Asia-Pacific Alcoholic Beverages Market Growth and Future Trends 2025 –2032

Fitness |

2026-07-06 07:14:10

The HDH (hydrogenation–dehydrogenation) titanium powder market is entering a phase of accelerated maturation and strategic reconfiguration. After steady expansion through the early 2020s, the market reached approximately USD 524.5 Million in our base year (2025) and is forecast to grow at a compound annual growth rate (CAGR) of 7.2% through 2032, culminating in a materially larger market by the end of the forecast horizon. For corporate leaders and investors preparing plans for 2026, this report synthesizes demand drivers, supplier dynamics, regulatory constraints, and high-probability scenarios into a set of actionable strategic choices.

HDH Titanium Powder Market

Timing of capacity investments: A mid-single-digit to high-single-digit CAGR signals robust demand visibility for materials managers and investors. However, capital projects in titanium metallurgy are long lead-time and capital intensive; the window to secure feedstock contracts and manufacturing infrastructure is now.

HDH Titanium Powder Market

Supply-chain reshoring and security: Geopolitical posture and trade policy are translating into procurement mandates and procurement scrutiny. Organizations planning supplier diversification, hedging strategies, or vertical integration should align 2026 budgets with multi-year sourcing strategies.

HDH Titanium Powder Market

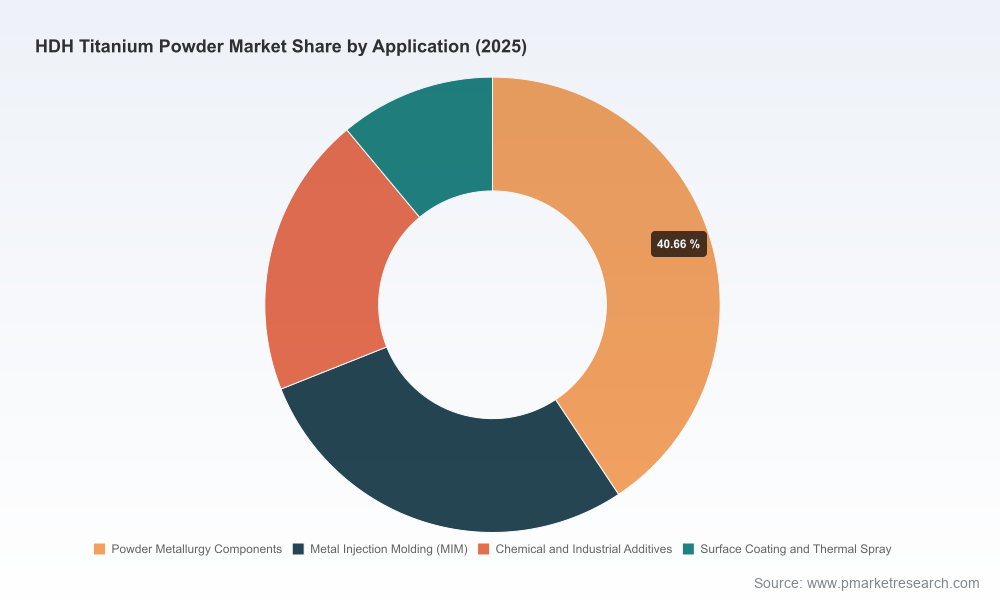

Product-portfolio optimization: HDH powder’s cost and particle morphology profile creates differentiated economics versus spherical atomized powders. Product and process engineers should evaluate HDH as a strategically advantaged input for powder metallurgy and thermal spray applications where spherical morphology is not essential.

Our analysis covers historical trends from 2020–2025 and provides a detailed forecast across 2026–2032. The market’s near-term trajectory is underpinned by industrial applications (powder metallurgy, MIM, thermal sprays), additive manufacturing adoption in select segments, and incremental penetration in high-value medical and aerospace niches where cost-performance trade-offs favor HDH forms. The reported USD 524.5 Million market in 2025 expands under a 7.2% CAGR to reach an estimated market size in excess of USD 850 Million by 2032, reflecting both volume growth and ongoing premiumization within specific purity and alloy classes.

Feedstock concentration and geopolitical risk: Titanium sponge capacity remains geographically concentrated, creating systemic exposure to export controls, tariffs, and other trade measures. Strategic sourcing plans for 2026 must therefore incorporate scenario-based safeguards — dual sourcing, contractual protective clauses, and nearshoring options where feasible.

Cost arbitrage and material substitution: HDH production, based on hydrogen-induced embrittlement followed by crushing and dehydrogenation, produces irregular/angular powders at lower unit cost than many gas-atomized spherical grades. Typical HDH pricing dynamics make it a competitive option for many powder metallurgy use cases; procurement teams should quantify lifecycle costs rather than unit price only.

Standards and qualification: Medical and aerospace adoption depends on compliance to strict specifications (including ISO and ASTM frameworks). Certification timelines and lot-release testing create multi-quarter lead times for qualification; investment in dedicated QA/QC capabilities and third-party validation should be focal points in 2026 plans.

Concentration and competitive positioning: Market concentration metrics indicate a moderately consolidated supplier base. The top three and top five suppliers command meaningful shares, which influences negotiation leverage, capacity availability, and M&A rationale. Buyers and investors must map supplier concentration to their risk appetite and contingency plans.

Our competitive analysis profiles global incumbents and regional specialists. Leading producers combine legacy metallurgy expertise with process control and customer-facing technical support. Notable strategic themes emerging across supplier strategies include integration to secure feedstock, product grade differentiation (purity and particle-size distribution), and long-term contractual anchors with key OEMs.

Major Japanese producers continue to emphasize high-purity HDH powders and are pursuing corporate realignments to strengthen integrated metal supply chains. Recent corporate integration activity among Japanese players underscores a trend toward consolidation and coordinated upstream-downstream strategies.

North American players are leveraging legacy relationships with aerospace and medical OEMs to secure long-duration off-take agreements and to justify incremental capacity and certification investments. Contract expansions with large OEMs provide signal value when evaluating supplier stability in 2026 procurement reviews.

Chinese manufacturers remain major volume suppliers with wide PSD and grade breadth. Their scale advantage informs freight-adjusted sourcing economics for global buyers, while export dependence and policy shifts create a separate set of strategic risks to be modeled.

European and specialized producers emphasize technical services, regulatory compliance, and niche alloy grades suitable for additive manufacturing and advanced surface treatments, often commanding premium pricing linked to qualification depth.

Strategic integrations and share-exchange transactions among established producers accelerate concentration and aim to lock in feedstock-to-powder value capture. Such moves lower the probability of isolated supply shocks for tied customers but may reduce buyer leverage in spot markets.

Renewed long-term offtake agreements between powder producers and aerospace OEMs de-risk revenue for suppliers and justify capacity upgrades. Buyers should anticipate that suppliers with long-term OEM contracts will prioritize those commitments when allocating constrained output.

Certification achievements among emerging producers expand the qualified-supplier pool over time, but OEM qualification cycles remain a gating factor for meaningful demand capture. Organizations seeking to onboard new suppliers in 2026 must budget for multi-stage validation and possible co-development programs.

The PW Consulting HDH Titanium Powder Market report is built for executives entering planning cycles in 2026. It combines macro forecasting with tactical tools and decision frameworks designed for immediate operationalization:

Demand-model workbook: A flexible demand model that allows users to stress-test assumptions (capacity constraints, adoption curves, and substitution scenarios) and to quantify 2026 procurement needs under multiple growth paths.

Supplier heatmap and qualification tracker: A concise, actionable heatmap that ranks suppliers against performance, certification status, geographic risk, and scale — enabling triage for new RFQs and second-source strategies.

Scenario playbooks: Three pragmatic scenarios (baseline growth, supply-constrained, and premiumization-led) that map recommended procurement, inventory, and contract strategies for each likely 18–36 month horizon.

CapEx and M&A checklist: A transactional framework for evaluating greenfield HDH capacity investments or strategic acquisitions, including due-diligence templates covering feedstock security, environmental permitting, and product qualification risk.

Regulatory & standards matrix: A distilled compliance roadmap for medical and aerospace applications that aligns product development milestones with ISO/ASTM qualification pathways and testing timelines.

Translate market growth into prioritized investments: Use layered decision gates — pilot buy, bilateral long-term contract, and co-investment in capacity — to move from tactical buying to strategic supply partnerships.

Operationalize resilience: Set explicit KPIs for feedstock diversification, on-hand inventory, and supplier redundancy. Model the cost of resilience against potential disruption scenarios; often a modest inventory or a secondary qualified supplier reduces enterprise risk materially at limited cost.

Accelerate qualification timelines: For buyers targeting medical or aerospace adoption of HDH powders, initiate supplier audits and joint qualification programs in 2026 to be production-ready for the next procurement cycle.

Evaluate vertical options: For integrated metal groups or OEMs with high titanium exposure, assess the total-cost economics of upstream integration versus strategic long-term contracting, accounting for feedstock control and margin capture.

Moderate market concentration — with leading firms commanding meaningful but not overwhelming shares — creates opportunities for regional consolidation, bolt-on acquisitions, and specialized greenfield projects. Investors should prioritize targets with certified product lines, stable OEM contracts, and demonstrable QA/traceability systems. Procurement teams should prefer suppliers who can demonstrate multi-year capacity plans and robust qualification evidence over those who compete solely on spot price.

In line with our “preview” approach, we have showcased the report’s analytical depth and strategic implications while intentionally withholding core segment-level tables and granular regional/application breakdowns from this press summary. The full report contains detailed segment forecasts, regional demand matrices, and price-sensitivity elasticities that are essential for transaction-level decisions. Access to these datasets and the interactive demand model is available on our report page and through tailored advisory engagements.

For executives preparing budgets, supplier strategies, or M&A playbooks for 2026, the next pragmatic step is a short scoping session to align our forecast scenarios with your internal demand projections and risk parameters. We then map recommended procurement and investment roadmaps tailored to your appetite for resilience, cost, and time to market.

To explore the full dataset, supplier heatmap, and scenario playbooks — including the precise segment-level forecasts and interactive modeling tools — please visit the PW Consulting HDH Titanium Powder Market report page or contact our industrial materials team for a briefing and advisory engagement.

For detailed analysis of this topic, please visit the official page:HDH Titanium Powder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com