Worldwide Digestive Bitters Market — Strategic Preview for 2026 Decision-Makers

Executive preview

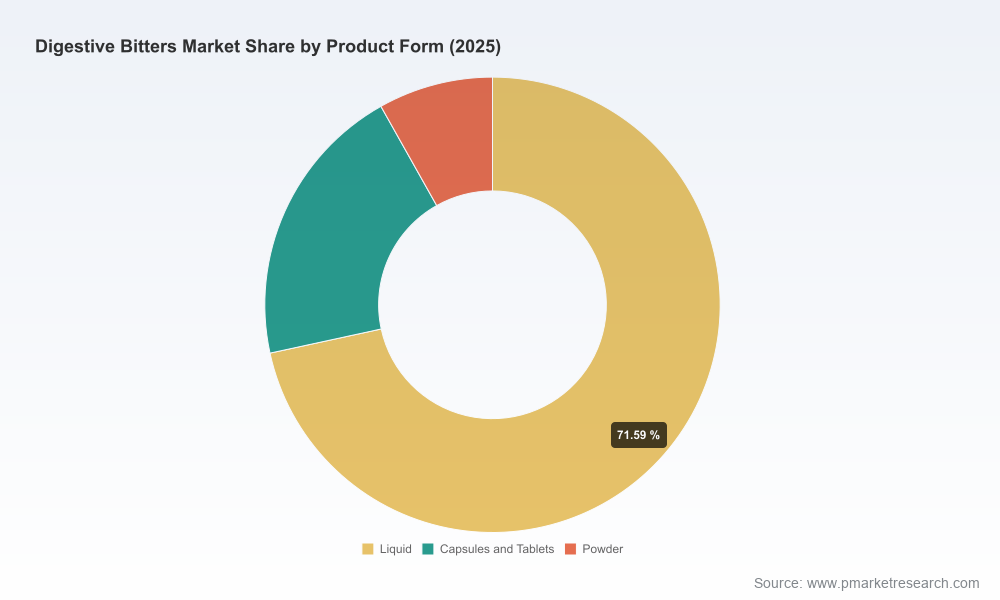

PW Consulting’s new Worldwide Digestive Bitters Market report (base year 2025; historical series 2020–2025; forecast 2026–2032) synthesizes primary research, retailer data, product audits and clinical/regulatory inputs into a single decision-grade asset. The global market for digestive bitters has expanded from roughly USD 1.28 billion in 2020 to approximately USD 1.65 billion in 2025 and, under our central forecast, is projected to reach about USD 2.39 billion by 2032 — an implied compound annual growth rate (CAGR) of 5.48% across the 2026–2032 forecast window. That growth reflects a confluence of consumer health trends, innovation in formulation and delivery formats, and an evolving regulatory and distribution landscape.

Worldwide Digestive Bitters Market

Why this matters for 2026 planning

- Timing for strategic bets: 2026 is a make-or-break year for players deciding whether to move from niche lifestyle positioning into mainstream therapeutic-adjacent claims. The market trajectory supports continued investment, but only where firms can demonstrate differentiated efficacy, supply security and regulatory clarity.

- Portfolio and channel optimisation: The next 18 months will determine which go-to-market models scale profitably — direct-to-consumer digital formats, mission-driven specialty retail, or hybrid omnichannel approaches backed by partnerships with beverage and hospitality sectors.

- M&A and partnership signal: Consolidation and bolt-on acquisitions will accelerate among firms that need rapid access to certified organic supply chains, validated clinical evidence, or broader distribution infrastructure.

What the report contains — practical, actionable deliverables

This report is designed to be operational from day one. It does not only describe market trends; it equips executives and line managers with tools to act.

Worldwide Digestive Bitters Market

- Comprehensive market sizing and transparent methodology (historical reconciliation 2020–2025; base year 2025; scenario-based forecasts 2026–2032).

- Investor-grade financial models and P&L sensitivity templates that allow users to test product launches, pricing, and channel mix assumptions.

- Go-to-market playbooks for three commercial archetypes — heritage brands, digitally native challengers, and ingredient-to-formulation specialists — with actionable KPIs and 90‑, 180‑ and 360‑day milestone maps.

- Regulatory and quality map covering the major regulatory regimes encountered by exporters and domestic manufacturers (including practical checklists for GMP alignment, claims language and label risk).

- Supply chain risk matrix and raw-material traceability framework tailored to botanical inputs frequently used in digestive bitters (including due-diligence templates for multi-country herb sourcing).

- Consumer and use-case segmentation with purchasing triggers, price tolerance buckets and messaging frameworks designed to increase conversion in both retail and e‑commerce environments.

- Channel economics and assortment playbooks for specialty retail, foodservice and online channels — including promotional levers, private-label considerations and fulfillment trade-offs.

- Competitive benchmarking and vendor scorecards that combine product, channel and operational metrics to highlight defensible advantages and acquisition targets.

Competitive landscape — what incumbents and challengers are doing

Our qualitative and portfolio-level analysis focuses on firms whose market behavior shapes the category’s evolution. Below is an executive synthesis of their strategic posture and the implications for competitors and potential acquirers.

Worldwide Digestive Bitters Market

- Underberg AG (Rheinberg, Germany — https://underberg.com/)

Positioning: Heritage, single-product concentration with deep provenance storytelling. Strengths are brand equity and long-standing global placement in travel retail and specialty channels. Strategic implication: incumbency advantage in heritage-led categories can be extended via limited editions and partnerships, but growth requires expanding beyond traditional after‑meal use cases.

- House of Angostura / Angostura Limited (Laventille, Trinidad and Tobago — https://angostura.com/)

Positioning: Iconic bitters with strong crossover into beverage mixology. Recent product activity (notably a 200‑year anniversary limited edition) highlights dual revenue streams — bar/cocktail demand plus occasional digestive positioning. Strategic implication: beverage-led brands can monetise premiumisation and co-branding with hospitality, but must clarify claims when moving toward digestive supplement channels.

- Urban Moonshine (Burlington, Vermont, USA — https://urbanmoonshine.com/)

Positioning: Certified organic, wellness-first formulations marketed for gut comfort and liver support. Strengths are ingredient transparency and clean-label storytelling. Strategic implication: organic, medicinal-adjacent positioning attracts wellness consumers but requires regulatory diligence on claims and validated supply for premium botanicals.

- Gaia Herbs (Brevard/Mills River, North Carolina, USA — https://gaiaherbs.com/)

Positioning: Farm-to-bottle narrative with regenerative practices; product innovation includes anti-inflammatory and digestion-centric blends. Strengths are vertical integration and clinical marketing. Strategic implication: integrated ingredient-to-brand models reduce supply volatility and can support faster innovation cycles.

- Herb Pharm (Williams/Medford, Oregon, USA — https://herb-pharm.com/)

Positioning: Certified organic extract lines and a diversified botanical portfolio. Strengths include established herbalist credibility and broad wholesale penetration. Strategic implication: supply-side specialists are attractive M&A targets for brands seeking GMP‑aligned bulk extracts and private‑label capacity.

- Botanica (TallGrass Natural Health, Canada)

Positioning: Liquid herb blends combining classic bitter herbs for digestive function. Strengths lie in formulation variety and category relevance in natural health retailers. Strategic implication: nimble formulators can win shelf space quickly but must formalise claims and testing to scale across regulated markets.

Regulation, evidence and raw‑material realities — immediate operational risks

Three contextual dynamics should guide 2026 operational plans:

- Clinical and prescribing environments are fragmenting: Recent real‑world observations from integrative-care settings (notably a Swiss prescription database study) indicate that herbal bitters are incorporated into routine care only when products are commercially registered or produced under certified GMP magistral processes. This raises the bar for firms seeking mainstream medical acceptance.

- Claims and labelling remain high-risk in major markets: In the United States, digestive bitters marketed as supplements carry statutory disclaimers and cannot make disease-treatment claims; similar guardrails exist in other regulated jurisdictions. Brands aiming to translate functional benefits into clinical claims must plan regulated clinical pathways well in advance.

- Botanical sourcing and traceability are strategic levers: Flagship formulations rely on botanicals such as gentian, dandelion, artichoke, orange peel and burdock among others. High-quality sourcing (often cross-border and multi-origin) is increasingly scrutinised by retailers and regulators; brands that can demonstrate inspected, traceable supply chains will command premium pricing and lower recall risk.

Practical 2026 playbook — recommendations by function

- Commercial leaders: Prioritise channel pilots that test premium bundles (e.g., bitters + digestive educational touchpoints) in specialty retail and subscription channels; require 12‑week cohort metrics before scaling.

- R&D and Product: Standardise extract specifications and stability protocols; invest in two bio‑assay validation studies for top-selling SKUs to unlock PAC (physician, athlete, consumer) endorsement routes.

- Supply chain: Create multi-sourced supplier panels for the top five botanical inputs and implement a robust supplier-audit calendar with contingency inventory targets tied to lead-time scenarios.

- Regulatory & Quality: Map product variants to the regulatory pathways of priority markets (including magistral/medicinal routes where applicable) and develop label language playbooks that preserve consumer benefit messaging without triggering prohibited claims.

- M&A & Corporate Development: Use a two‑track screening funnel: (1) short list targets that deliver immediate supply or channel access; (2) longer-term bolt‑ons that offer clinical evidence or proprietary extraction processes.

- Finance & Investors: Base three-year cash-flow models on the report’s scenario outputs and stress-test for higher cost of goods driven by botanical scarcity or certification premiums.

How to use PW Consulting’s report

This release is a strategic trailer: it conveys the high-level market trajectory and the decision use cases that PW Consulting believes will matter most in 2026, while preserving the granular segment and channel-level detail for the full report package. The full deliverable includes interactive dashboards, downloadable financial models, supplier due-diligence templates and a confidential annex with granular segmentation and regional/channel level metrics. These elements are intentionally gated because they are the competitive differentiator for market participants preparing bids, partnerships or M&A activity in 2026.

For teams assessing product launches, M&A targets, supply security or regulatory pathways, the report functions as both a roadmap and a playbook: it tells you where the value pools are growing, what structural risks can erode margins, and which operational moves compress time-to-scale.

Next steps

PW Consulting is available to run customised workshops that map this intelligence directly onto corporate strategy, including bespoke modelling, target screening and a 90‑day implementation sprint to operationalise the report’s recommendations. Access to the full dataset, chapter-level forecasts and interactive models is available through our report order page or by contacting our industry team for an executive briefing.

For detailed analysis of this topic, please visit the official page:Worldwide Digestive Bitters Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com