Sleep Masks Market Growth Outlook Ahead

Other |

2026-06-24 09:32:04

PW Consulting’s new market research brief on Worldwide Veterinary API Manufacturing provides a forward‑looking intelligence package designed to inform C‑suite decisions for 2026 and beyond. Anchored in a rigorous 2020–2025 historical base and a 2026–2032 forecast horizon, the study projects the global veterinary API manufacturing market growing at a compound annual growth rate (CAGR) of 7.15%. Total market value expands materially from the mid‑2020s base to reach mid‑to‑high‑four‑digit USD millions by the end of the forecast.

Worldwide Veterinary API Manufacturing Market

This release outlines the report’s strategic value, summarizes market dynamics that will affect sourcing, manufacturing and M&A choices in 2026, and highlights the competitive posture of incumbent and emerging suppliers. In the spirit of a strategic “trailer,” we showcase the depth of our analysis while deliberately reserving granular regional and product split tables for the full report—accessible via PW Consulting’s report portal.

Worldwide Veterinary API Manufacturing Market

Growing, resilient end‑market: Demand drivers across livestock and companion animal care are sustaining investment into veterinary APIs, with steady expansion expected through the forecast period. The market’s mid‑term trajectory provides both volume and margin opportunities for suppliers who align capacity, quality and regulatory readiness.

Worldwide Veterinary API Manufacturing Market

Supply chain concentration and geopolitical risk: Sourcing patterns and tariff actions have increased landed costs and supply volatility for finished products. Strategic procurement and diversified supplier networks will be decisive for companies seeking to avoid production interruptions.

Regulatory complexity and antimicrobial stewardship: Evolving standards on residues, exports and antimicrobial use force manufacturers to rework formulations, documentation and monitoring systems—creating winners among firms that can demonstrate compliant, auditable supply chains.

Our base‑year analysis (2025) establishes a clear inflection: the market has expanded significantly since 2020 and is forecast to continue growing at a robust 7.15% CAGR through 2032. This translates into a meaningful increase in absolute market value over the next six years—creating capacity utilization challenges for OEMs and opportunities for contract manufacturers and CDMOs that can deliver quality, speed and regulatory assurance. The report includes detailed scenario variants that isolate outcomes under differing demand, trade and regulatory conditions.

Concentration versus fragmentation: The veterinary API landscape shows a middle‑ground concentration profile—large, integrated animal health players co‑exist with specialist API producers and regionally dominant contractors. For buyers, this implies both bargaining options and points of single‑source vulnerability.

Geopolitical and trade pressures: A significant share of veterinary API supply for key markets originates from Asian manufacturing hubs. Trade measures and shipment disruptions materially affect landed costs and inventory strategies; nearshoring and dual‑sourcing are no longer tactical choices but strategic imperatives.

Regulatory enforcement and quality expectations: Regulatory agencies are intensifying supply‑chain oversight, particularly around antimicrobials and residues. Companies must invest in compliance infrastructure (audit trails, analytical capabilities, GMP documentation) or face market access constraints.

Technology and platform shifts: Advances in biomanufacturing, synthetic biology and nucleic acid‑based platforms are beginning to appear in animal health—creating pathways for faster vaccine and biological API development. Early movers that master platform scale‑up will capture margin premium in growing biological API segments.

Raw material and logistics friction: Ongoing raw‑material bottlenecks and global logistics unpredictability increase working‑capital needs and drive demand for strategic safety stocks and supplier financing solutions.

The market features a balanced set of players: global integrated animal health leaders; specialist European and Asian API producers; and emerging CDMOs expanding veterinary‑dedicated capacity. Our analysis of named industry participants reveals differentiated strategies:

Large integrated animal health companies (e.g., Zoetis, Elanco, Merck Animal Health, Boehringer Ingelheim) leverage combined R&D, in‑house API capabilities and global distribution to protect margins and ensure supply continuity for priority therapies. Their advantage lies in vertical integration, scale GMP infrastructure and ability to internalize regulatory risk.

Specialist API manufacturers (e.g., SUANFARMA, Huvepharma, Ofichem) and regional producers focus on supply reliability for core anti‑infectives and antiparasitics. Their competitive edge is cost‑competitive manufacturing and specialization in veterinary formulations.

India‑based producers and CDMOs (e.g., Sequent Scientific/Alivira, Sai Life Sciences, Chempro) are rapidly expanding capacity and service breadth, positioning themselves as global contract partners for companies seeking scale and cost efficiency. Recent capacity additions illustrate this pivot toward dedicated veterinary manufacturing.

Specialty and hybrid players exploit technology partnerships (for example, access to novel nucleic acid platforms) to move up the value chain—from commodity APIs to advanced biologicals and vaccine components.

Recent market moves illustrate these dynamics in real time: a CDMO’s commissioning of a dedicated veterinary API unit to increase capacity and compliance; a major animal health firm acquiring a contract manufacturing site to secure production continuity; and a technology licensing partnership enabling new biological development paths across animal health. Each development underscores the central strategic levers of capacity, partnership and platform access.

For executives and functional leaders making 2026 choices, the report offers pragmatic tools and actionable intelligence, including:

A bottoms‑up market model (2020–2032) with scenario toggles for demand shocks, trade disruptions and regulatory tightening.

Supply‑chain heatmaps and vulnerability indices identifying single‑point risks and strategic sourcing priorities (with supplier scorecards and audit readiness matrices).

Regulatory playbooks mapping approval, residue and export compliance across major jurisdictions—plus an antimicrobial stewardship risk matrix for portfolio managers.

CDMO selection and due‑diligence toolkit, with operational KPIs and sample contractual terms tailored to veterinary API engagements.

CapEx and capacity optimization models calibrated to utilization scenarios and lead‑time sensitivity analyses.

M&A and partnership navigator: target archetypes, valuation drivers and integration checklists for acquiring or partnering with API manufacturers or CDMOs.

Commercial pricing sensitivity models and route‑to‑market considerations for finished‑dosage manufacturers dependent on API cost pass‑throughs.

Prioritize supply‑chain resilience. Implement dual‑sourcing for critical APIs, introduce dynamic safety stocks, and stress‑test contract manufacturers for regulatory continuity.

Invest selectively in compliance and traceability. Regulatory readiness is a market access enabler—capabilities in analytics and documentation pay off quickly under heightened enforcement.

Accelerate partnerships with capable CDMOs. For companies preferring variable cost models, vetted CDMOs with veterinary‑dedicated capacity offer a fast path to scale without large upfront capex.

Make technology scouting part of the strategic plan. Early screening of biological/biotech platforms can create first‑mover advantages in emerging therapeutic classes.

Use M&A and minority equity to secure supply. Buying capacity or taking strategic stakes in regional producers reduces commercial risk and can be structured to de‑risk integration.

Our report is designed for operational planners and corporate strategists alike. It couples quantitative forecasting with line‑level implementation tools—procurement playbooks, contract templates, supplier audit checklists, capex calculators and M&A readiness assessments—so teams can move directly from insight to action. We also provide encrypted data appendices and scenario model files to integrate into client planning systems.

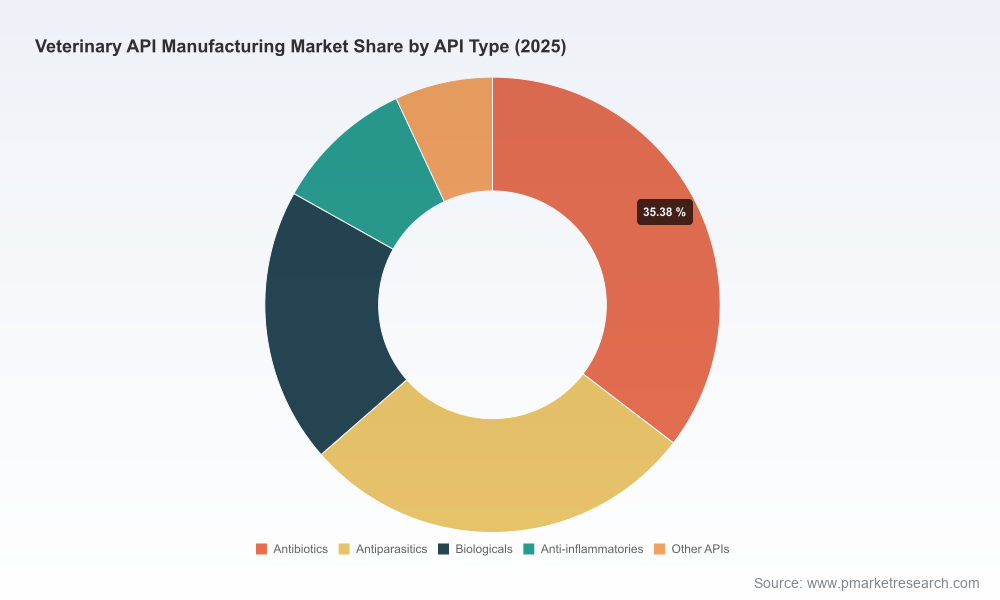

This communication intentionally highlights the strategic contours and decision levers without publishing the granular regional and API‑type splits, supplier market shares, or raw transaction tables that underpin our modeling. Those core subsegment datasets, detailed supplier heatmaps and downloadable modeling templates are available exclusively in the full PW Consulting report and the report’s data appendices on our report portal.

For procurement leaders, product heads, investors and M&A teams preparing 2026 playbooks, this report converts market intelligence into executable options—identifying which investments and partnerships will protect supply, capture growth and deliver regulatory‑robust portfolios in an evolving veterinary API landscape.

For detailed analysis of this topic, please visit the official page:Worldwide Veterinary API Manufacturing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com