Choosing the Right IPO Consultant: A Complete Guide for Successful IPO Planning (2026)

Other |

2026-07-01 05:56:44

PW Consulting’s latest market study on the Worldwide Automotive Racing Slicks Market delivers an actionable intelligence package built for executive decision cycles in 2026. The research synthesizes historical performance (2020–2025), a detailed base-year benchmarking at 2025, and scenario-informed forecasts through 2032. At the macro level, the global market has expanded from roughly USD 845 million in 2020 to about USD 1.21 billion in 2025 and is projected to approach USD 1.94 billion by 2032, tracking at a compound annual growth rate of approximately 7.02%. These headline dynamics create both runway and risk for manufacturers, series organizers, teams, suppliers, and investors — our report distills what those parties must prioritize this year.

Worldwide Automotive Racing Slicks Market

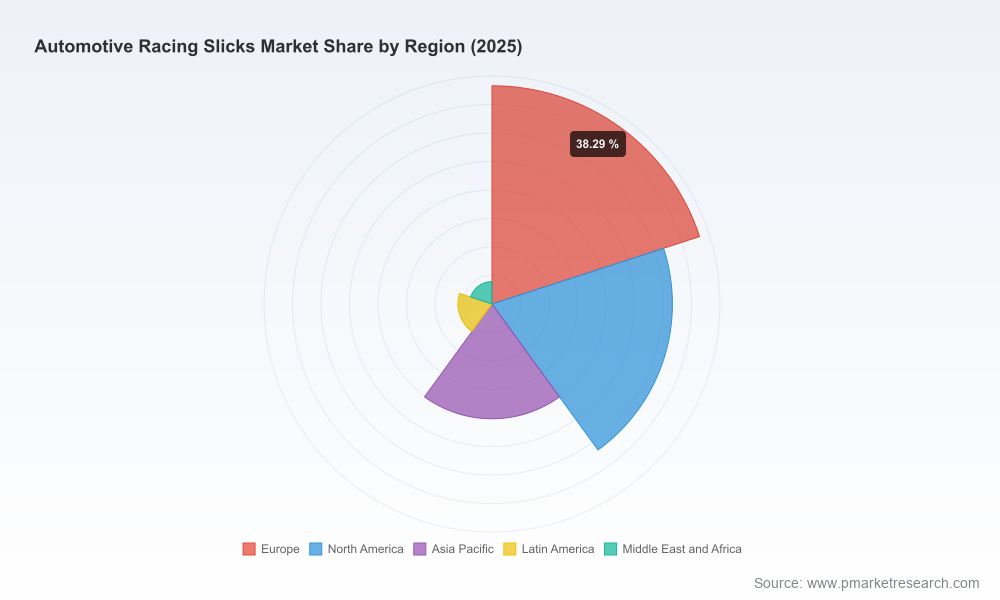

The racing slicks market is in a phase of steady, structurally supported growth. After a post‑pandemic rebound through 2023–2025, the forecast period shows sustained expansion driven by increased professional series activity, growth in grassroots and track-day participation, and a rise in spec-series programs that favor single-supplier arrangements. Market concentration is material: the top three suppliers account for a strong majority of market share, and the top five consolidate an even larger portion, indicating that scale and motorsport legacy remain decisive competitive advantages.

Worldwide Automotive Racing Slicks Market

Two forces stand out. First, demand-side segmentation is maturing — different racing formats (from premier endurance to club-level sprint series and consumer track-day use) each impose distinct performance, warranty and logistics demands. Second, supply-side economics are being reshaped by raw-material cost volatility (natural and synthetic rubbers, carbon black) and by an emergent sustainability imperative that touches product design, manufacturing inputs and procurement sourcing. The combination strengthens incumbents with deep R&D and production footprints, while opening pockets of opportunity for nimble challengers who can manage cost and sustainability commitments simultaneously.

Worldwide Automotive Racing Slicks Market

Several recent strategic developments illustrate the competitive choreography for 2026: a major supplier was nominated as the official tire provider for a high-visibility one-make series starting in 2026; another renewed multi-year supply for an established sprint challenge; a prominent manufacturer launched a new radial slick product line aimed at junior single-seater categories; and a regional supplier committed continued support for an electric single‑class competition, underscoring the sector’s breadth of technical and commercial agendas. These vendor moves serve as live templates for how series operators and suppliers will negotiate exclusivity, technical support, and product evolution through 2026.

PW Consulting’s study was designed to be operational from day one. Key deliverables include:

To preserve the competitive value of the dataset and to guide commercial engagement, the report presents the full regional and application splits, unit pricing curves, and underlying financial tables on the source landing page. PW Consulting’s benchmarking datasets and spreadsheets are available under license.

For executives planning capex, product launches, series tendering, or M&A in 2026, the report highlights five immediate strategic priorities:

2026 is a year where tactical supplier decisions will have multi-year operational impacts. Series nominations announced and product launches completed now will shape supply commitments, inventory strategies, and R&D roadmaps for the remainder of the decade. With a market growing at roughly 7% annually and clear concentration among top suppliers, time-sensitive actions — from negotiating supply contracts to accelerating sustainable compound validation — will determine competitive positions.

PW Consulting’s report is intentionally structured to support those actions. We provide the synthesis and the instruments to operationalize strategy: scenario models, negotiation playbooks, cost templates and a supplier scorecard calibrated to motorsport imperatives. For practitioners who need immediate, executable insights, the study supplies both the “why” and the “how.”

To access the complete set of regional and application-level breakdowns, the full dataset, and licensing options for our benchmarking spreadsheets, visit the PW Consulting report page. The publicly available executive summary outlines principal findings; the full report grants you the tables, models and supplier-level benchmarking needed to translate insight into 2026 decisions.

Contact PW Consulting to schedule a tailored briefing where we will walk clients through the forecast scenarios, run a bespoke cost-sensitivity analysis for your supply chain, and outline a prioritized action plan customized to your strategic objectives.

For detailed analysis of this topic, please visit the official page:Worldwide Automotive Racing Slicks Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com