Ultrasound Probe Market Research Report: Industry Size, Share, Dynamic Trends, and Forecast by 2030

Other |

2026-06-02 10:02:39

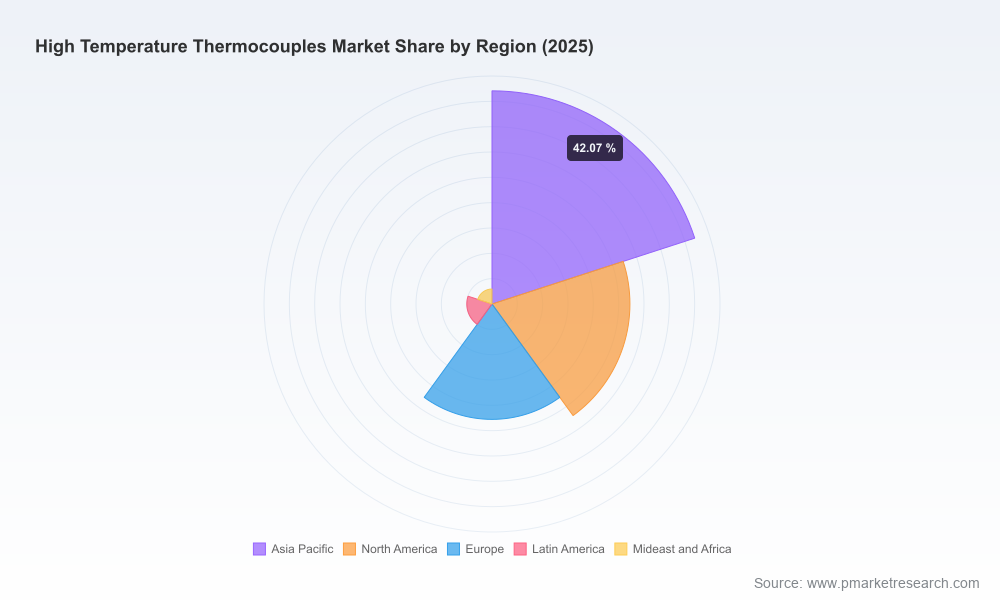

The worldwide market for high temperature thermocouples stands at an important inflection point as companies plan budgets and strategic moves for 2026. Our latest PW Consulting analysis shows the market reached USD 582.45 Million in 2025 and, under the central forecast scenario, is expected to expand to approximately USD 829.45 Million by 2032, representing a compound annual growth rate (CAGR) of about 5.17% across the 2026–2032 forecast window. That trajectory reflects steady, demand-driven expansion rather than explosive disruption — a signal for buyers, suppliers and investors to prioritize operational resilience, incremental technology differentiation, and supply-chain discipline.

Worldwide High Temperature Thermocouples Market

Timing: 2026 is the first full planning year after the dataset cut (base year 2025) and is when many capital and procurement cycles restart; our report translates the latest market dynamics into concrete procurement, R&D and M&A decision levers.

Worldwide High Temperature Thermocouples Market

Clarity: We combine market-level sizing and multi-year forecasts with scenario analysis and supply-side diagnostics so executives can convert a 5% CAGR baseline into dollar-implications across product lines and geographies.

Worldwide High Temperature Thermocouples Market

Risk-adjusted playbook: The report prioritizes actions to mitigate raw-material and certification risks that disproportionately affect high-temperature sensor supply chains — essential for firms that cannot tolerate thermal-measurement downtime.

Demand drivers: Precision temperature control needs in semiconductor fabrication, metallurgical processes, and advanced ceramics continue to push demand for high-temperature measurement solutions. Buyers are increasingly valuing repeatability, traceability and integration-ready assemblies over commodity probes.

Raw-material exposure: High-temperature thermocouples used above 1000°C rely on platinum-rhodium alloys for core performance. Our sensitivity models quantify how fluctuations in precious-metal pricing and availability can ripple through supplier margins and end-user procurement costs.

Standards and compliance: Evolving standards (for example, recent updates to industry test methods and the continuing application of IEC/ASTM accuracy and EMF-temperature standards) are raising the bar for traceability and certification — creating both a barrier and a differentiator for vendors.

Product evolution: Adoption of mineral-insulated probes, multi-point assemblies, and integrated digital calibration is accelerating in higher-value applications. The market is bifurcating between engineered assemblies for demanding processes and commodity sheathed probes for routine service replacement.

Comprehensive market sizing and seven-year forecasts with scenario stress-testing tied to raw-material price bands and demand-shock events.

Vendor benchmarking and scorecards covering technical breadth, custom-assembly capability, service footprint, certification readiness, and commercial terms.

Procurement playbook with negotiation levers, recommended contracting timeframes for critical alloys, and tactical sourcing routes to reduce lead-time risk.

Product roadmaps and R&D prioritization matrix for OEMs and sensor makers (including trade-offs between exotic alloy formulations and design-for-repairability).

Supply-chain heatmap identifying single-point risks, substitution pathways for platinum-rhodium exposure, and inventory strategies for production continuity.

Regulatory and compliance checklist aligned to ASTM and IEC norms, including practical implementation steps for audit readiness and hazardous-location approvals.

M&A and partnership screening framework highlighting target profiles that accelerate access to high-value verticals (e.g., semiconductor handling or aerospace-grade assemblies).

The high-temperature thermocouples market presents a moderately concentrated supplier base: our market concentration analysis shows the top three players control a meaningful share of revenue while the top five increase that concentration materially. This structure favors established specialists with deep alloy know-how and wide channel reach, but there is still room for focused challengers that can combine application expertise with rapid customization and strong service delivery.

Key vendor archetypes and positioning notes included in the report:

Full-solution incumbents (e.g., established engineering brands): Firms with broad portfolios — covering exotic alloys, high-integrity probes and calibration services — remain go-to partners for industrial OEMs and laboratory customers that require single-source reliability.

Process-specialists: Suppliers that tailor assemblies for steel, glass, or semiconductor environments command pricing power where process conditions demand bespoke designs and tight tolerances.

Assembly-focused challengers: Manufacturers that emphasize short lead-times, custom termination styles, and application-specific sealing solutions capture a growing share of aftermarket and retrofit opportunities.

The report contains individual competitive profiles on leading names in the space, assessing strengths such as exotic alloy capability, global service networks, product innovation and vertical concentration. We also catalog recent industry events and certifications — for example, updated hazardous-location approvals and prominent trade-show participations — and map what these developments imply for commercial momentum and certification risk.

Certification moves that expand approved models for hazardous locations — a factor that reduces replacement downtime for process operators and raises the certification premium vendors can charge.

Active participation by suppliers at major industry expos and aerospace/space technology events — signaling product roadmaps aligned to higher-reliability, high-value markets.

Continued vendor emphasis on sensor assemblies and integrated solutions at processing trade events — pointing to aftermarket and systems-integration revenue growth.

Lock in raw-material exposure: Negotiate multi-year supply terms, consider consortium purchasing for platinum-rhodium inputs, and run hedging scenarios against the report’s price-sensitivity models to protect margin and availability.

Differentiate through services: Invest in calibration-as-a-service, traceability platforms and extended warranties for high-value installations — service revenue expands lifetime value and creates switching costs.

Prioritize certifications: Target compliance with the latest ASTM and IEC standards actively referenced in process specifications — certification drives access to regulated end-markets and reduces qualification cycles.

Pursue targeted M&A or alliances: For OEMs and system integrators, acquiring niche assembly specialists or forming exclusive supply partnerships accelerates access to verticals where custom solutions command premiums.

Operationalize scenario-based procurement: Use the report’s stress-tested forecasts to size safety stock, define reorder points for critical probe types and plan CAPEX in line with 5.17% CAGR expectations rather than one-off annual extrapolations.

Procurement leaders will find the report actionable for vendor rationalization and contract design; R&D leaders can prioritize efforts around mineral-insulated and multi-point assemblies where margin expansion is possible; corporate development teams receive a shortlist and valuation lens for M&A targets that plug capability deficits. Investors and private equity teams get an industry-level valuation framework tied to durable demand drivers and supply-side constraints that underpin mid-single-digit growth.

This press release showcases the report’s analytical depth and practical orientation while following our “trailer” principle: to preserve the strategic value of the full study we have intentionally omitted detailed segment tables, region-by-application revenue splits and the granular vendor scorecards that drive tactical sourcing and M&A decisions. The full Worldwide High Temperature Thermocouples Market report contains those proprietary tables, supplier-specific benchmarks and transaction-ready recommendations required to operationalize a 2026 strategy.

To access the complete dataset, scenario models, supplier scorecards and the tactical playbook for procurement and M&A, visit the PW Consulting report page or contact our industry team for a briefing. If your 2026 planning cycle includes decisions on sourcing, certification priorities, or capability acquisition in high-temperature measurement, this analysis is designed to be your tactical companion.

For detailed analysis of this topic, please visit the official page:Worldwide High Temperature Thermocouples Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com