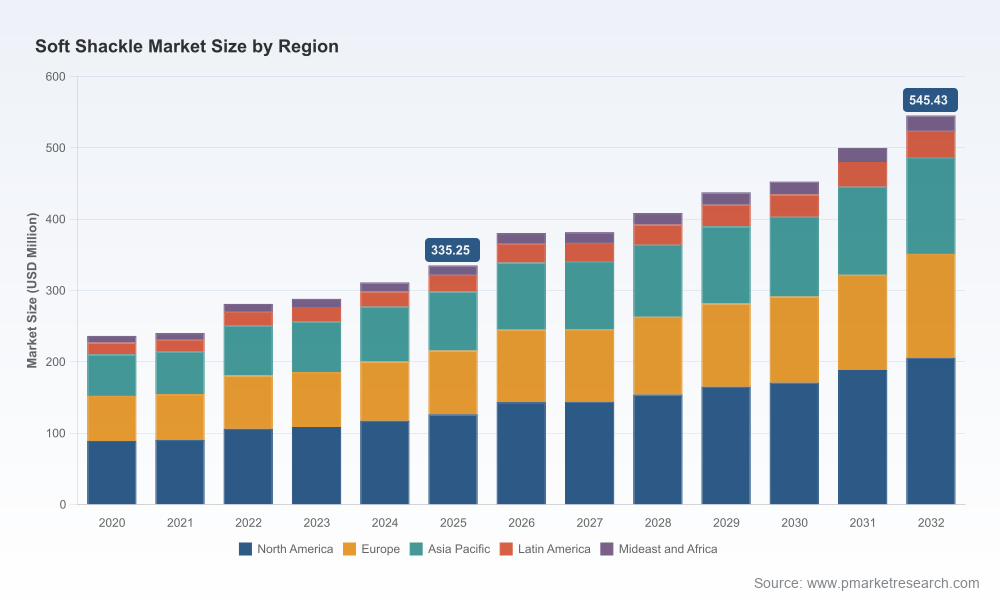

PW Consulting today publishes an executive market brief derived from our forthcoming full report, Worldwide Soft Shackle Market (base year 2025, forecast 2026–2032). The soft shackle category — lightweight, high-strength synthetic connectors primarily made from UHMWPE (Dyneema/Plasma) and related high-performance fibers — is transitioning from a niche alternative to steel into a mainstream industrial and recreational solution. Our modeling shows the market expanding steadily from an estimated USD 335.25 Million in 2025 to USD 380.64 Million in 2026, and projecting to reach USD 545.43 Million by 2032 at a 7.21% CAGR over the forecast horizon. For executives planning capital allocation, product roadmaps, or procurement strategies in 2026, these macro dynamics create actionable choices — and risks — that demand an informed response.

Worldwide Soft Shackle Market

Timing: 2026 is a pivotal year for firms to shift from proof-of-concept to scaled commercialization. Our forecasted 7.21% CAGR signals sustained demand growth that will reward first movers who solve production, certification, and end-user trust barriers.

Worldwide Soft Shackle Market

Capital allocation: Investors and corporate strategy teams must balance capex for in-house rope processing and finishing against outsourced, certified manufacturing relationships. The market scale and growth trajectory justify near-term investments in automated processing and traceability systems for many players.

Worldwide Soft Shackle Market

Regulatory and procurement windows: Military and institutional procurement windows are opening for compliant suppliers. Buyers who can demonstrate traceability, ISO-aligned quality systems, and adherence to requested safety factors gain preferential access to long-term contracts.

Market sizing and forecasts (2020–2025 historical series; 2026–2032 projection) with scenario analyses and sensitivity testing tied to raw material price and supply disruptions.

Demand-driver mapping across vehicle recovery, marine, industrial lifting, forestry, and other end uses — with quantified adoption curves and adoption triggers (safety certification, OEM endorsement, pricing thresholds).

Supply-side intelligence: factory capability benchmarking, quality systems (e.g., ISO 9001:2015), in-house rope processing, machine-stretching practices, and coating/cover technologies that materially affect durability and lift certification.

Competitive landscaping and playbooks — not just profiles, but acquisition targets, partnership archetypes, and platform bets for entrants and incumbents.

Commercial tools for procurement and product teams: supplier evaluation scorecards, TCO templates, minimum break-strength test protocols, and field-validation plans for OEM integration.

Risk and regulatory matrix — including military procurement considerations, safety factor policies for overhead lifting, and certification pathways that convert product acceptance into recurring revenue.

The soft shackle market remains fragmented with meaningful differentiation by technology, vertical focus, and certifications. Measured concentration is modest: the top three firms account for under one fifth of market revenue (CR3 ≈ 18.45%), and the top five near a quarter (CR5 ≈ 25.6%). This low concentration highlights two realities: the market is accessible to mid-sized specialists with tech or channel advantages, yet scale economies at the manufacturing and distribution levels are emerging as decisive competitive levers.

Our qualitative benchmarking of leading suppliers reveals distinct strategic archetypes:

Specialist off-road and recreational innovators (e.g., early entrants focused on vehicle recovery) who combine product lineage with brand equity in enthusiast channels. Their strength: rapid product iteration and community-driven testing. Their challenge: translating enthusiast credibility into institutional procurement.

Certification- and defense-grade manufacturers who emphasize traceability, serialized testing, and compliance with domestic sourcing rules. Their moat: access to defense and government programs that value Berry Amendment and Buy American Act alignment.

Industrial rigging and lifting companies that treat soft shackles as engineered alternatives to metal connectors, investing in fatigue and overhead-lift validation to capture higher-margin lifting/rigging contracts.

Marine-focused suppliers who position soft shackles as corrosion-free, lightweight replacements for metal hardware in demanding saltwater environments, often coupled with in-house rope manufacture and finishing to control quality.

Representative corporate behaviors from our company scans illustrate these archetypes. Some firms emphasize domestic manufacture, ISO-aligned facilities, and serialized factory testing to pursue institutional buyers. Others prioritize abrasion covers, Fiber Lock coatings, or proprietary rope formulations to serve off-road and marine enthusiasts where product feel and perceived safety matter more than formal certifications. These strategic choices shape margin profiles, channel strategies, and acquisition vectors.

UHMWPE fibers (commonly branded as Dyneema or Plasma) form the technical core of modern soft shackles, delivering strength-to-weight ratios that materially surpass steel while offering corrosion resistance and floatation. Suppliers that vertically integrate fiber procurement, on-site rope manufacturing, and machine-stretching capture both margin and quality control advantages. Conversely, firms reliant on third-party rope inputs face two pressing risks in 2026: raw material availability and the need for tighter supplier SLAs tied to batch traceability and minimum breaking strength variation.

Our recommended mitigations include: dual-sourcing high-tenacity fiber, developing supplier scorecards keyed to long-term tensile stability, and investing in standardized destructive testing protocols to validate batch-to-batch consistency. For players eyeing lift-and-rigging segments, investments in fatigue testing rigs and collaborative validation with end-users will accelerate adoption.

Regulatory context is a competitive accelerator. Certain products and facilities conform to military sourcing rules and ISO-quality systems, unlocking contracts with elevated lifetime value. Additionally, soft shackles are increasingly specified with engineering safety factors (commonly documented for overhead-lift requests as a 5:1 safety factor upon customer request). Firms that institutionalize laboratory and field testing — and can supply certified datasets — will find a widening gulf in procurement pipelines between certified and non-certified suppliers.

Prioritize certification and traceability if targeting institutional channels: obtain ISO-aligned processes, serialize units for test-traceability, and document factory load-testing protocols to meet defense and lifting-market requirements.

Invest selectively in vertical capabilities that unlock margin: machine-stretching and in-house rope finishing reduce variability and enable bespoke coatings/covers that address abrasion and UV exposure concerns.

Adopt differentiated GTM plays by vertical: recreational/off-road brands should double down on community-led field testing and influencer partnerships; industrial players should build engineered product families and engage with standards bodies to codify acceptance.

Design procurement playbooks for TCO over unit price: include lifecycle inspection protocols, replacement cadences, and failure-mode economics to shift conversations from upfront cost to operational risk mitigation.

Scan M&A and JV opportunities to stitch channel reach to production scale: with CR5 well below levels that indicate consolidation, 2026–2028 is a window for roll-up strategies that create distribution scale before commoditization pressures intensify.

Across marine, automotive recovery, industrial lifting, and utility uses, adoption is driven by three buyer priorities: demonstrable strength-to-weight improvements, repeatable testing/traceability, and clear maintenance/inspection protocols. Our field-validated buyer personas and spec-sheets in the full report translate these priorities into procurement checklists and contract clauses that reduce supplier risk and accelerate time-to-market for product-integrated OEM applications.

The soft shackle market in 2026 presents a classic opportunity window: clear technical superiority versus legacy metal hardware, an expanding addressable market illustrated by our modelling (rising from roughly USD 236 Million in 2020 to USD 335.25 Million in 2025 and projected to USD 545.43 Million by 2032 at a 7.21% CAGR), and a competitive landscape that still rewards differentiated quality, certification, and channel strategy. Executives who move decisively this year — investing in traceability, targeted certification, and route-to-market specialization — will capture the premium end of the market and shape industry standards that others will follow.

PW Consulting’s full Worldwide Soft Shackle Market report includes the detailed market models, supplier scorecards, product test-protocol templates, M&A targets, and a buyer’s negotiation playbook required to operationalize the insights summarized here. For access to the complete dataset, segmentation tables, and downloadable financial models, visit our report landing page or contact your PW Consulting representative.

For detailed analysis of this topic, please visit the official page:Worldwide Soft Shackle Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com