Worldwide Ionic Hydroxypropyl Starch Ether Market — 2026 Strategic Outlook: PW Consulting Releases Actionable Intelligence for Executive Decision-Making

PW Consulting today publishes its authoritative market brief, "Worldwide Ionic Hydroxypropyl Starch Ether Market — 2026–2032 Strategic Outlook," designed as a practical playbook for corporate leaders, procurement teams, R&D heads and private investors preparing decisions in 2026. Built on a comprehensive base-year assessment (2025) and a seven-year forecast horizon (2026–2032), the study quantifies long-term growth and translates market dynamics into executable strategies. The market is estimated at USD 170.8 Million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 5.58% through the forecast period, reflecting structural demand in construction-related segments and selective industrial applications.

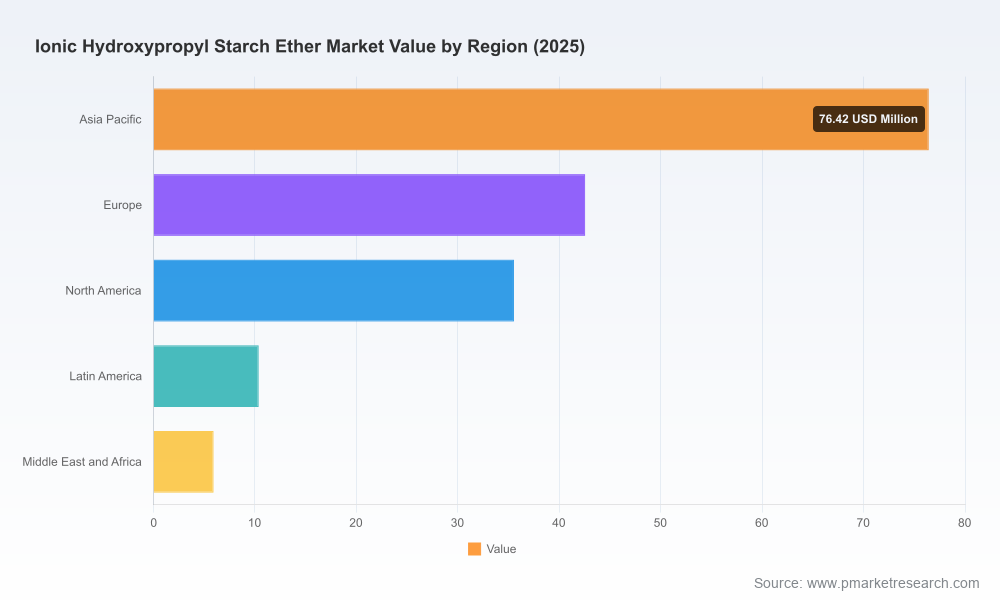

Worldwide Ionic Hydroxypropyl Starch Ether Market

Why 2026 Is a Pivotal Year for Strategic Choices

Two converging forces make 2026 a decision inflection point for firms exposed to ionic hydroxypropyl starch ether (HPS) markets. First, steady demand in construction-adjacent applications is creating predictable capacity needs that reward early, disciplined investments. Second, upstream exposure — to agricultural feedstocks and to propylene oxide based chemistry — is increasingly volatile, requiring new commercial and operational risk-management approaches. In this context, the PW Consulting report reframes market intelligence from descriptive to prescriptive: it highlights where to commit capital, where to pursue partnerships, and how to structure procurement to protect margins while maintaining responsive service levels.

Worldwide Ionic Hydroxypropyl Starch Ether Market

What the Report Delivers — Practical, Executable Insight

- Concise market sizing and scenario-based projections for 2026–2032, enabling finance teams to stress-test capex and revenue plans against realistic demand paths.

- Driver-and-restraint maps tying macro and micro trends (construction cycle, dry-mix formulations, cellulose-ether synergy) to price and volume outcomes.

- Supply-chain risk diagnostics focused on raw-material sensitivity (starch feedstocks, propylene oxide), energy and freight exposure, and supplier concentration.

- Vendor scorecards and a competitive playbook that assess product portfolios, manufacturing models, and route-to-market capabilities of the industry’s leading suppliers.

- Commercial templates and negotiation levers — term-sheet considerations, hedging structures, inventory buffers and contingency-service clauses tailored to HPS supply patterns.

- R&D and product strategy guidelines: formulation opportunities, co-development approaches with cellulose ethers, and regulatory-compliance checklists for chemical modification routes.

- Transaction and partnership decision matrices for M&A, joint ventures and distribution agreements — framed to identify assets that accelerate market access or integrate feedstock supply.

Market Dynamics That Matter for 2026 Planning

Three dynamics in particular should influence corporate plans for 2026:

Worldwide Ionic Hydroxypropyl Starch Ether Market

- Feedstock and input volatility. HPS production fundamentally depends on agricultural starches (corn, potato, tapioca) and the etherification step, which utilizes propylene oxide under alkaline conditions. Weather-driven crop yields, quality premiums for specific starches, and fluctuations in energy and freight costs all translate directly into input cost variability for processors. Procurement strategies that do not explicitly model this volatility will likely see squeeze on margins.

- Demand resilience tied to construction formulations. Ionic HPS is used as a rheology modifier, water retainer and workability enhancer in cement- and gypsum-based systems. Its performance synergy with cellulose ethers, and role in dry-mix mortars, sustain baseline demand even amid cyclical construction slowdowns. However, the pace and geography of product uptake vary by application and require localized go-to-market approaches.

- Moderate supplier concentration and competitive fragmentation. The market shows mid-level concentration — our analysis indicates that the top three players control just over a third of market share and the top five approach half the market. This structure creates opportunities for focused, regional competitors to defend niches, while larger suppliers can exert pricing and innovation leadership. For buyers, that means a mix of negotiating leverage and single-source risk to balance.

Competitive Landscape — Who Shapes the Market

Our vendor analysis profiles established starch processors, chemical-specialty producers and vertically integrated suppliers. Each brings distinct strengths for partners and competitors to evaluate:

- SLEO Chemical Technology Co., Ltd. (China) — Known for SLEO® SL-HPS, positioned as an ionic HPS tailored to gypsum and cement mortars. SLEO’s practical product framing emphasizes thickening, water retention and workability enhancement for tile adhesives, joint fillers and EIFS formulations.

- Kima Chemical (Zibo, Shandong, China) — A leading HPS manufacturer serving mortar applications with a range of grades; its breadth in product specifications makes it a go-to supplier for formulators seeking consistency across project types.

- AVEBE (Netherlands) — A starch-processor with established starch ether brands for building applications; its emphasis on synergy with cellulose ethers and product system thinking supports premium positioning in formulations that demand extended open time and sag resistance.

- AGRANA (Austria) — Offers hydroxypropyl derivatives from waxy maize and promotes sustainability credentials, giving it appeal with customers focused on bio-based inputs and traceable supply chains.

- EMSLAND-Stärke GmbH (Germany) — A recognized European producer with a strong presence in starch derivatives, well placed to serve regional construction and industrial markets.

- MATECEL / Shijiazhuang Henggu Jianxin Cellulose (China) — Focuses on mortar performance improvement; its technical orientation supports formulators seeking tailored rheology solutions.

- Regional specialists — Zhejiang Yisheng New Material, WOTAIchem, Kundu Chemicals and Meska Joinway (Cemotec JV) are examples of focused suppliers serving local dry-mix and adhesive value chains with competitive cost and ASI (after-sales/in-field) capabilities.

The competitive reality is that producers range from large starch-integrated groups to smaller specialty chemical houses. This spectrum creates a menu of potential partners for different strategic aims — scale, sustainability, technical differentiation, or local service intensity.

Strategic Playbook: Three Priority Moves for 2026

- Hedge and diversify feedstock exposure. Build a multi-source procurement plan that combines term contracts with variable-volume spot exposure. Consider strategic co-investment with starch suppliers or long-term offtake agreements that include penalty/bonus mechanisms tied to crop-quality metrics.

- Embed formulation differentiation into commercial strategy. Move beyond product-only selling. Offer system-level packages that combine ionic HPS with complementary cellulose ethers and application-support services (field trials, technical documentation, installer training). This preserves margin and builds stickiness.

- Invest in nimble manufacturing and logistics options. Small capacity additions targeted at high-growth applications can outperform large greenfield projects in payback. In parallel, deploy regional hubs to reduce freight exposure and improve lead times for construction-driven demand spikes.

M&A and Partnership Signals — Where Value is Likely to Be Created

We see three types of transactions that will create disproportionate value through 2032:

- Acquisitions that vertically integrate starch feedstocks with HPS processing to lock-in raw-material margins and reduce input volatility.

- Minority investments and JV structures with regional formulators or distribution networks to accelerate market entry and local technical support.

- Technology and IP partnerships that improve etherification yield, reduce propylene oxide usage, or enable bio-derived alternatives — all of which bolster sustainability positioning and mitigate regulatory risk.

How the PW Consulting Report Supports 2026 Decisions

Our study translates the macro forecast — market size as of 2025, growth trajectory through 2032 and structural concentration metrics — into operational and commercial actions. It includes ready-to-use deliverables (supplier scorecards, commercial term templates, cost-sensitivity models and scenario planning worksheets) that shorten the time from insight to implementation. Importantly, this brief serves as a trailer: the full report contains the granular, segment-level demand forecasts, regional uptake curves, and detailed vendor financial and technical benchmarking required to execute M&A diligence, negotiate long-term contracts, or prioritize capital projects.

Next Steps

For executives preparing budgets, procurement compacts, or M&A pipelines for 2026, the PW Consulting outlook provides a concise, action-oriented foundation. To access the complete dataset, including granular application and regional forecasts, detailed vendor profiles and downloadable commercial tools, please visit our report page on the PW Consulting website. The full intelligence package is designed to convert market knowledge into measurable business outcomes — faster, with less execution risk.

PW Consulting’s Worldwide Ionic Hydroxypropyl Starch Ether Market — 2026–2032 Strategic Outlook is intended to equip decision-makers with the insights and instruments they need to act decisively in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Worldwide Ionic Hydroxypropyl Starch Ether Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com