Worldwide Needle Bearings Market: Strategic Imperatives for 2026 — PW Consulting Announces Comprehensive Industry Outlook

PW Consulting today releases its authoritative briefing derived from the Worldwide Needle Bearings Market research — a tactical roadmap designed for executives, procurement leaders, product strategists, and M&A teams who must make high-consequence decisions in 2026. The needle bearings ecosystem is transforming at the intersection of electrification, industrial automation, and materials volatility. Our new analysis quantifies the scale of that transformation and translates it into actionable guidance without giving away the proprietary segment-level intelligence reserved for the full report.

Worldwide Needle Bearings Market

Market trajectory — what the headline numbers tell you

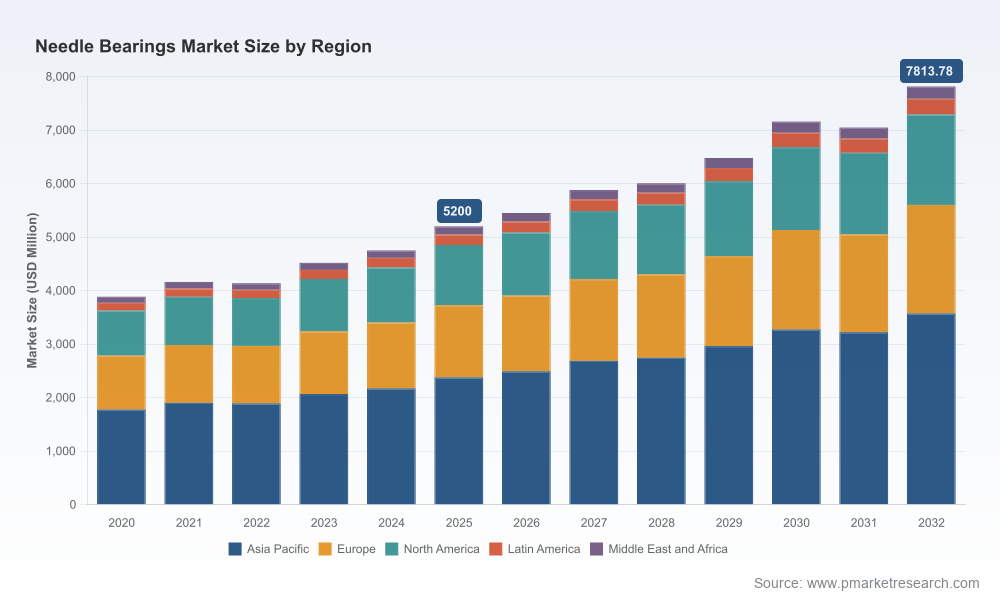

The global needle bearings market has grown from an estimated USD 3,885.5 Million in 2020 to an observed USD 5,200.0 Million in the report base year of 2025. Our forecast shows continued expansion through the 2026–2032 planning window, with the market reaching an estimated USD 5,449.94 Million in 2026 and a projected USD 7,813.78 Million by 2032. The compound annual growth rate for the forecast period is 5.99% (USD Million basis).

Worldwide Needle Bearings Market

These topline figures mask important structural shifts: demand is increasingly driven by compact, high-load applications such as e-mobility powertrains and precision industrial automation; meanwhile, manufacturing and raw material dynamics are compressing margins for select product formats. The market’s concentration profile is informative for competitive strategy — the three largest firms together control a meaningful portion of supply, and the five largest firms expand that control further, underscoring both opportunity and risk for new entrants and Tier-2 suppliers.

Worldwide Needle Bearings Market

Why this matters for 2026 decisions

- Procurement and supply continuity: Raw material volatility — notably in bearing steel inputs — is already influencing price and lead-time dynamics. Buyers who postpone hedging and supplier diversification decisions risk exposure to sudden cost inflations and plant-level disruptions.

- Product development prioritization: The rise of compact e-axle architectures and higher integration in industrial actuators prioritizes needle bearing formats optimized for axial space and contamination resilience. OEM roadmaps that do not align bearing selection to these constraints risk late-stage redesigns.

- M&A and partnership timing: The market is moderately consolidated; strategic acquisitions, minority stakes, and joint ventures remain effective routes to broaden product portfolios and secure capacity without the multi-year lead time of greenfield plants.

- Cost-to-serve optimization: Geographic footprint, tooling intensity, and assembly vs. component sourcing materially affect total landed cost. 2026 capex allocations should be informed by a granular factory-level view of cost drivers and scale economics.

Practical contents of the PW Consulting report — what you get

We designed this research as an operational toolkit for decision-makers. Highlights of the report’s deliverables include:

- Top-down and bottom-up demand models: Integrated forecasts across the 2026–2032 horizon, reconciled against historical production and trade flows, with scenario runs for upside and downside macrodrivers.

- Supplier matrix and capability maps: Proprietary scoring of manufacturers against technology, capacity, global footprint, and aftermarket support — enabling fast identification of strategic partners and potential acquisition targets.

- Supply chain heatmap and risk register: Node-level analysis of critical raw material exposure (bearing steel and alloy inputs), single-source dependencies, and logistics choke points plus mitigation playbooks.

- Cost-model templates: Adjustable cost-to-manufacture models that allow teams to stress-test outcomes under raw material pricing swings, labor scenarios, and regional energy-cost differentials.

- Product roadmaps and engineering guidance: Comparative guidance on drawn-cup, machined ring, and needle-cage assemblies relative to durability, space constraints, and assembly economics — presented as decision matrices rather than prescriptive prescriptions.

- Commercial strategy tools: Channel segmentation, pricing levers, win-loss analysis, and GTM frameworks tailored for OEMs, Tier-1 integrators, and aftermarket distributors.

- M&A playbook and valuation benchmarks: Deal-screening filters, synergy checklists, and scenario-based valuations to support bid/no-bid decisions in a market where scale and specialized IP carry premium multiples.

We intentionally anchor these deliverables to a “tell, don’t show” approach in this public briefing — demonstrating methodology and insight while protecting the granular segment-level numbers that provide competitive advantage. The full dataset and appendices are accessible via the report portal for licensed clients.

Competitive landscape: strengths, gaps, and what to watch

The global supplier community combines legacy scale players with specialist manufacturers. Leading multinational bearing groups maintain wide product portfolios and global manufacturing footprints; regional champions and niche precision houses supply high-volume or high-precision applications respectively. Strategic takeaways for 2026:

- Global integrators (e.g., Schaeffler, SKF, NTN, NSK, Timken): These firms leverage deep product engineering and broad channel access to win system-level OEM engagements. Their strengths include engineering depth, large-scale manufacturing, and integrated aftermarket networks. Watch for incremental investments in e-mobility-specific variants and higher service integration.

- Regional champions and specialists (e.g., JTEKT/Koyo, NRB, Universal Bearings, NOSE SEIKO, Hartford Technologies): These providers are strong where lightweight designs, cost competitiveness, or custom engineering are prioritized. Their agility makes them attractive partners for Tier-1s and OEMs pursuing differentiated cost or form-factor targets.

- Emerging tier dynamics: Consolidation moves, such as strategic restructuring in EMEA operations by major suppliers, reflect attempts to rationalize capacity and align product portfolios to EV and automation demand. Event participation and trade-show activity in 2026 also suggests that manufacturers are accelerating commercialization of new machining and assembly technologies.

Raw materials, regulation and macro trends — the near-term operating environment

Three non-technical factors will shape supplier and buyer strategies in 2026:

- Bearing steel and input costs: The bearing steel market is subject to structural growth and periodic volatility. Market estimates point to a multi-year expansion in the broader bearing-steel sector, and recent upward movement in global steel prices (notably hot-rolled coil in Europe and North America) has immediate pass-through implications for bearing manufacturers’ margins.

- Regulatory and application-driven design shifts: Electrified powertrains and tighter emissions/regulatory frameworks mean needle bearings must adapt to higher rotational speeds, contamination-resistant seals, and integration with e-axle modules. Suppliers who can demonstrate durability under these conditions command higher commercial leverage.

- Automation and precision demand: Industrial automation and advanced consumer devices are increasing demand for compact, high-load rolling elements, pushing manufacturers to optimize tolerances, surface treatments, and cage technologies.

Recommended 90–180 day actions for executives

For organizations making 2026 plans, our research suggests a prioritized sequence of actions:

- Immediate (0–90 days): Initiate supplier stress tests that simulate raw material price shocks and lead-time disruptions; review existing long-term purchase agreements for renegotiation opportunities; and commission targeted lab trials for e-axle bearing endurance under contaminant ingress scenarios.

- Near term (90–180 days): Accelerate strategic sourcing toward dual-sourced architectures for critical formats; explore capacity-sharing or JV options with regional specialists to de-risk single-node manufacturing; and integrate the report’s cost-model templates into capital planning cycles.

- Board-level (180 days+): Assess M&A targets using the PW Consulting deal filters; reweight R&D budgets toward contamination-mitigation and surface-engineering capabilities; and adjust market-entry strategies for regions where industrial automation growth outpaces local manufacturing capacity.

How PW Consulting’s report supports your 2026 playbook

Executives use our work to compress time-to-decision and to validate hypotheses with quantitative rigor. This briefing has surfaced the principal implications of market scale, growth trajectory (5.99% CAGR through the forecast window), and competitive dynamics. The full report contains the underlying datasets, factory- and SKU-level cost models, supplier due-diligence dossiers, and scenario outputs that allow organizations to move from strategic intent to executable programs.

For procurement leaders, product strategists, and deal teams preparing for 2026, the difference between reactive and proactive posture will be decided by access to the nuanced, validated data and playbooks contained in the full PW Consulting report. Our team is available to deliver executive briefings, tailored workshops, and custom due-diligence workstreams to translate these insights into implementable plans.

Next steps

- Request a confidential executive briefing to review the scenario outputs most relevant to your business.

- Commission a tailored supplier assessment or regional market entry analysis based on the PW Consulting templates.

- Access the full dataset and appendices through the PW Consulting report portal for licensed clients to obtain the granular intelligence needed for procurement, engineering, and M&A workflows.

PW Consulting’s Worldwide Needle Bearings Market report equips leaders with the clarity required to navigate 2026 — revealing where to invest, where to defend, and where to partner. For a market that is expanding from approximately USD 3.9 billion in 2020 to an expected USD 7.8+ billion by 2032, the strategic choices made this year will determine competitiveness for the next decade.

For detailed analysis of this topic, please visit the official page:Worldwide Needle Bearings Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com