Laptop Repairing Course in Delhi

Other |

2026-05-22 08:09:44

PW Consulting is pleased to release a strategic preview of our forthcoming market research report on the Worldwide Progressive Familial Intrahepatic Cholestasis (PFIC) Type 2 treatment market. As a targeted, ultra-rare indication with a rapidly evolving therapeutic landscape, PFIC Type 2 presents both acute clinical complexity and concentrated commercial opportunity. This briefing distills the report’s most decision-relevant insights for 2026 corporate strategy while preserving the proprietary segmentation data that drive tactical actions — a deliberate “trailer” approach designed to demonstrate our analytical depth and compel investment in the full dataset and model.

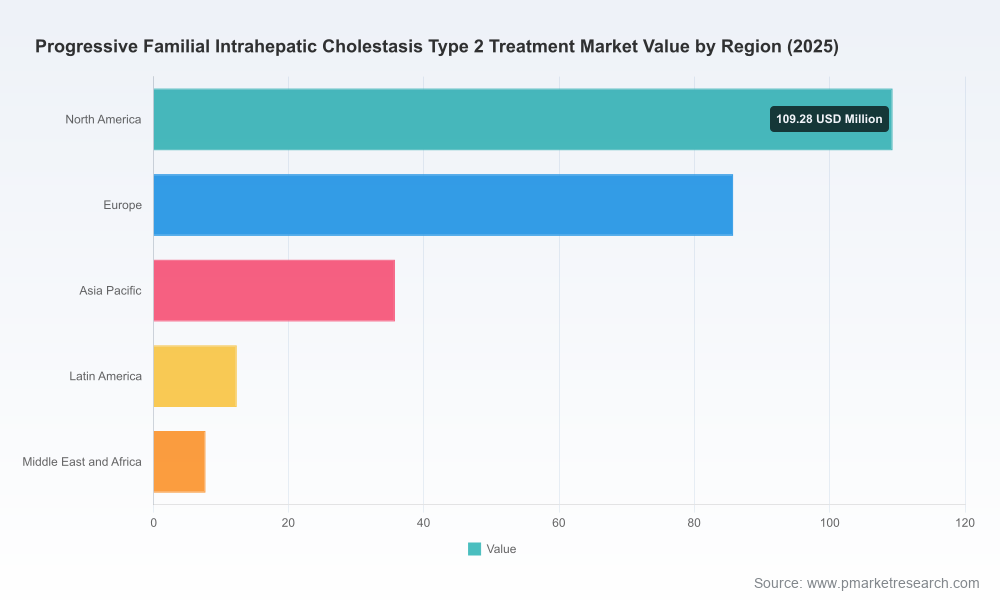

Worldwide Progressive Familial Intrahepatic Cholestasis Type 2 Treatment Market

PFIC Type 2 is transitioning from an almost exclusively supportive-care model to a specialty-therapeutics market shaped by disease-modifying approaches, targeted IBAT inhibitors, and a maturing pipeline of genetic interventions. Our analysis — built on historical 2020–2025 trends with 2025 as the base year and a forecast horizon of 2026–2032 — quantifies that transition. The market is exhibiting a robust compound annual growth rate (CAGR) of 19.34%, moving from a modest base at the start of the decade to a materially larger specialty market by the early 2030s.

Worldwide Progressive Familial Intrahepatic Cholestasis Type 2 Treatment Market

Key headline trajectory (USD, Million): the market scaled substantially through 2020–2025 and is projected to grow meaningfully across 2026–2032 under current therapeutic and regulatory assumptions. For executives planning clinical investments, commercial launches, manufacturing scale-up or partnership strategies in 2026, the numbers underpin a clear opportunity but demand precise segmentation, timing and payer strategy to capture value efficiently.

Worldwide Progressive Familial Intrahepatic Cholestasis Type 2 Treatment Market

Therapeutic evolution: The emergence and regional expansion of ileal bile acid transporter (IBAT) inhibitors has shifted treatment paradigms from symptomatic management to targeted symptom control and potentially improved long-term outcomes, changing prescribing behavior among pediatric hepatologists and transplant centers.

Clinical pipeline and gene therapy potential: Gene therapy and precision-medicine candidates targeting the underlying ABCB11 defects are progressing through early development. These programs — while still nascent compared with approved pharmacologics — materially affect long-term strategic planning for incumbent and prospective entrants (distribution rights, manufacturing, and long-term patient registries).

Market concentration and commercialization levers: The PFIC Type 2 market is highly concentrated among a small number of specialty drug developers and partners. This concentration accelerates the emergence of dominant channel strategies and payer negotiations but also preserves pockets of strategic flexibility for late entrants that can demonstrate differentiation in outcomes or cost-effectiveness.

Regulatory nuance and label limitations: Approved IBAT therapies carry indication-specific limitations tied to BSEP functionality. Those limitations create clinically meaningful subgroups within PFIC Type 2 that require nuanced clinical and diagnostic strategies (genotyping, biomarker-driven patient selection) to optimize label-consistent use and reimbursement.

Our report provides granular, actionable profiles of leading developers and commercialization partners shaping PFIC Type 2 treatment access and adoption. Two companies require specific attention in near-term strategic planning:

Ispen — With Bylvay (odevixibat) approved across multiple markets, Ipsen acts as a commercial anchor in key jurisdictions. Recent regulatory momentum, including approval in Japan (September 2025), reinforces its regional launch playbook and post-marketing evidence generation strategy. Ipsen’s global commercialization footprint and partner network position it to defend share via integrated medical affairs, physician engagement and pediatric hepatology center access.

Mirum Pharmaceuticals — Mirum’s LIVMARLI (maralixibat) has advanced both formulation access and label breadth, including a tablet formulation approval (April 2025) and regulatory approvals via partners in major markets. Mirum’s investment in broader trial enrollment (completed Phase 3 EXPAND enrollment in March 2026) indicates a strategic intent to expand label-eligible populations and to generate comparative evidence that will influence payer and prescriber decision-making.

Both companies’ labels contain clinically consequential limitations for patients with non-functional or absent BSEP protein, creating an effectively segmented patient pool that will be addressed through diagnostics, off-label supportive care and emerging gene-targeted modalities. For market entrants and incumbents, this creates a dual-track strategy: optimize approved-therapy uptake in label-eligible patients while investing in differentiated solutions for biologically refractory subgroups.

Label constraints: Prescribing information for current IBAT inhibitors includes explicit contraindications or cautions for patients with severe BSEP defects. Commercial teams must align medical education and diagnostic reimbursement strategies to maximize treated, eligible populations and to reduce inappropriate off-label use.

Payer expectations: Rare-disease payers increasingly demand post-launch real-world evidence (RWE) and outcomes-based contracting. Our report models several payer negotiation scenarios to quantify the financial and access impact of outcomes guarantees, risk-sharing agreements and registry-driven coverage decisions.

Supportive treatment economics: Established symptomatic agents (e.g., ursodeoxycholic acid, bile-acid sequestrants, rifampicin) remain part of many treatment pathways. Strategic combinations, sequencing studies and economic models will influence formulary positioning, especially where IBAT inhibitors carry label-based exclusions.

Recognizing that execution determines value capture in ultra-rare markets, the full PW Consulting report is designed as a hands-on toolkit for 2026 decision cycles. Key deliverables include:

Market sizing and forecast model (2020–2032, USD Million) with configurable assumptions so teams can stress-test scenarios for pricing, uptake, and pipeline shifts.

Patient-journey mapping and diagnostic workflows that identify critical clinical touchpoints and bottlenecks affecting diagnosis, referral and treatment initiation.

Commercial archetypes and channel economics tailored to hospital pharmacies, specialty pharmacies and outpatient settings, including reimbursement pathways and inventory/fulfillment considerations.

Regulatory and HTA prioritization matrix that ranks launch sequences by expected payer receptivity, clinical need, and evidence gaps that can be closed in the first 24 months post-launch.

Partnership and M&A playbook — valuation frameworks, milestone structures and due diligence checklists focused on gene-therapy candidates and diagnostic platforms relevant to PFIC Type 2.

Clinical development optimization guidance — trial design alternatives, endpoint selection, and patient-enrichment strategies to accelerate label expansion while preserving payer credibility.

Prioritize diagnostic access and genotyping programs now. Given label-linked BSEP constraints, ensuring rapid, reimbursed genotyping will maximize the addressable population for approved therapies and reduce leakage to less efficient care pathways.

Accelerate post-approval evidence generation with operationalized registries and pragmatic studies. Payers will seek outcomes data; early investment in RWE infrastructure will materially lower coverage friction and support value-based contracting.

Consider adaptive commercialization strategies that defer full-capex investments until post-market data validate price and utilization. For potential entrants, licensing or co-commercial agreements can be an efficient path to scale in a concentrated competitive field.

Treat gene therapies as strategic inflection points. Even if not immediate revenue drivers, gene therapies redefining curative potential will change lifetime-cost calculations and payer willingness to reimburse high upfront prices — and therefore influence discounting and contracting strategies for small-molecule incumbents.

To preserve the commercial utility of the full research package and to comply with our “trailer” principle, this briefing demonstrates analytic depth while intentionally withholding the detailed splits and proprietary sub-segment figures that operational teams use to construct launch and investment models. Specifically, fine-grained regional/application/channel shares, therapy-type dollar splits, and certain modeled payer-reimbursement curves are available exclusively in the full report and interactive model.

Executives seeking to convert 2026 opportunities into measurable results should access the complete dataset, which includes downloadable scenario models, region- and channel-level assumptions, and downloadable go-to-market templates.

For market-access leads, R&D strategists, business development teams and C-suite decision-makers preparing 2026 plans: PW Consulting’s full Worldwide PFIC Type 2 Treatment Market report provides the validated numbers, scenario tools and strategic playbooks necessary to move quickly and with confidence in a high-growth, high-stakes therapeutic area.

Contact PW Consulting to request the full report, secure a briefing with our lead analysts, or license the underlying forecast model. Our team will walk you through the assumptions, provide sensitivity analyses tailored to your portfolio, and help you define concrete next steps for commercial launch, evidence generation, and partnership negotiation.

For detailed analysis of this topic, please visit the official page:Worldwide Progressive Familial Intrahepatic Cholestasis Type 2 Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com