Local Bank Integrates Digital Payment Gateway market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-05-21 12:44:34

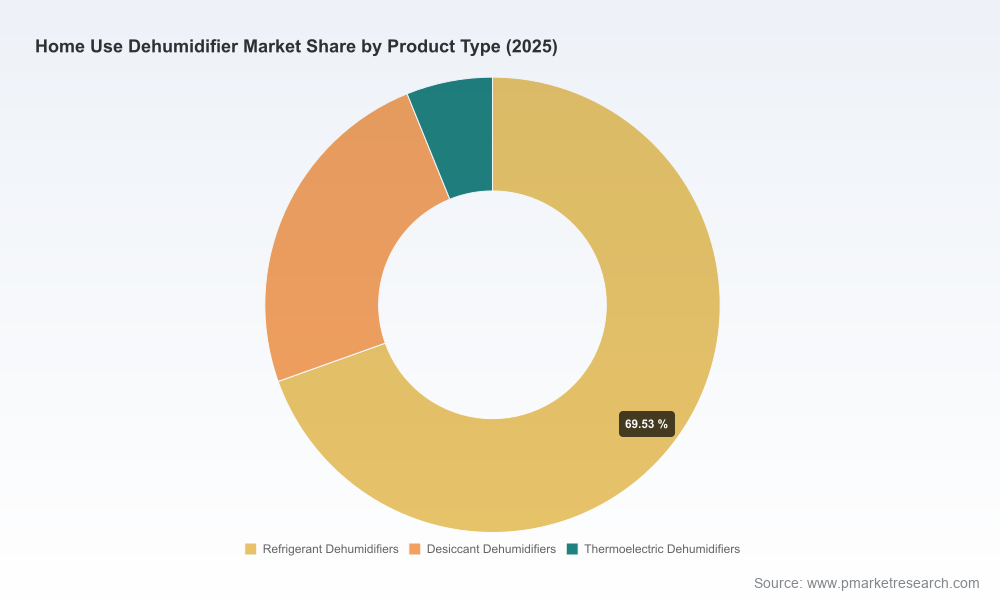

The global home use dehumidifier market is at an inflection point. After steady expansion through the early 2020s, the market reached USD 3,640.5 Million in 2025 and is forecast to sustain a mid-single‑digit trajectory — a 6.25% compound annual growth rate (CAGR) across the 2026–2032 forecast window — pushing toward roughly USD 5.57 Billion by 2032. Market concentration is moderate: the top three vendors account for just over 31% of sales, and the top five approach 47%, indicating a competitive landscape in which scale matters but specialist plays and channel advantages still unlock outsized returns.

Worldwide Home Use Dehumidifier Market

Actionable precision for product roadmaps: Our analysis translates macro trajectory into product-level priorities (efficiency, smart integration, and capacity mix) enabling manufacturers to align R&D budgets to the demand curve.

Worldwide Home Use Dehumidifier Market

Regulatory and standards navigation: The U.S. Department of Energy test procedures and the EPA ENERGY STAR Most Efficient 2025 criteria are shaping product acceptance and shelf‑eligibility. Understanding how these rules filter into design and cost targets is a 2026 must-have.

Worldwide Home Use Dehumidifier Market

Channel and service economics: The report provides go-to-market playbooks that quantify acquisition cost differentials between direct-to-consumer, big-box retail, and HVAC channel strategies — helping commercial leaders prioritize investments this fiscal year.

Risk mitigation in sourcing and recalls: Recent product safety recalls and legacy hazard issues underline the value of validated component sourcing, extended warranty economics, and recall contingency budgeting.

Energy efficiency is no longer optional. With ENERGY STAR updates and tighter DOE procedures, energy consumption and test-compliance are now gatekeepers to premium placement. Models that meet or exceed the Most Efficient criteria command distribution and consumer trust gains that materially affect sell-through.

Smart and integrated experiences drive margin expansion. Devices with reliable humidistat control, remote diagnostics, and integrations into home ecosystems (voice, HVAC controls, mobile apps) are rapidly moving from nice-to-have to expected features, enabling tiered pricing and subscription services for filter replacement, diagnostics, and performance guarantees.

Channel fragmentation creates white spaces. While heritage appliance retailers retain share, online marketplaces and specialty HVAC channels are expanding. Each channel has distinct SKU economics and post-sales liability profiles — an important consideration when forecasting 2026 inventory and service costs.

Durability and safety influence brand equity. Active recalls and historical fire‑hazard events have reshaped consumer risk tolerance. Brands that demonstrate transparent traceability, extended warranty options, and third-party safety certifications accelerate adoption among risk-averse buyer segments.

Midea Group (Foshan, China) — A dominant global producer of portable residential solutions, Midea’s Cube series demonstrates how modular product ranges, platformized electronics, and aggressive costs-to-serve can defend share in price-sensitive categories while enabling international expansion.

Haier Smart Home (GE Appliances) — Leveraging GE Appliances’ U.S. heritage and Haier’s global manufacturing scale, the company’s focus on reliable portable units with smart-home integration highlights a playbook of combining trusted after-sales with connected features to protect ASPs.

Electrolux (Frigidaire) — The Gallery and Frigidaire lines showcase the premium‑appliance approach: strong retail partnerships, product styling, and feature differentiation aimed at consumers who prioritize brand and in-home aesthetics as much as performance.

Honeywell, Whirlpool, LG, De’Longhi — These incumbents illustrate diversified strategies: from consumer electronics integration to channel-focused plays and lifestyle positioning. Their route to growth centers on incremental innovation, warranties, and cross-category bundling.

AprilAire, Santa Fe (Therma‑Stor) — Specialists in whole‑home and high‑capacity residential dehumidifiers underscore a segmented opportunity: premium performance for conditioned spaces and moisture-critical basements/crawlspaces, where value is demonstrated by engineering and serviceable product lifecycles.

Gree, Hisense, Danby — These players strengthen the value segment and OEM supply chain roles — important for buyers seeking volume at price, as well as brands that wish to outsource production while retaining design and market-facing functions.

Product launches at major industry events are accelerating adoption of inverter and variable-speed technologies, improving part-load efficiency and driving new performance benchmarks for residential units.

The EPA’s ENERGY STAR Most Efficient 2025 criteria creates a two-tier market where certified products gain disproportionate retail exposure and consumer preference; manufacturers missing the threshold risk SKU de‑listing in premium channels.

Regulatory and recall histories continue to influence procurement: ongoing fire-hazard recalls for certain legacy designs emphasize the strategic importance of robust compliance testing and serial-level traceability in supply chains.

Manufacturers — build a two-speed product portfolio. Preserve cost leadership in core portable SKUs while accelerating development of high-efficiency, connected units that target certification and premium channels. Prioritize design-for-service to reduce field failures and recall exposures.

Retailers and distributors — segment channel strategies. Use differentiated assortments by channel: value, mid-tier, and certified‑efficient premium. Invest in-store demo units and online performance calculators to reduce returns and increase conversion rates.

Investors and M&A teams — focus on platform value. Acquisition targets with proprietary smart HVAC integration, validated efficiency performance, or established whole-home distribution frameworks offer the fastest path to accretive growth in a moderately concentrated market.

After-sales and services — monetize the install-to-maintain lifecycle. Subscription-based filter delivery, remote diagnostics, and limited-performance guarantees extend revenue lifecycles and deepen customer lifetime value while mitigating reputational risk from safety incidents.

Supply chain leaders — de‑risk strategically, not broadly. Prioritize dual-sourcing for critical components (compressors, control boards) and create traceability systems to expedite recalls or targeted service campaigns without disrupting broader operations.

Verified market sizing and outlook tables covering historical (2020–2025) and forecast (2026–2032) performance with scenario planning that reflects energy regulation and innovation adoption curves.

Detailed segmentation by product architecture, capacity tiers, and channel economics — with pricing bands, unit economics, and ASP trend analysis to inform SKU rationalization.

Competitive positioning maps and vendor profiles that include strength/weakness diagnostics, innovation roadmaps, and M&A appetites for the leading suppliers.

Regulatory impact modeling for DOE procedures and ENERGY STAR criteria, and a compliance playbook quantifying development timelines and incremental BOM costs needed to meet thresholds.

Go‑to‑market blueprints for manufacturers and retailers, including pilot templates for direct-to-consumer trials, logistics and warranty models, and KPIs to measure profitability per channel.

Operational checklists for manufacturing resilience, quality assurance protocols to mitigate recall risk, and a supplier due-diligence framework that reduces time-to-service when hazards emerge.

We translate strategic intent into executable initiatives: prioritized product development sprints tied to certification milestones, SKU rationalization paths with modeled P&L impacts, and channel investment roadmaps keyed to 12–18 month retailer buying cycles. For leadership teams deciding 2026 capital allocation, this turns abstract growth percentages into concrete spend, staffing, and partner actions that move share and margin in the next two fiscal years.

This overview highlights the strategic vectors that will matter most in 2026. To preserve competitive integrity for our subscribers, we have intentionally withheld the granular regional and application-level splits and raw tables in this press summary. The full Worldwide Home Use Dehumidifier Market report contains the detailed breakdowns, downloadable datasets, and model access you need to set budgets, prioritize launches, and evaluate acquisition targets with confidence.

For direct access to the report, tailored briefings, or to commission a custom scenario run centered on your product portfolio, contact PW Consulting through our report page. Our analysts are prepared to run bespoke sensitivity analyses keyed to your geographic footprint, channel deployment, and product development timelines.

For detailed analysis of this topic, please visit the official page:Worldwide Home Use Dehumidifier Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com