Market Trends Powering the Future of Bioresorbable Coronary Scaffolds

Health |

2026-05-29 12:26:54

PW Consulting’s new market study on Worldwide Small-Size Flexible OLED Panels provides a practice-focused view for corporate strategists, product leaders, investors and OEM procurement teams making pivotal choices in 2026. Our base year is 2025 (historical window 2020–2025) and the forecast window runs 2026–2032. The market has expanded rapidly from an evaluated USD 22,500 Million in 2020 to USD 40,550 Million in 2025; our central forecast projects a continuation of this expansion at a compound annual growth rate (CAGR) of 8.31% across 2026–2032, with total market value approaching USD 70,900 Million by 2032. All values in this release are presented in USD Million.

Worldwide Small Size Flexible OLED Panel Market

Capital allocation and capacity timing — panelmakers and investors face a narrow window to sequence Gen‑6/Gen‑8 investments against demand cycles for foldable and premium smartphone programmes.

Worldwide Small Size Flexible OLED Panel Market

Supplier selection and risk mitigation — OEMs must balance cost, lead time and technology risk (crease reduction, LTPO backplanes, PI substrate supply) when locking multi‑year contracts.

Worldwide Small Size Flexible OLED Panel Market

Product portfolio and ASP strategy — device OEMs need rigorous scenarios to decide whether to accelerate foldable device programs, extend flexible displays into mid‑price tiers, or focus on wearables and automotive niches.

M&A and partnership playbooks — consolidation and strategic alliances remain a fast route to secure capacity and IP; the market’s concentrated supplier base means M&A can yield outsized control over supply chains.

This study is built as a hands‑on toolkit for 2026 execution. Highlights include:

Top‑down market model (2020–2032) with downloadable Excel: revenue and unit scenarios, ASP trajectories, sensitivity levers and a clearly annotated assumptions tab for auditability.

Three scenario pathways (conservative, base, aggressive) to stress‑test capex decisions, supplier commitments and SKU roadmaps under varying demand, price and geopolitical outcomes.

Supplier scorecards and comparative TCO (total cost of ownership) for panel procurement — covering technology maturity, yield curves, capacity phasing, IP exposure and commercial flexibility.

Manufacturing cost model and margin waterfall by substrate/backplane choice (polyimide vs ultra‑thin glass/hybrids; LTPO vs conventional backplanes) to inform design‑for‑cost decisions.

Patent and standards landscape with infringement heatmaps and defensive IP strategies for panelmakers and OEMs.

Supply‑chain stress tests (raw material shocks, substrate shortages, capacity outages) and recommended contractual clauses to limit margin and delivery risk.

Go‑to‑market and commercialization playbooks for panelmakers entering wearable, foldable, and automotive segments, including pricing cadence, launch sequencing and reference‑design strategies.

M&A diligence checklist and model templates for accretion/dilution and synergy capture specific to the flexible OLED value chain.

The small‑size flexible OLED panel market is a high‑barrier, highly concentrated sector. Our concentration analysis shows the top three suppliers account for over 80% of market share (CR3 ≈ 82.4%) and the top five exceed 90% (CR5 ≈ 91.5%). That structural reality amplifies strategic importance for any supplier decision or partnership negotiation in 2026.

Samsung Display (SDC) (South Korea, https://www.samsungdisplay.com) — Market leader for small‑to‑medium flexible AMOLEDs, with strengths in foldables, crease mitigation technologies and scale production. Recent capacity announcements indicate continued emphasis on the foldable roadmap.

LG Display (LGD) (South Korea, https://www.lgdisplay.com) — Strong in polymer OLED (P‑OLED) for smartphones, wearables and nascent automotive designs. LGD’s high‑volume flexible runs and supply relationships position it as a preferred partner for several global OEMs.

BOE Technology Group (China, https://www.boe.com) — Rapidly scaling Chinese player with multiple Gen‑6 flexible lines and improving crease technologies. BOE’s shipments and aggressive fab rollouts are reshaping supplier options for smartphone OEMs.

Tianma, Visionox, CSOT / TCL CSOT, Everdisplay Optronics (EDO), Truly Semiconductors, and Futaba Corporation — Regional specialists and niche innovators that together provide capacity depth, localized supply options and specialized product variants for wearables and consumer devices.

BOE unveiled the “Mirror‑sense 0‑Crease” (Glaze Fold) technology at MWC 2026, demonstrating significant crease reduction and signalling improved competitiveness in foldable supply chains.

Samsung Display announced incremental investment to expand its A4 factory starting Q2 2026 to increase flexible/foldable capacity — a move that will influence slot availability for tier‑1 OEMs.

BOE’s first LTPO OLED prototype from its Gen 8.6 (B16) fab marks a diversification into larger and higher‑value flexible applications, including notebooks and advanced displays.

Supply volume updates through 2025 showed substantial flexible AMOLED shipments across China‑based fabs; however, market commentary and corporate updates indicate moderated growth into 2026 with price normalization expected in H2 2026.

Raw materials and substrate supply — polyimide and specialty barrier films remain critical constraints. Manufacturers should bake in multi‑tier sourcing and long‑lead purchase agreements for H2 2026 ramp plans.

Yield and technology risk — LTPO backplanes and Gen‑6 yield maturation are primary drivers of per‑unit economics. Investment timing must be coordinated with demonstrable yield curves, not just fab availability.

Pricing and ASP pressure — BOE and others have signalled downward pricing pressure expected in H1 2026 with stabilization later in the year. Procurement teams should design flexible pricing clauses and volume‑linked rebates to capture upside while limiting downside.

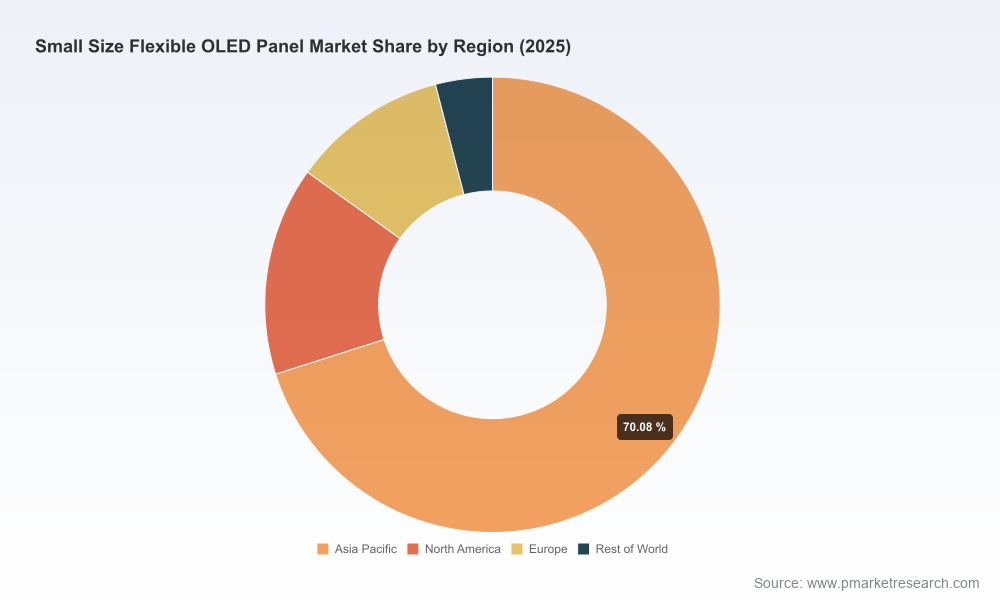

Geopolitics and trade concentration — the Asia Pacific cluster (notably South Korea and China) dominates production and upstream supply. Corporates should prepare contingency plans for supply‑chain disruptions and compliance costs tied to trade policy shifts.

Standards and IP — ongoing industry focus on crease mitigation, lifetime, and automotive qualification standards means product certification cycles can be lengthy; factor certification timelines into commercial launch plans.

Accelerate supplier audits and secure capacity options now — leverage staged commitments with clear performance milestones tied to yield and quality KPIs.

Adopt dual‑sourcing for critical substrates and componentry to reduce single‑point failure risk; negotiate exclusivity windows only where strategic premium is justified.

Defer full‑scale Gen‑6/Gen‑8 capex until validated yield improvements are demonstrated; prefer earn‑out and JV structures where possible to share execution risk.

Embed pricing hedges and adjustment clauses in long‑term supply contracts to manage anticipated ASP volatility through H1 2026 and stabilization thereafter.

Prioritize investments in crease‑reduction and LTPO capabilities for products where margin and differentiation justify cost; for mass‑market models, evaluate ultra‑thin glass and hybrid approaches to balance cost and reliability.

For investors: focus due diligence on operational metrics (yield by fab, equipment utilisation, and substrate supply contracts) rather than headline shipment numbers alone.

OEM product strategy: use scenario modelling to decide whether to accelerate foldable rollouts or to adopt a tiered flexible strategy across flagship and mid‑tier portfolios.

This article is a strategic preview designed to surface the most consequential levers and risks for 2026 planning. It intentionally omits granular subsegment breakdowns and detailed tables that are included in the full PW Consulting report and the accompanying Excel model. If your 2026 decisions require supplier‑level negotiation data, indexed cost models, or the full matrix of application and regional forecasts, the complete dataset and analyst support package will be available through PW Consulting.

For procurement teams, corporate development groups, and C‑suite leaders preparing budgets and partner negotiations for 2026, the full report delivers the exact numbers, scenario outputs and playbooks you will need to act with conviction.

Contact PW Consulting for access to the full report, the downloadable forecast model, and bespoke advisory services to translate findings into an executable 90‑day plan.

Book a workshop with our industry practice to run your specific supplier scenarios or M&A diligence in a two‑day session with senior analysts and manufacturing experts.

PW Consulting’s Worldwide Small‑Size Flexible OLED Panel Market study is structured to convert market intelligence into decisions — not just charts. For executives who must commit capital, choose partners, or set product strategy in 2026, the difference between acting on high‑quality foresight and reacting to events will be measured in market share and margin. Our report provides the operating details that underpin that foresight.

For detailed analysis of this topic, please visit the official page:Worldwide Small Size Flexible OLED Panel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com