متى تظهر نتائج علاج هيدرا فيشل في الرياض

Health |

2026-07-13 09:41:31

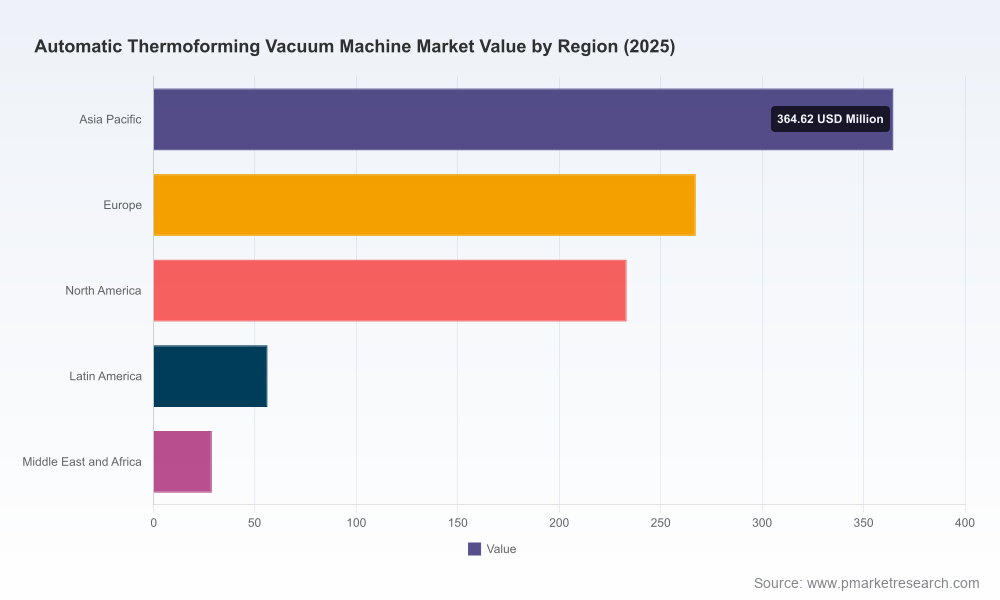

PW Consulting’s latest market research brief — the Worldwide Automatic Thermoforming Vacuum Machine Market report (base year 2025, forecast 2026–2032) — delivers a focused, decision-ready view for industrial equipment buyers, packaging OEMs, private equity sponsors, and plant operations leaders who must set investment priorities in 2026. Our topline market modelling shows steady expansion from a USD 950.0 Million market in 2025, growing at a compound annual growth rate (CAGR) of 5.4% through the forecast window. In practical terms, the global market is poised to breach the USD 1 billion threshold in 2026 and continues to expand into the early 2030s, reflecting the persistent conversion of manual packaging tasks to automated thermoforming vacuum lines and the premium placed on productivity, safety, and energy performance.

Worldwide Automatic Thermoforming Vacuum Machine Market

Immediate purchasing decisions carry multi-year implications. Capital deployed on thermoforming vacuum systems now will define production throughput, energy consumption, and regulatory compliance for the next decade. Our forecast and scenario modules translate macro trends into machine-level planning assumptions that materially affect payback and capacity planning.

Worldwide Automatic Thermoforming Vacuum Machine Market

Cost pressure and regulatory tightening are creating a new selection calculus. Material and component cost dynamics (notably increases in stainless steel and servo motor component costs) and evolving safety and energy rules are driving buyers to evaluate total cost of ownership (TCO) rather than headline machine price.

Worldwide Automatic Thermoforming Vacuum Machine Market

Supplier selection is becoming more strategic. With the top manufacturers capturing a meaningful—but not dominant—share of the market (our concentration metrics show the top three and top five suppliers controlling under majority thresholds), procurement teams must balance scale, innovation capability, and specialization when shortlisting partners.

Actionable market sizing and forward-looking scenarios: a base-case forecast plus sensitivity runs that stress-test demand under alternative macro, regulation, and cost scenarios.

Proprietary vendor benchmarking: scorecards covering throughput, modularity, automation level, energy footprint, spare-part lead-times, and documented service SLAs—designed to shorten vendor selection cycles.

CapEx and TCO playbooks: plant-level calculators that convert throughput needs into recommended line architectures (single-station, continuous, rotary and hybrid approaches), incorporating energy mandates and expected maintenance profiles.

Supply chain sensitivity analysis: component-level cost drivers, lead-time risk maps, and contract negotiation templates focused on long-lead items such as servo motors and precision tooling.

Compliance and certification checklists: practical steps for meeting current EU machinery directives and ISO-based energy management expectations for new installations.

M&A and partnership playbooks: target screening filters, diligence checklists, and integration risk matrices for firms considering consolidation or capability acquisition in the thermoforming vacuum space.

The market is characterized by several established equipment manufacturers with differentiated value propositions. Our qualitative and quantitative vendor review synthesizes recent product roadmaps and commercial moves to identify where competitive advantage is forming:

Multivac Group (Germany) — a global leader with a broad portfolio of high-speed R-series thermoformers and an early adopter of AI-enabled controls. Their public demonstrations in 2024 highlighted intelligent asset management and predictive diagnostics as differentiators for high-throughput food and medical packaging lines.

ULMA Packaging (Spain) — known for robust, fully automatic TF-series lines and inline printing integrations, ULMA’s trade show reveals emphasize active-roller configurations optimized for flexible packaging formats common in retail and fresh food segments.

ILLIG Maschinenbau (Germany) — continues to invest in productivity gains; its recent product introductions focus on bidirectional forming and vacuum efficiency improvements for medium-to-high volume operations.

Kiefel GmbH (Germany) — leverages servo-driven Speedformer platforms for medical and tray applications where precision, repeatability, and regulatory traceability are paramount.

Henkovac and Audion Elektro (Netherlands) and Italian OEMs such as Orved, Minipack-Torre and G.M.S. — these vendors occupy niches from modular fresh-food lines to compact systems for short runs, enabling customers to select based on SKU mix and floor space constraints.

North American specialists like SencorpWhite focus on custom thermoforming for regulated medical device packaging, emphasizing cleanroom compatibility and validation support.

Collectively these suppliers create a competitive topology where the top three firms capture an influential share of market activity (CR3 ~32.4%), while the top five widen reach but still leave meaningful room for specialist vendors and regional integrators (CR5 ~48.15%). For buyers, that means access to both scale and niche innovation—if they build procurement strategies that reflect performance needs, not only brand recognition.

Labor and automation adoption. Structural labor shortages in food processing (documented as a material shortfall in 2025) are accelerating demand for automated thermoforming lines that reduce dependence on manual packing and enable night-shift consolidation.

Raw material and component volatility. Stainless steel frame costs rose noticeably year-over-year amid supply-chain disruptions; similarly, servo motor pricing has been pressured by semiconductor shortages. These shifts increase upfront equipment costs and emphasize negotiating component supply or choosing designs tolerant of component substitution.

Regulatory and energy mandates. The EU’s machinery safety expectations and the rising adoption of ISO 50001-style energy management drive buyers to prefer machines with certified interlocks, lower vacuum cycle energy demands, and real-time energy reporting.

Technology convergence. Machine vendors are increasingly bundling AI-enabled predictive maintenance, inline vision, and advanced sealing controls. Early adopters report higher uptime and lower scrap rates—key metrics for justifying premium equipment.

Buyers: Shift procurement criteria to TCO and regulatory fit. Include energy certification and spare-part availability as pass/fail filters. Require vendors to demonstrate predictive maintenance capabilities and provide performance data from comparable installations.

Manufacturers: Prioritize modular platforms that accommodate both high-speed continuous and compact, single-station use cases. Strengthen supply chain transparency—locking in long-lead components under multi-year agreements can be a differentiator.

Investors: Use vendor scorecards and scenario forecasts in this report to stress-test acquisition targets against commodity shocks and regulatory shifts. Fragmentation creates roll-up opportunities, but integration hurdles around service networks and spare parts are significant.

Operations leaders: Pilot energy recovery and vacuum optimization modules on a controlled line before plant-wide roll-outs; small percentage improvements in cycle energy translate into multi-year savings given typical usage profiles.

Our engagement model pairs the published report’s quantitative assets (forecasts, vendor indices, scenario models) with tailored advisory deliverables: site-level TCO modeling, vendor selection workshops, supply chain hedging strategies, and M&A diligence support. For clients preparing CapEx cycles in 2026, we deliver implementation roadmaps that align manufacturing KPI targets with procurement timelines and warranty terms—reducing the risk that an ostensibly low-cost line becomes a long-term drag on productivity.

This briefing intentionally omits the exhaustive segmentation tables, regional and application-specific percentage breakdowns, and full vendor scorecards that are included in the complete report. Those proprietary elements—detailed by type, application, and geography, along with downloadable financial models and negotiation playbooks—are reserved for subscribers and clients who require the deep, actionable granularity necessary to finalize 2026 investment mandates.

To request the full report, interactive forecast models, or a briefing with our industry team, please visit PW Consulting’s report page or contact our lead industry analyst. Our team will help you translate the macro trajectory and supplier dynamics described here into a stepwise procurement or investment plan tailored to your operating context.

For detailed analysis of this topic, please visit the official page:Worldwide Automatic Thermoforming Vacuum Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com