Worldwide Wafer and Integrated Circuits (IC) Shipping and Handling Market: Strategic Imperatives for 2026

PW Consulting presents an executive briefing distilled from our new market intelligence release, "Worldwide Wafer And Integrated Circuits (IC) Shipping And Handling Market." As senior industry strategists, we designed this briefing to orient corporate leaders, procurement chiefs, and strategic planners for the decisions that will matter most in 2026. The analysis below highlights the macro trajectory, competitive dynamics, operational stress points, and actionable playbooks embedded in the full report — while deliberately preserving the granular segment-level tables and models for readers who access the full study.

Worldwide Wafer And Integrated Circuits (IC) Shipping And Handling Market

Macro picture: steady expansion with structural inflections

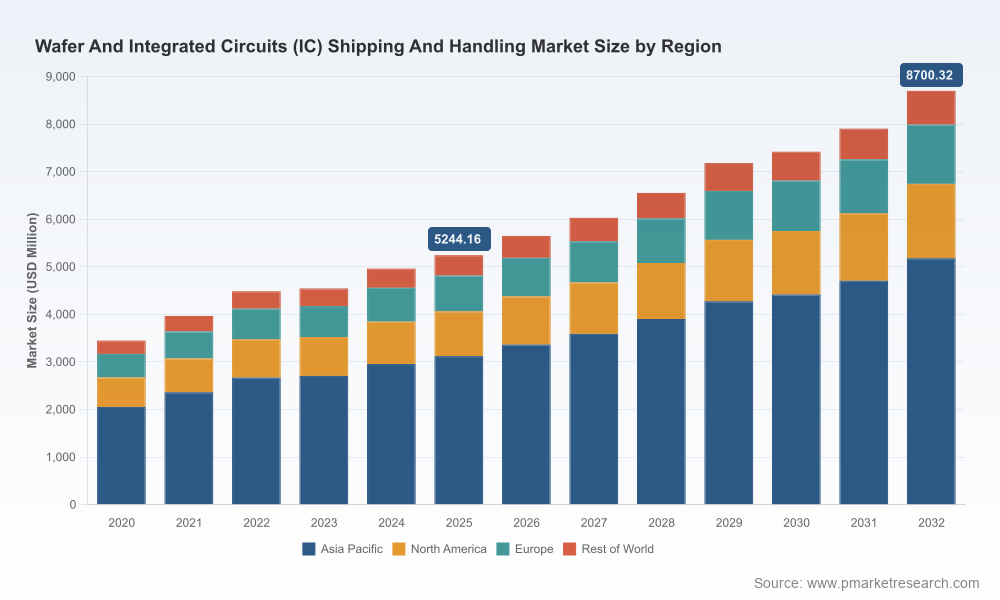

Between 2020 and 2025 the market expanded meaningfully, moving from a base measured in the low billions to surpassing USD 5.2 billion (USD Million denominated reporting) in our 2025 base year. Our model projects continued compound growth at a 7.51% CAGR through the forecast horizon, with the market approaching roughly USD 8.7 billion by 2032. That trajectory masks important phase changes: increased wafer diameters and automation investments, more complex regional trade dynamics, and pronounced supply-side constraints for specialty polymers that serve as the raw materials of many carrier and shipper systems.

Worldwide Wafer And Integrated Circuits (IC) Shipping And Handling Market

What the full report delivers (practical, operational content)

- A transparent market-sizing methodology with reconciled historicals (2020–2025) and scenario-driven forecasts (2026–2032).

- Decision-ready supplier maps and tiering frameworks that link capability (e.g., contamination control, automation compatibility) to commercial terms and lead-time risk.

- Actionable risk matrices for sourcing teams that quantify exposure to raw material constraints, export/regulatory shock, and regional policy shifts.

- Playbooks for procurement and operations: contract clauses, buffer inventory heuristics, qualification checklists for pods/FOUPs/FOSBs, and inspection/validation protocols for incoming carriers.

- Detailed company profiles and capability heatmaps for incumbent and niche suppliers, including capital intensity, automation integration, and R&D focus.

- Integrated benchmark tools to model TCO (total cost of ownership) across carrier choices, including failure modes, contamination events, and automation retrofit costs.

- Scenario-based M&A and alliance recommendations tuned to concentration dynamics and potential consolidation opportunities.

Note: this briefing intentionally omits the granular regional and application split tables and individual product segment financials that are present in the full report; those detailed datasets are available only through our download portal to preserve the integrity of our primary research and to encourage direct engagement with the underlying models.

Worldwide Wafer And Integrated Circuits (IC) Shipping And Handling Market

Competitive landscape — what we see and why it matters in 2026

The market exhibits a moderate degree of concentration: the top three suppliers account for nearly half of the market, and the top five approach two-thirds. That structure creates both competitive pressures and strategic openings for mid-sized specialists and vertically integrated players.

- Entegris Inc. — With industry-leading wafer shipping solutions optimized for 300mm ecosystems (FOUPs, FOSBs, and horizontal shippers), Entegris combines contamination-control expertise with strong automation compatibility. For global firms, Entegris represents a security-of-supply anchor; for competitors, it sets the bar on integration with tool vendors and fabs.

- Shin-Etsu Polymer and Miraial — Japan-based polymer specialists command material know-how that is increasingly strategic given resin supply constraints. Their capability to engineer polymer compounds for lower particle generation and improved long-term stability aligns directly with fabs’ quality objectives.

- Brooks Automation — Positioned at the intersection of handling automation and shipping hardware, Brooks is a key partner for customers pursuing closed-loop automation upgrades that minimize human intervention during wafer transport.

- ePAK, Pozzetta, Gudeng, Chuang King, and regional specialists — These vendors provide differentiated value through customization, local service footprints, and competitive pricing. They matter in multiregional sourcing strategies where lead-times and local compliance are decisive.

- Smaller niche players (3S Korea, ITW ECPS, Dalau, Daitron, Achilles, Ted Pella) — Often overlooked in strategic planning, these firms fill critical roles in specialty applications, prototype flows, and geographic-specific support arrangements.

Strategic implication: buyers should adopt a layered supplier strategy that mixes global leaders for reliability with regional specialists for agility. Sellers should evaluate whether to deepen material science capabilities, invest in automation interfaces, or pursue bolt-on acquisitions to expand service footprints.

Key market dynamics and 2026 risk vectors

- Regulatory decoupling and export controls — Recent measures introducing case-by-case license reviews for sophisticated compute chips and new tariff treatments have already influenced equipment and component flows. These actions create a non-linear risk premium for suppliers whose production footprints are concentrated or whose products are dual-use.

- Raw material constraints — Supply limitations for certain advanced resins are producing persistent lead-time and cost pressures. This acts as a tax on unit economics for polymer-based carriers and elevates the value of material-substitution roadmaps.

- Standards and automation — Industry standards (e.g., for FOUP and FOSB interfaces) remain critical. Products that preserve automation compatibility and meet contamination-control benchmarks will command preference and price resilience.

- Geopolitical tooling requirements — Recent rules requiring down-spec tool versions for certain markets have ripple effects across the supply chain; suppliers must plan for bifurcated product variants and associated certification efforts.

- Concentration and consolidation pressure — With nearly half the market served by three suppliers and a sizeable share by five, M&A activity is a plausible path for firms seeking scale in logistics, regional service, or material R&D.

Actionable strategic recommendations for 2026

- Sourcing and supplier risk: Implement a dual-sourcing mandate for critical carriers and negotiate volumetric commitments with price-adjustment clauses tied to resin indices or lead-time thresholds. Include qualification pathways for regional specialists to act as temporary surge suppliers.

- Inventory and operations: Recalibrate buffer policies to reflect not just demand variability but supplier-specific lead-time volatility. Prioritize automation-compatible carriers in capital planning to reduce manual touchpoints that increase contamination risk and labor dependency.

- Product and engineering: Invest in cross-functional material-substitution projects that reduce dependency on constrained resin inputs. Design modular carrier interfaces to simplify SKU proliferation when dual-spec variants are required by regulation.

- Regulatory and geopolitical planning: Incorporate export-control scenario planning into procurement and logistics playbooks. Establish contingency routing and qualification of alternative carriers for regions with emerging licensing friction.

- M&A and partnerships: For buyers seeking to secure supply, prioritize targets that add material science capabilities, local manufacturing footprints, or automation integration expertise. For suppliers, consider alliances with tool OEMs to lock in automation compatibility as a competitive moat.

Three scenarios to monitor and their 2026 triggers

- Base case (Policy-managed growth): Continued investment in capacity and automation, with manageable resin shortages resolved through incremental capacity additions. Trigger: stable regulatory posture and gradual easing of lead times.

- Acceleration (Tech-driven uptake): Rapid adoption of larger wafer diameters and high-mix automation increases demand for advanced carriers. Trigger: a meaningful step-change in wafer fab capex focused on advanced nodes and HVM ramps.

- Downside (Supply shock and policy disruption): Acute resin blockage or tightened export controls that bifurcate supply channels materially raise costs and cause reorder delays. Trigger: prolonged resin plant downtime or a new tranche of export restrictions with practical operational impacts.

How senior leaders should use the full report in 2026 planning

- Procurement: use our supplier heatmaps and TCO calculators to reprice long-term agreements and to model insurance strategies against lead-time spikes.

- Operations: adopt the report’s qualification checklists to accelerate onboarding of alternate carriers and to reduce qualification cycle time.

- Strategy & M&A: use concentration analytics and scenario models to prioritize targets that offer either material-security or automation integration benefits.

- R&D and engineering: leverage the material substitution playbooks and lab-validation protocols to fast-track lower-risk replacements for constrained resins.

Closing: an invitation to the full intelligence

The condensed insights above capture the most consequential structural forces shaping the wafer and IC shipping and handling market as firms prepare for 2026. PW Consulting’s full report includes the exhaustive datasets, segment-level models, vendor scorecards, and playbooks referenced here — tools designed to move teams from strategy to execution. In keeping with our "trailer" principle, we have preserved the detailed regional and segmental tables for the full study to ensure clients who rely on those granular inputs receive validated, actionable intelligence.

For procurement leaders, operations executives, and corporate strategists that need to translate this landscape into defensible 2026 plans — including contract language templates, actionable supplier shortlists, and scenario-specific contingency roadmaps — we recommend downloading the full report and engaging with PW Consulting’s advisory team for a bespoke workshop that aligns the research to your specific footprint and risk profile.

For detailed analysis of this topic, please visit the official page:Worldwide Wafer And Integrated Circuits (IC) Shipping And Handling Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com