Corteiz: The Streetwear Brand Redefining Modern Fashion

Fitness |

2026-06-29 05:44:06

PW Consulting’s latest market study on the Worldwide Maskless Lithography Machine market is released as businesses re-evaluate capital plans, supply chains, and product roadmaps for 2026. Anchored on a rigorous base year of 2025 (with historical coverage from 2020–2025 and forecasting through 2026–2032), the report synthesizes quantitative traction and qualitative shifts shaping buyer and supplier strategies. At the macro level, the market expanded from roughly USD 678 million in 2020 to about USD 1,121 million in 2025 and is forecast to continue growing at a compound annual growth rate (CAGR) of 8.76% through 2032, approaching the USD 2,017 million mark by the end of the forecast horizon. These headline numbers signal both steady adoption and an accelerating mid‑cycle opportunity for firms that position correctly in 2026.

Worldwide Maskless Lithography Machine Market

Component and subsystem breakthroughs are lowering barriers to higher throughput. Advances in digital micromirror device (DMD) pixel counts and data throughput — exemplified by recent high‑resolution DMD introductions — materially improve resolution/throughput tradeoffs that constrained maskless systems until now.

Worldwide Maskless Lithography Machine Market

Equipment vendors are consolidating product roadmaps that bridge R&D, prototyping, and low‑to‑medium volume manufacturing. Several established and emerging vendors launched upgrades or new co‑location facilities in the 2024–2026 timeframe to accelerate customer learning cycles and shorten time‑to‑process‑qualification.

Worldwide Maskless Lithography Machine Market

Regulatory and standards dynamics are tightening. Maskless tools used in microelectronics and medical device manufacturing must navigate FDA and ISO quality and environmental requirements, as well as laser‑characterization standards that impact process control and qualification time.

Computational and data‑flow bottlenecks are now strategic constraints. High data‑rate patterning and adaptive exposure require integrated hardware/software stacks; firms lacking real‑time data pipelines risk under‑utilizing improved optics and actuator capability.

Product roadmap timing: For semiconductor packaging and advanced photonics, maskless lithography should be treated as an accelerating complementary route — ideal for rapid iterations, prototype-to-pilot transitions, and targeted low‑volume production runs. Decisions on when to add maskless capability depend less on basic throughput thresholds today and more on integration with hybrid process flows (e.g., hybrid bonding, roll‑to‑roll approaches) and qualification timelines.

CapEx vs Opex tradeoffs: Given the market momentum and improving device economics, firms should model both capital procurement and service‑based access (shared labs/co‑creation platforms). The cost of ownership equation is increasingly dominated by software, metrology, and qualification labor rather than raw exposure throughput alone.

Supply‑chain concentration and single‑source risk: Critical subsystems (such as high‑pixel DMDs, precision optics, and high‑performance motion stages) are concentrated among a handful of suppliers. Procurement and design teams should qualify alternatives or secure multi‑year component commitments to avoid bottlenecks in 2026–2028.

Regulatory preparedness: Companies targeting medical, biomedical, or other regulated end markets must embed compliance planning into early tool selection and process design to minimize months of downstream validation delay.

Software and computational investments: Real‑time patterning, stitching avoidance on large formats, and adaptive exposure demand significant investments in software toolchains, FPGA/firmware optimization, and edge compute — areas where partnerships or acquisitions can deliver immediate capability.

Service and aftermarket revenue: As maskless adoption matures, services (process development, training, retrofits, and software subscriptions) will become a meaningful value pool. Vendors and service providers should craft modular commercial models that monetize both equipment and tacit process knowledge.

The market demonstrates a mid‑to‑high concentration: a set of established optics, direct‑write, and e‑beam vendors collectively shape pricing, performance expectations, and the direction of incremental innovation. Rather than presenting raw market share tables in this overview, PW Consulting highlights tactical positioning to inform 2026 strategy discussions.

Heidelberg Instruments (Heidelberg, Germany) — A global leader in high‑precision laser lithography and direct‑write platforms, Heidelberg’s product line emphasizes R&D-to-production scalability and advanced packaging process integration. Their recent upgrades reflect a focus on improved microfabrication throughput and pattern fidelity.

EV Group (St. Florian am Inn, Austria) — EVG has pushed maskless exposure into the high‑volume conversation with its LITHOSCALE family and scalable systems aimed at advanced packaging and MEMS. Their trade show presence and technical sessions underscore a strategy of pairing exposure hardware with front‑end bonding and process stacks.

Raith GmbH (Dortmund, Germany) — Specializing in high‑resolution laser beam lithography, Raith’s offerings target ultra‑fine feature work where resolution is the dominant constraint, particularly in photonics and nano‑fabrication research.

Kloe (Montpellier, France) and miDALIX (Slovenia) — These companies occupy a growing niche in accessible direct‑write and tabletop systems for labs and universities, shortening the pathway from concept to demonstrator.

JEOL, Vistec, Nanoscribe and others — Their portfolios span photomask, e‑beam, and grayscale lithography, offering differentiated resolution, throughput, and application footprints. Each vendor’s strategic play reflects tradeoffs between ultimate resolution, throughput, and integration ease.

Recent industry developments reinforce these positions: major component suppliers released higher pixel‑count DMDs that unlock new resolution/throughput points; leading OEMs launched upgraded direct‑write platforms and co‑creation facilities to accelerate commercialization of flexible electronics and advanced interconnects; and trade shows in early 2026 showcased hybrid workflows that combine maskless exposure with bonding and post‑process assembly.

Robust market sizing and scenario forecasts — Historical time series (2020–2025), a detailed 2026 baseline, and multiple scenario runs through 2032 to stress‑test capital and portfolio choices.

Actionable segmentation — Complete segmentation by region, technology architecture, and application, paired with qualitative notes on adoption drivers and risks. (Note: detailed segment tables and financial breakdowns are available within the full report.)

Vendor benchmarking and partnership playbook — Comparative matrices on product capabilities, capacity, service models, and target end markets, enabling tailored supplier selection for procurement and R&D managers.

Regulatory and standards checklist — Practical guidance for compliance planning in regulated markets (medical, automotive, aerospace), including recommended pre‑qualification activities that reduce time‑to‑market risk.

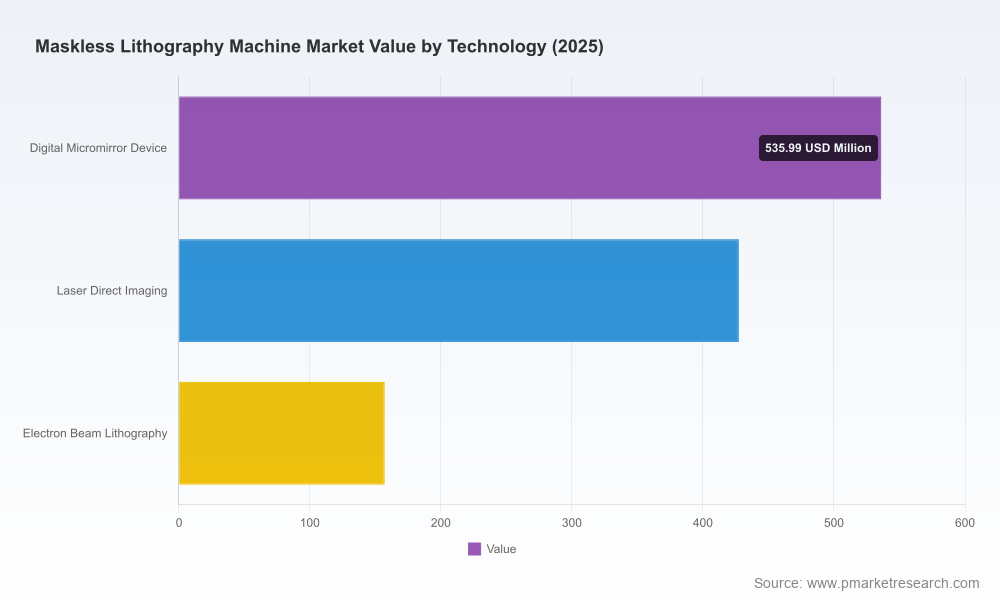

Technology deep dives — Focused analyses on DMD‑based systems, laser direct imaging, and electron‑beam direct‑write platforms covering bottlenecks, typical process envelopes, and integration risk factors.

Implementation playbooks — Roadmaps for CAPEX prioritization, shared‑service lab models, software and data stack selection, and M&A scouting criteria for corporate development teams.

CEOs and Business Unit Heads: Reassess three‑to‑five‑year product mix and go‑to‑market strategies; model outcomes under both high‑adoption and constrained‑supply scenarios.

CTOs and R&D Leaders: Prioritize integration pilots that prove end‑to‑end workflows (patterning → bonding → test) and invest in software/data integration to leverage new DMD capabilities.

Procurement and Operations: Establish multi‑sourcing strategies for critical subsystems and negotiate flexible service arrangements with equipment providers to offset lifecycle uncertainty.

Corporate Development: Identify tuck‑in targets with complementary software or metrology IP; consider strategic partnerships with co‑creation labs to accelerate customer adoption.

Regulatory and Quality Teams: Begin simultaneous process and regulatory planning for any product lines targeting medical or safety‑critical applications to reduce downstream certification time.

Maskless lithography is no longer niche. The technology’s trajectory from lab tool to an industrialized, complementary exposure technology has been accelerated by system upgrades, higher‑performance image engines, and a maturing service ecosystem. However, the commercial winners in 2026 will be those who combine hardware selection with software, metrology, and regulatory readiness — not solely those who buy the fastest scanner. PW Consulting’s report is designed as a decision‑support toolkit: it maps where the growth will occur, where bottlenecks will arise, and, most importantly for executives making 2026 commitments, how to align timing, partners, and capabilities to capture the strategic upside.

For sector leaders, engineers, procurement teams, and corporate strategists preparing 2026 plans, PW Consulting’s full report contains the granular segmentation tables, vendor scorecards, and modelable forecasts needed to convert this industry inflection into competitive advantage. Accessing the full analysis will provide the confidential detail necessary to finalize budgets, supplier selections, and integration plans for the coming buying cycle.

For detailed analysis of this topic, please visit the official page:Worldwide Maskless Lithography Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com