Worldwide High Voltage System Market: Strategic Imperatives for 2026 — PW Consulting Preview

Executive snapshot

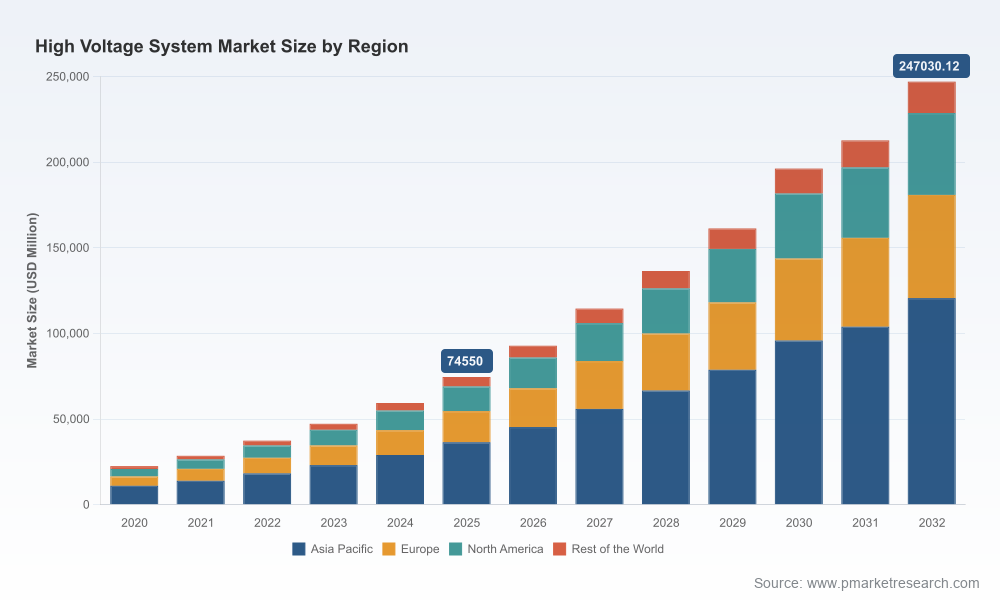

PW Consulting’s new market study on Worldwide High Voltage Systems provides a forward-looking framework that senior executives, capital allocators, and program directors will use to shape decisions in 2026. The industry is in a distinct acceleration phase: the global market expanded from USD 22,450.12 Million in 2020 to USD 74,550.0 Million in the base year 2025, and is forecast to grow at a compounded annual growth rate (CAGR) of 18.64% across our 2026–2032 projection window. By 2026 the market is expected to exceed USD 92,785.95 Million and, under central-case assumptions, reach approximately USD 247,030.12 Million by 2032.

Worldwide High Voltage System Market

Why this preview matters for 2026 decision-making

- Timing and scale are now strategic levers. Rapid market expansion and multi‑year project pipelines mean procurement and capacity decisions made in 2026 will determine technology adoption and margin capture for the next decade.

- Capital planning must internalize system-level supply chain constraints. Lead‑time inflation for large power transformers and other critical components has tightened project calendars and raised delivered equipment costs — industry data indicate significant price increases driven by raw material inflation and manufacturing bottlenecks.

- Regulatory and programmatic shifts are accelerating demand patterns. Select public funding and demonstration programs are lowering technical risk for next‑generation converters and facilitating multi‑GW interconnections, while regional permitting and corridor policies are changing project viability thresholds.

- Competitive positions are evolving from single-product OEM strength to system-integration and service-led playbooks. Companies that combine converter, cable, and digital asset-management capabilities are establishing differentiated contract terms and lifecycle revenues.

What the market numbers tell us (high-level)

The path from 2020 through our 2025 base year shows compounding scale and systemic investment: a roughly threefold increase in reported market size over five years signals both accelerated deployment of high voltage transmission assets and an expanding product scope (power electronics, cables, switchgear and digital substation layers). The 18.64% CAGR embedded in our forecast reflects sustained project announcements, increased offshore and long‑distance interconnections, and electrification-driven demand for higher‑voltage architectures. These macro facts define two immediate managerial priorities: secure project‑critical supply lines, and pivot design roadmaps to architectures that offer faster commissioning and higher lifecycle value.

Worldwide High Voltage System Market

Competitive landscape — who to watch and why

The market shows a moderate degree of concentration: the top three players command a substantive share of industry procurement, and the top five hold a majority share of reported revenues. This configuration creates room for both scale consolidation and targeted disruption by vertically integrated suppliers and specialized cable/connector manufacturers.

Worldwide High Voltage System Market

- Hitachi Energy (Zurich, Switzerland) — strong in HVDC Light (VSC) and classic HVDC solutions; recently investing in U.S. manufacturing capacity to meet rising grid modernization demand.

- Siemens Energy (Munich, Germany) — offers modular multilevel converter technologies and grid‑integration solutions tailored to offshore wind and multiterminal HVDC.

- GE Vernova (Cambridge, MA, USA) — significant installed base in LCC and VSC systems; active in large offshore cluster wins and refurbishment contracts for legacy HVDC links.

- Mitsubishi Electric and Toshiba (Japan) — longstanding capability in converter stations, transformers and system reliability for long‑distance links.

- Schneider Electric, Eaton — expertise in high voltage switchgear and digital substation integration that influences lifecycle O&M economics.

- Prysmian, Nexans, NKT, Sumitomo Electric — cable specialists whose turnkey subsea and land HVDC systems are decisive in offshore and interconnector projects.

- Regional system integrators and Chinese vendors such as TBEA and NR Electric — expanding presence on large interconnection and domestic modernization projects.

Recent contract flows underscore the point: consortium awards for multi‑GW offshore grid links, multi‑billion‑euro cable contracts, and targeted manufacturing investments by tier‑one suppliers are reshaping competitive intensity and capacity distribution across supplier types.

Selected recent developments shaping 2026 strategy

- Major offshore and interconnector awards are clustering in northern Europe and Asia, with several multi‑GW projects awarded to global consortia — signalling larger, more complex procurement cycles.

- Tier‑one manufacturers are expanding manufacturing footprints: large capital deployments to augment domestic transformer and power‑electronics capacity are being used as strategic responses to long lead times and national security of supply considerations.

- Policy and grant programs are de‑risking advanced HVDC R&D — selective government support for high‑performance, low‑cost converters accelerates commercial readiness of next‑generation architectures.

- Raw material pressure remains material to project economics: long‑lead components and steel/copper price dynamics have pushed delivered equipment costs higher and elevated the case for local sourcing and inventory strategies.

What our report delivers — practical outputs for 2026 action plans

The full PW Consulting report is designed as an operational playbook rather than an academic exercise. Key deliverables include:

- Scenario-based market sizing and TCO models calibrated to buyer profiles (utilities, IPPs, cable consortia), including sensitivity to raw material and lead‑time inputs.

- Procurement and contract templates that mitigate long-lead risk and align incentives across converters, cable suppliers and system integrators.

- Supplier scorecards and a negotiation-ready supplier short list by technology and project type (included as a gated dataset in the full report).

- Project delivery risk maps and a regulatory heatmap for fast assessments of corridor feasibility and permitting exposure.

- Commercialization roadmaps for 400–600V and higher‑voltage architectures, including recommended investment timelines for manufacturing and pilot projects.

- A rolling project pipeline tracker and M&A watchlist to identify near‑term acquisition or partnership targets that accelerate scale or capability.

Note: this preview intentionally omits the granular segmentation tables and node-level revenue shares that underpin our supplier shortlists and price-curve forecasts. Those datasets are available in the full report package on our site.

Strategic recommendations by stakeholder

- Utilities and system operators: accelerate early-stage procurement approvals in 2026 for critical converters and cables, and incorporate contract clauses that hedge raw material escalation and long-lead replacement costs.

- OEMs and integrators: prioritize modular, scalable converter architectures and invest selectively in regional assembly to capture margin and shorten delivery timelines.

- Cable manufacturers and suppliers: lock multi-year feedstock and manufacturing capacity contracts; pursue integrated project delivery models with civil and installation partners.

- Private capital and infrastructure investors: target platform plays that combine installation capability with long-term service contracts; look for tuck-in opportunities in digital asset-management and predictive maintenance.

- Policymakers and system planners: coordinate corridor policies and co‑location opportunities to reduce realization times and enable cost-effective route aggregation.

Methodology and confidence framing

PW Consulting’s study uses a transparent, multi-source methodology: historical market reconstruction covering 2020–2025 (base year), bottom-up project-tracking, vendor revenue modelling, and scenario-driven forecasting across 2026–2032. We overlay supplier contract awards, announced manufacturing investments, regulatory programs, and raw-material indices to stress-test our central case and alternative scenarios. The report also includes a confidence assessment for each forecasted segment and an audit trail to the primary sources and company disclosures used in our models.

Next steps — how to use this preview

This preview is purpose-built to help executive teams start planning for procurement, capacity investments, and M&A activity during 2026. For teams ready to operationalize these insights, the full report provides the granular segmentation, vendor scorecards, and downloadable financial models needed to build 18–36 month roadmaps and board-level investment proposals.

To access the complete Worldwide High Voltage System Market report — including the full dataset, proprietary supplier shortlists, and project-level pipeline tracker — visit our report page. PW Consulting’s advisory team is available to run custom briefings and scenario workshops to translate the findings into transaction-ready deliverables for your organization.

For detailed analysis of this topic, please visit the official page:Worldwide High Voltage System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com