Worldwide Aliphatic Polysulfide Market — Strategic Briefing for 2026 Decision-Making

PW Consulting's latest market study, "Worldwide Aliphatic Polysulfide Market," equips industrial leaders, investors, and technology strategists with the context and tools needed to make high-confidence decisions in 2026 and beyond. Built on a 2020–2025 historical run and a forward-looking 2026–2032 forecast, the report synthesizes demand drivers, supply-side dynamics, regulatory pressures, and competitive positioning across the aliphatic polysulfide value chain. Our aim in this press release is to preview the analytical depth and practical utility of the full report while reserving the segment-level data and proprietary models for subscribers and direct purchasers.

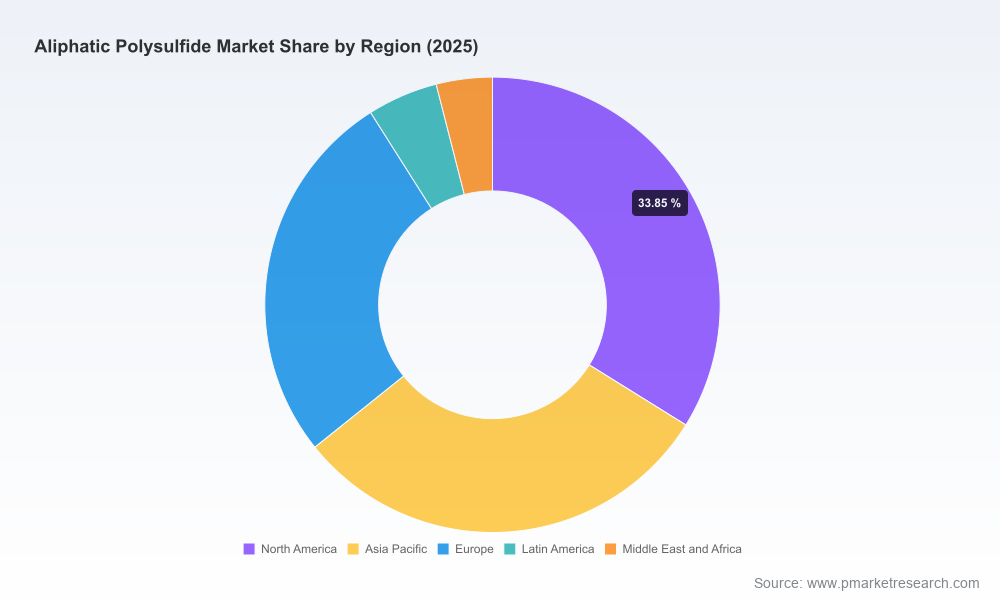

Worldwide Aliphatic Polysulfide Market

Executive snapshot: a moderate-growth, structurally resilient specialty polymer market

The aliphatic polysulfide market reached an estimated USD 428.8 Million in the base year (2025). PW Consulting’s forecast model shows a multi-year expansion through 2032, with an overall compound annual growth rate (CAGR) of 4.89% driven by steady demand in high-performance sealants, coatings, and specialty adhesives. Our deterministic baseline projects continuous growth across the 2026–2032 horizon, culminating in a materially larger global market by 2032 under base-case assumptions.

Worldwide Aliphatic Polysulfide Market

- Historical momentum (2020–2025): the market demonstrated resilience through episodic raw-material and demand-side shocks, reflecting polysulfide’s entrenched role where low moisture permeability, chemical resistance and elastic recovery are required.

- Forecast posture (2026–2032): under PW Consulting’s principal forecast the market grows at ~4.9% CAGR, a profile that rewards disciplined capacity planning, targeted product differentiation and pragmatic customer segmentation strategies.

- Concentration and competitive dynamics: the sector shows moderate-to-high concentration at the top, with the leading manufacturers accounting for a dominant share of global supply—creating both barriers and opportunities for entrants and specialty formulators.

Why this matters for 2026 strategy

For executives setting 2026 budgets and three- to five-year roadmaps, the polysulfide market represents a niche in which operational choices translate directly into price realization, customer retention and long-term margin stability. The report translates high-level growth into concrete decision levers:

Worldwide Aliphatic Polysulfide Market

- Supply resilience and feedstock risk: feedstock availability and regional price dispersion materially affect margin volatility. Late‑cycle pricing dynamics for chlorinated feedstocks have produced regional cost differentials and create short-term arbitrage opportunities for producers with flexible logistics. Procurement teams should integrate feedstock-sensitivity runs into 2026 contracts and consider dual-sourcing where feasible.

- Capex and capacity timing: with growth modest but persistent, greenfield capacity is only warranted alongside clear advantaged access to feedstock or differentiated downstream contracts. Brownfield debottlenecking, specialty grade conversion and modular capacity expansions are often higher-return plays.

- R&D and product differentiation: customer willingness-to-pay in aerospace, insulating glass, and marine applications remains linked to validated performance under temperature cycling, chemical exposure and long-term elastomeric recovery. Investment in epoxy-terminated and thiol-terminated aliphatic grades, and in low-emission curing systems, is a defensible route to premium pricing.

- M&A and commercial plays: acquisitive strategies should prioritize technology platforms (e.g., low-VOC formulations or proprietary curing systems), regional distribution footprints, and downstream sealant formulators with established OEM relationships. The concentration profile of the market means bolt-on acquisitions can rapidly improve scale economics for mid-size players.

Regulation, environmental drivers and manufacturing compliance

Regulatory dynamics are a direct input to 2026 planning. In Europe and North America, the industry continues its transition away from legacy lead-based curing agents toward alternatives such as manganese dioxide‑cured systems in response to RoHS, REACH and analogous regional restrictions. Meanwhile, point-source effluent control and pretreatment standards (for example, regulatory frameworks that govern organic chemicals and polymer intermediates) should be integrated into capital planning for both new and retrofit projects. PW Consulting’s regulatory module maps rule-sets to likely capex triggers and compliance timelines so planners can prioritize capital allocation and product reformulation roadmaps.

Competitive landscape — who matters and why

The market structure favors established specialty chemical producers and regionally entrenched manufacturers. PW Consulting’s competitive profiles analyze strategic intent, product portfolios, manufacturing footprints and commercial strategies for the principal suppliers that shape industry benchmarks:

- Nouryon — a global leader in liquid polysulfide polymers, marketed under a well-known Thioplast® franchise, which has invested in epoxy-terminated aliphatic grades targeted at coatings and adhesive markets. Nouryon’s recent product introductions underscore a premium strategy emphasizing chemical resistance and low-temperature flexibility.

- Toray Fine Chemicals — as a major Japanese producer, Toray’s polysulfide lines (including mercaptan‑terminated THIOKOL® LP grades) play a critical role in domestic construction and specialty resin modification markets. Toray’s strength is its integration with regional engineering supply chains and long-term relationships with civil engineering formulators.

- Kazan Synthetic Rubber Plant (KSRP) — an important supplier with a focus on chemical-resistant elastomer grades and industrial mastics, supporting regional industrial customers and downstream formulators.

- PPG Industries (DeSoto operations) — notable for aerospace-qualified Thiokol-branded sealants and specialty formulations for fuel tanks, windshield seals and corrosion-inhibitive primers that rely on polysulfide chemistries.

PW Consulting’s competitive matrix goes beyond logos and product lists. For each player we evaluate technology differentiation, margin architecture, contractual exposure to OEMs, and the degree of commoditization in supplied products. These evaluations are cross-referenced with market concentration metrics to assess the likely evolution of supplier bargaining power through 2026 and beyond.

Raw materials and cost outlook — what to watch

Feedstock economics remain a proximate driver of profitability. The report examines the entire upstream-to-downstream chain: from the availability and pricing of chlorinated feedstocks used in polysulfide synthesis to the logistics and inventory strategies that industrial buyers employ to flatten cost cycles. Geographic disparities in feedstock availability and PVC-related demand cycles create pockets of margin pressure and opportunities for geographically advantaged producers. PW Consulting provides scenario-driven price sensitivity analyses and breakeven curves to help procurement and finance teams stress-test budgets under multiple commodity paths.

What’s inside the full PW Consulting report — practical deliverables

The report is designed as an operational playbook for teams that must act in 2026. Key contents include:

- Executive briefing and three strategic scenarios (base, upside, downside) with quantified demand implications;

- Multi-year demand model (2020–2032) by macro segment and product architecture, with transparent assumptions and an interactive version available to clients;

- Supplier and capacity maps with plant-level capability assessments and simple cost curves for marginal producers;

- Regulatory impact matrix aligning major regimes (including effluent and chemical controls) with reformulation and compliance capex triggers;

- Raw-material sensitivity and procurement playbook, including hedging and dual-sourcing strategies;

- Technology and innovation landscape—benchmarks for liquid vs. solid polysulfide polymer approaches, curing chemistries, and routes to lower-emission formulations;

- Commercial go-to-market templates: OEM account segmentation, margin-preserving pricing approaches, and contract structures for long-term supply agreements;

- M&A target shortlist methodology and scorecards for screening bolt-ons and value-accretive assets;

- Risk register and prioritized mitigation plans, from feedstock outages to regulatory shocks and downstream substitution threats.

How clients use the report in 2026

Clients typically deploy the PW Consulting report across four use cases in their 2026 planning cycle:

- Capital allocation — to justify or defer capacity projects using scenario-weighted NPV analyses;

- Procurement and commercial negotiation — to set reference prices and contract indexation clauses tied to feedstock proxies;

- New product introduction and R&D prioritization — to allocate resources toward grades that command structural premiums in aerospace or insulating glass markets;

- M&A and portfolio strategy — to identify targets that fill geographic gaps, add differentiated chemistries, or improve captive feedstock access.

Selective case signals and tactical recommendations for 2026

- Prioritize supply agreements that include flexible take-or-pay bands and feedstock pass-through mechanics to protect margins during commodity swings.

- Accelerate validation of low‑emission curing systems to preempt regulatory-driven displacement of legacy chemistries and secure premium OEM approvals.

- Favor time-limited brownfield expansions and targeted product upgrades over large greenfield commitments unless feedstock or offtake certainty is demonstrable.

- Use competitor product launches and patent landscaping to inform defensive R&D and licensing strategies—early awareness of new epoxy-terminated aliphatic grades can change seat-of-the-pants pricing and contract negotiations.

Read the full analysis

The above is a strategic preview intended to convey the practical value and decision-focused orientation of PW Consulting’s Worldwide Aliphatic Polysulfide Market report. For the complete dataset, proprietary segment-level forecasts, plant-by-plant supply maps, and downloadable modeling tools, please consult the full report on PW Consulting’s website. Detailed regional and application splits, supplier share tables and unit-cost curves are preserved in the full report to enable rigorous due diligence and transaction support.

Contact PW Consulting to request the full report, schedule a briefing with our lead analysts, or commission custom scenario runs tailored to your company’s portfolio. In a market where feedstock dynamics, regulatory change and OEM qualification timelines interact, a structurally informed strategy is the difference between chasing short-term volume and capturing long-term margin.

For detailed analysis of this topic, please visit the official page:Worldwide Aliphatic Polysulfide Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com