https://www.facebook.com/ProstaSurgeXCapsules

Art |

2026-04-27 11:30:00

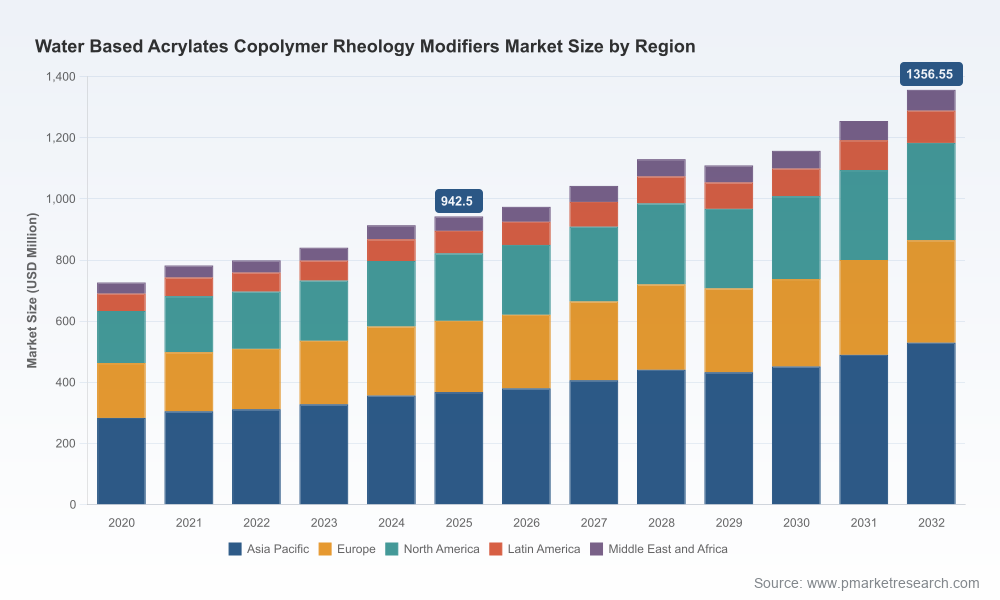

PW Consulting’s new industry report on the Worldwide Water Based Acrylates Copolymer Rheology Modifiers market delivers a focused intelligence package designed to inform executive decisions in 2026. The market has shown steady expansion over the past half‑decade, rising from mid‑2020 levels to an estimated USD 942.5 Million in 2025. Our baseline forecast points to a compound annual growth rate (CAGR) of approximately 5.34% over the 2026–2032 horizon, taking the market toward a multi‑hundred‑million dollar opportunity by 2032. This briefing highlights the strategic implications embedded in those headline numbers and explains how the full PW Consulting report converts them into operational decision support without revealing the granular splits that constitute our paid model.

Worldwide Water Based Acrylates Copolymer Rheology Modifiers Market

Rheology modifiers based on acrylates copolymers are a cornerstone technology across multiple water‑based formulations — from paints and coatings to personal care, adhesives and household cleaning. For 2026, three structural forces determine the choices available to suppliers, formulators and investors:

Worldwide Water Based Acrylates Copolymer Rheology Modifiers Market

Executives who treat the market as a stable “sell more of the same” opportunity will under‑invest in procurement sophistication and product differentiation. Conversely, those who use a quantified view of demand growth and concentration to guide portfolio and sourcing choices will capture outsized margins in 2026.

Worldwide Water Based Acrylates Copolymer Rheology Modifiers Market

From 2020 through 2025 the market expanded materially, reflecting both recovery following macro shocks and ongoing shifts toward water‑based systems in mature and emerging end‑uses. Our forecast to 2032 reflects a steady continuation of that trend at a 5.34% CAGR. That trajectory supports a two‑track strategy in 2026: consolidate in established product families where scale and service win, and selectively invest in new chemistries and formulations where customers are actively seeking sustainability or performance advantages.

PW Consulting’s full model contains granular regional, technology and application splits, plus pricing and margin scenarios. In this release we deliberately withhold those detailed cells and charts — the headline growth and directionality are supplied here to demonstrate the report’s strategic relevance while reserving the actionable numbers for purchasers of the full study.

Recent product initiatives illustrate these dynamics. In 2025 a leading supplier announced a bio‑oriented rheology polymer ahead of its full launch, and later supplied comparative performance data showing parity with incumbent acrylates in rinse‑off systems. Such product motions accelerate customer trials and can shift procurement criteria within 12–18 months — a horizon that matters for 2026 budgeting and partnership decisions.

Raw material movements are the single most important short‑term driver of margins in 2026. Across 2025 and into Q1 2026, acrylic acid pricing exhibited material regional divergence: China experienced a notable softening through 2025, while North American prices showed a modest fall in early 2026. At the same time, a major producer implemented list price adjustments in March 2026 citing cost pressures.

Those ostensibly contradictory signals create both risk and opportunity:

PW Consulting’s report provides a quantified risk matrix tying acrylic monomer scenarios to supplier P&L outcomes. The matrix is intentionally excluded from this preview but is central to the tactical playbook we recommend for procurement teams in 2026.

The market is clustered: the top global players account for meaningful shares of supply, yet there remains room for regional specialists and differentiated niche providers. Market concentration metrics show that the three largest players represent a substantial portion of global supply, and the leading five approach a majority share — a structure that favors scale but still allows focused players to win through formulation intimacy and service.

Key players we track include major integrated chemical companies and specialists that combine polymer know‑how with personal‑care or coatings go‑to‑market capabilities. Their maneuvering in 2025–early 2026 reveals several strategic postures:

Notable company initiatives in the last 18 months include pre‑commercial launches of sustainable rheology polymers, performance claims that challenge incumbent technologies, and list price adjustments by monomer producers. For commercial leaders in 2026, the competitive question is no longer just “what do we sell?” but “how do we bundle product, service and risk mitigation to be the preferred strategic supplier?”

Each element is accompanied by ready‑to‑use slides and executive summary decks so that commercial and strategy teams can move from insight to action within weeks, not months.

For boards and C‑suites, the core question is resource allocation: which pockets of the acrylates rubric will deliver margin and growth in the next 18–36 months, and which ones are tactical plays requiring defensive actions? PW Consulting’s model turns headline CAGR and market size into a prioritized list of initiatives with expected ROI windows. For commercial teams, the technical playbooks and supplier scorecards in our full report translate directly into account strategies and tender responses.

We built the report with the explicit goal of converting market forecasting into executable plans — from procurement term sheets to R&D roadmaps. The analysis you see here demonstrates the report’s strategic value while reserving the detailed, transaction‑grade data behind the paywall — a deliberate “trailer” to show capability while protecting the high‑value datasets that our clients rely on.

For access to the complete dataset, scenario tools, supplier scorecards and the tactical playbooks described above, please refer to PW Consulting’s full market report. The full study is the tool that will let your organization translate the 2026 market environment into defensible, revenue‑generating action.

For detailed analysis of this topic, please visit the official page:Worldwide Water Based Acrylates Copolymer Rheology Modifiers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com